Asia Faces Major LNG Supply Risks as Strait of Hormuz Tensions Mount

Rising Concerns Over a Crucial Energy Artery

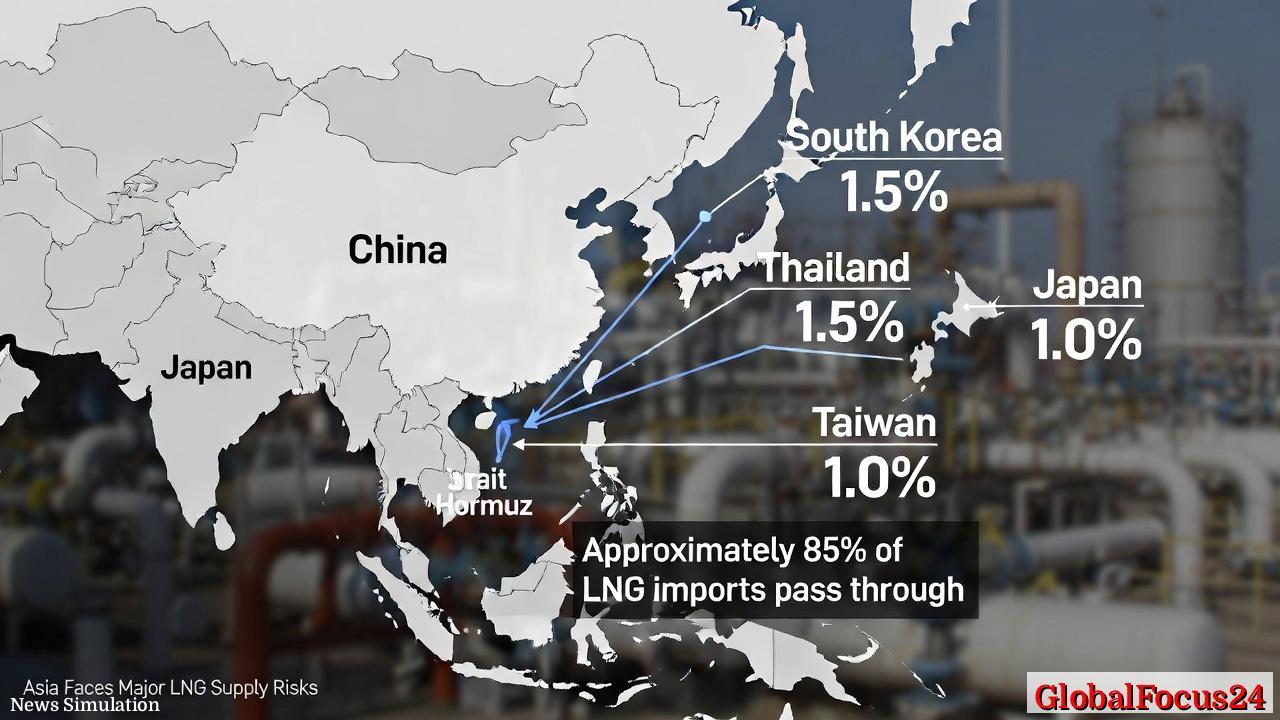

Asia’s energy security is facing a renewed test as potential disruptions in the Strait of Hormuz threaten to choke the flow of liquefied natural gas (LNG) to key economies across the region. Roughly 85% of global LNG that passes through the narrow waterway is destined for Asia, where countries such as Japan, South Korea, Thailand, and Taiwan rely heavily on imported gas to power industries and urban centers. With limited rerouting options and steep trade deficits tied to LNG imports, the region is bracing for potential volatility that could reverberate through energy markets, manufacturing, and national budgets.

The Strait of Hormuz, barely 21 miles wide at its narrowest point, has long been one of the most strategically vital—and vulnerable—maritime chokepoints. Located between Oman and Iran, it is the conduit for nearly one-fifth of global oil and a substantial share of LNG exports, particularly from Qatar. Any instability in this narrow stretch of water could have cascading consequences for Asia’s energy supply chain.

The Scale of Asia’s Dependence

The region’s LNG demand has soared over the past decade as countries transition away from coal and nuclear energy, seeking cleaner and more flexible alternatives. In this energy pivot, LNG has become indispensable—not just as a fuel for electricity generation but also as a feedstock for petrochemical industries and a backstop for emerging renewable grids.

Japan is the world’s second-largest LNG importer, with consumption levels that account for nearly 20% of global trade. Despite a diversified supply chain drawing from nations such as Australia, the United States, and Qatar, its energy deficit linked to LNG imports stands at approximately 1.0% of GDP. The island nation’s dependence is underscored by its legacy nuclear constraints following the 2011 Fukushima disaster, which accelerated a turn toward gas-fired power.

South Korea, Thailand, and Taiwan are in even more precarious positions. Each is reporting LNG trade deficits of roughly 1.5% of GDP—one of the highest ratios in the region. These economies have limited domestic energy resources and depend on consistent maritime supply routes for stability. South Korea, home to major refiners and shipbuilders, has also positioned LNG at the heart of its industrial modernization strategy. Thailand and Taiwan, both heavily reliant on imported energy for manufacturing, face pressing challenges in securing alternatives should shipments through Hormuz be interrupted.

China presents a different picture. It is the world’s largest LNG importer by volume, overtaking Japan in 2023, but its import-related deficit remains nearly flat relative to GDP size—an indication of its economic scale and diversified sourcing strategy. China’s growing use of long-term contracts and equity investments in overseas gas fields has provided some cushion against global spot market volatility.

Limited Rerouting Options Heighten Exposure

The structural geography of Asia’s energy trade leaves few practical alternatives in the event of a major disruption through the Strait. Most LNG bound for East and Southeast Asia is loaded in Qatar’s Ras Laffan terminal and must pass through Hormuz before crossing the Indian Ocean. While some volumes could, in theory, be redirected from suppliers in Australia, the United States, or Africa, production capacity and existing commitments limit flexibility.

Australia remains Asia’s largest regional LNG supplier, but its export infrastructure is already running near capacity, serving long-term contracts with Japan, South Korea, and China. The United States has significantly expanded its global LNG footprint over the past five years, with terminals in the Gulf of Mexico sending record volumes to Europe following the war in Ukraine. However, logistical constraints make sustained redirection to Asia challenging without substantial shipping time and cost increases.

In practice, any significant Hormuz obstruction would immediately tighten supply in Asia’s LNG spot market, bidding up prices and forcing governments to draw on strategic reserves or reduce industrial consumption. Given that many Asian economies import over 90% of their energy needs, even short-term disruptions could trigger price spikes across power and manufacturing sectors.

Economic Implications and Inflationary Pressures

The economic consequences of an LNG shock in Asia could be profound. Natural gas prices directly affect electricity costs, industrial output, and consumer inflation. The region’s energy-intensive economies—particularly those with large petrochemical, electronics, and automotive industries—would face eroding profit margins and rising costs of production.

A hypothetical two-week supply interruption through Hormuz could raise Asian spot LNG prices by more than 30%, analysts estimate, depending on the speed of restoration and availability of reserve supply. Such volatility would ripple through currency markets and fiscal planning. Governments that subsidize electricity, such as in Thailand and South Korea, would be compelled to increase budget outlays, pushing up fiscal deficits. In energy-import-dependent Japan, higher LNG import bills could weaken the yen and amplify concerns over inflation, already a growing challenge for the Bank of Japan.

For emerging economies across Southeast Asia, where gas-fired generation supports industrialization, tightening LNG supplies could slow growth and strain public finances. Moreover, high global energy prices typically incentivize coal consumption—undermining regional climate targets and carbon reduction strategies.

Historical Context: Energy Routes and Regional Vulnerability

Asia’s energy risk exposure through Hormuz is not new. Historical episodes such as the 1980s Iran-Iraq War and the 2019 Persian Gulf tanker attacks underscored how vulnerable the route is to geopolitical shocks. In both cases, temporary disruptions sent oil and gas prices upward, forcing importers to reassess diversification strategies.

Following those crises, several Asian economies embarked on building strategic LNG reserves and investing in pipeline infrastructure, albeit with limited success. Japan and South Korea each maintain small public and private LNG storage facilities, but these reserves cover only weeks of consumption. In contrast, China has accelerated construction of underground gas storage and pipeline connections linking Central Asian suppliers, reducing its relative exposure to maritime chokepoints.

Despite progress, Asia’s overall LNG infrastructure remains shaped by seaborne trade. Roughly two-thirds of imports arrive via long-haul shipping, a pattern unlikely to change soon given the slow pace of alternative pipeline development. The long-discussed Trans-Asian Gas Pipeline has made little headway beyond sections in Central Asia, leaving the balance of LNG logistics dependent on maritime stability.

Regional Comparisons and Strategic Adjustments

Asian governments are exploring multiple pathways to reduce vulnerability. Japan is stepping up joint purchasing frameworks with South Korea and Taiwan to improve buying power and coordination during supply emergencies. The three economies are also investing in flexible floating storage and regasification units (FSRUs) that can be repositioned as needed.

Southeast Asia’s approach differs. Thailand is expanding its Map Ta Phut terminal capacity and considering long-term supply contracts with the United States and Mozambique. Vietnam, a newcomer to LNG imports, has accelerated terminal construction but remains reliant on Qatari and Australian cargoes.

China is likely to maintain its diversified strategy. Alongside imports from Qatar and the United States, Beijing has cultivated pipeline gas links with Russia via the Power of Siberia network, giving it partial insulation from maritime risks. However, pipeline capacity remains modest compared to overall demand, meaning LNG will continue to play a pivotal role for decades.

India, while outside East Asia, plays a growing part in the regional energy map. With its proximity to the Strait, India could serve as a staging hub for emergency LNG redistribution, though its domestic consumption and infrastructure limitations constrain that potential.

Market Impacts and Long-Term Transition Pressure

The broader LNG market is already under strain. Global demand has risen faster than liquefaction capacity, and project delays have slowed new supply from Africa and North America. As a result, Asia’s leverage in the spot market may weaken further if supply disruptions persist or geopolitical tensions escalate.

Over time, energy security fears may accelerate transitions toward renewables and domestic energy resilience. Countries such as Japan and South Korea have expanded investments in hydrogen, offshore wind, and energy storage projects to reduce dependence on imported gas. Yet these technologies remain years away from offsetting LNG demand at scale.

For the foreseeable future, LNG remains the cornerstone of Asia’s power and industrial landscape. Any instability through the Strait of Hormuz therefore constitutes not only a logistical challenge but also a structural test of the region’s economic endurance.

Outlook: Managing a Fragile Energy Lifeline

Analysts warn that Asia’s energy planners must prepare for a “new normal” in which geopolitical risk is an enduring factor in pricing and procurement. The region’s economies, previously able to rely on steady gas flows and stable pricing, now confront an era where security of supply carries its own cost premium. Greater coordination on emergency reserves, regional grid connections, and investment in alternative fuel technologies will be critical to weather future disruptions.

For now, the combination of high dependency, constrained alternatives, and exposed trade balances places Asia at the epicenter of global LNG risk. The region’s next moves—whether through diplomacy, diversification, or innovation—will shape not only its energy future but also the stability of global markets for years to come.