Iranian Missile Strike Cripples Qatar’s Ras Laffan LNG Hub, Disrupting 17% of Global Supply

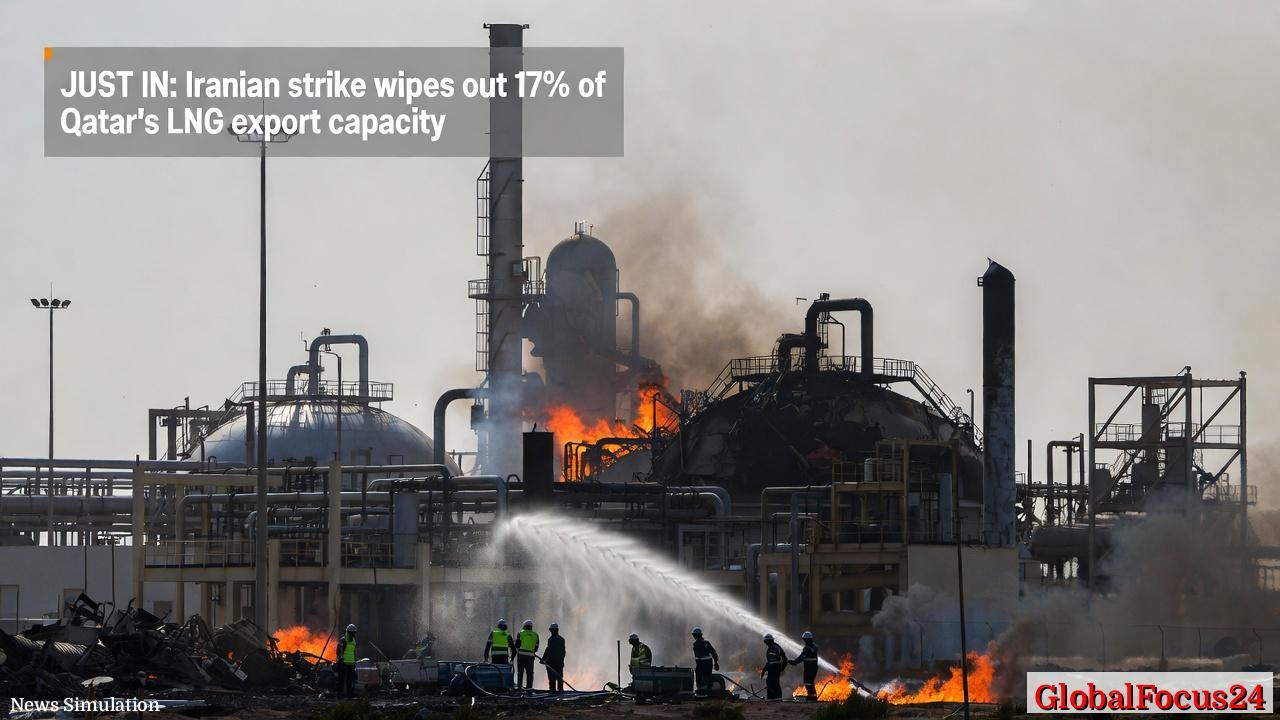

Qatar’s position as the world’s leading exporter of liquefied natural gas (LNG) has been shaken after a missile strike, attributed to Iran, devastated parts of the country’s Ras Laffan Industrial City overnight. The attack, which ignited large-scale fires across the complex, has sidelined approximately 17 percent of Qatar’s total LNG export capacity—an estimated 12.8 million tonnes per year. With restoration expected to take up to five years, the global energy sector faces one of its sharpest supply shocks in recent history.

Damage at the Heart of Global LNG Production

Ras Laffan Industrial City is the beating heart of Qatar’s energy economy—a sprawling complex that processes natural gas from the country’s massive North Field and converts it into LNG for export worldwide. The facility’s scale is unmatched, feeding demand across Europe, Asia, and parts of the Americas. The missile strike, however, has left several LNG trains—large industrial systems that condense gas at cryogenic temperatures—damaged or destroyed.

According to a statement from QatarEnergy, the state-owned energy producer, initial inspections show “extensive fire and structural damage across multiple LNG processing units and adjacent utilities.” Although no fatalities were reported, the operational blow is profound. Experts estimate it will take three to five years to fully repair the cryogenic systems, which require specialized materials and precision engineering that cannot be rapidly sourced.

Civil defense teams spent the night battling blazes fueled by residual gas and hydrocarbons. Satellite imagery on Thursday showed thick plumes of smoke drifting over the Persian Gulf, while emergency shutdown protocols were triggered across neighboring facilities to prevent further accidents.

Economic Impact on Qatar and the Global Market

The immediate consequence of the attack is a sharp contraction in Qatar’s export capacity. The loss of 12.8 million tonnes annually represents almost a fifth of global LNG supply, a volume crucial to international energy stability. Qatar’s LNG exports are a cornerstone of the country’s GDP and foreign exchange earnings, as well as a stabilizing factor in global energy markets.

Financial analysts in Doha and London expect Qatar’s GDP growth outlook for 2026 to be revised downward by as much as 1.5 to 2 percent due to lost export revenues and repair costs. Insurance and reconstruction expenses are expected to exceed several billions of dollars, placing additional strain on the state budget despite Qatar’s considerable sovereign wealth reserves.

Globally, the LNG market response has been immediate and severe. European and Asian spot prices jumped by double digits within hours of the news, reversing months of relative stability. Importers in Japan, South Korea, Germany, and the UK—already navigating tighter energy balances—face renewed cost pressures as they scramble to secure replacement cargoes from the United States, Australia, and Africa.

A Blow to Energy Security in an Unstable Region

The missile strike threatens to unsettle the fragile equilibrium of global energy security, particularly in Europe and Asia. Europe’s pivot toward LNG accelerated after 2022, as Russian pipeline gas became politically and logistically constrained. With Ras Laffan down, European utilities are under pressure to diversify supplies even further, though existing alternatives are limited.

Asian buyers, long-term partners of QatarEnergy, also face disruption. The majority of Qatar’s LNG exports are bound under long-term contracts to countries like South Korea, Japan, China, and India. While these agreements offer fixed pricing stability, they do not protect customers from supply force majeure events. Several importers are now expected to invoke contingency clauses or seek arbitration to manage shortfalls.

The timing of the strike compounds these challenges. Global gas reserves were already trending below seasonal averages following a colder-than-expected winter in the Northern Hemisphere. Analysts warn that another supply loss of this magnitude could push the market into a sustained deficit through 2027 if other exporters cannot increase output.

Historical Context: LNG’s Strategic Evolution

Since the 1990s, Qatar’s deliberate investment in LNG infrastructure has transformed it from a small oil producer into a centerpiece of global energy trade. Ras Laffan, developed over successive phases beginning in 1996, has been symbolic of that rise. Its carefully managed partnerships with Western energy majors, including Shell, ExxonMobil, and TotalEnergies, established Qatar as a reliable and technologically advanced supplier.

However, this reliability is now under scrutiny. While Ras Laffan’s security infrastructure was considered robust, the precision targeting of key processing units suggests significant intelligence and ballistic capacity behind the attack. Historical parallels can be drawn to regional assaults on energy infrastructure, such as the 2019 drone strike on Saudi Arabia’s Abqaiq facility, which temporarily disabled 5 percent of global oil production. Yet the scale and complexity of Ras Laffan’s damage appear even more consequential.

Regional Tensions and Strategic Ramifications

The strike follows months of increasing strain between Tehran and Doha, particularly over shared offshore gas fields that straddle the Qatar-Iran maritime boundary. The North Field, known as South Pars on the Iranian side, is the largest natural gas field in the world and has long been a delicate subject of resource competition. Recent diplomatic disagreements over production rights and maritime boundaries have escalated rapidly.

In response to the attack, Qatar expelled Iranian military and security attachés, calling the strike “a grave act of aggression against civilian infrastructure vital to global energy stability.” Regional allies, including Saudi Arabia and the United Arab Emirates, have reportedly strengthened naval patrols in the Gulf to secure shipping lanes and LNG carrier routes.

International reaction has been swift. The International Energy Agency (IEA) called for “urgent global coordination to ensure supply continuity.” Meanwhile, U.S. and European officials condemned the strike as “destabilizing” and encouraged emergency releases from strategic reserves to mitigate price spikes. Financial markets responded with volatility: energy sector equities surged, while broader indices posted minor losses amid uncertainty over oil and gas supply chains.

Reconstruction Challenges and Long-Term Recovery

Rebuilding Ras Laffan will be a formidable task. LNG production facilities operate under extreme conditions—temperatures lower than -160°C and immense pressures. Any damage to cryogenic heat exchangers, compressors, or pipelines requires custom fabrication, often taking years for procurement and installation. Additionally, replacement parts are typically produced by specialized firms in Japan, Germany, and the U.S., meaning supply chain constraints could slow recovery efforts.

Industry experts anticipate QatarEnergy will prioritize partial resumption of production at undamaged units within 12 months to stabilize essential export contracts. However, full operational capacity is not expected before 2030. The company is also likely to accelerate development of its North Field East and North Field South expansion projects, which were originally planned to boost output by 2027.

Comparison with Other Global LNG Producers

Qatar’s supply shortfall opens a temporary window for other exporters. The United States, Australia, and Mozambique stand to benefit from higher spot prices and contract renegotiations. U.S. Gulf Coast terminals could reroute additional cargoes to Europe, while Australian suppliers may gain leverage in Asian markets. However, experts caution that these shifts are temporary stopgaps rather than permanent replacements, given Qatar’s unmatched scale and consistency.

Globally, LNG infrastructure is already operating at near-maximum levels. U.S. liquefaction capacity, for instance, is constrained by maintenance cycles and ongoing expansion projects. Meanwhile, Australian operators face their own technical and regulatory hurdles. As such, while some market balance could return by late 2027, sustained high prices are expected to persist for at least two years.

Broader Economic Ripples

Beyond the energy sector, the Ras Laffan incident threatens broader economic repercussions across shipping, manufacturing, and finance. LNG shipping rates have surged sharply, with charter rates rising more than 20 percent overnight as vessel availability tightened. Global equity markets reacted unevenly: heavy industries dependent on gas feedstock, such as chemicals and steel, face increased input costs that could reduce profit margins worldwide.

Developing economies reliant on imported LNG are particularly vulnerable. Countries in South Asia and Africa, already struggling with foreign exchange pressures, may be forced to revert to heavier fuel oil or coal, reversing recent gains in cleaner energy adoption. Energy poverty risks are once again emerging as a pressing concern for policymakers.

Outlook: Years of Uncertainty Ahead

The missile strike on Ras Laffan marks a defining moment for global energy security. The world’s largest LNG producer has been severely disrupted, and while emergency measures and allied cooperation may cushion immediate effects, the path to recovery will be long. For Qatar, the incident underscores both the fragility and the strategic importance of its energy infrastructure. For the rest of the world, it’s a reminder of how regional instability in the Gulf continues to reverberate far beyond its shores.

As crews work around the clock to assess and repair the damage, global energy markets are bracing for prolonged volatility. The coming months will test the resilience of international energy supply chains—and perhaps permanently reshape the dynamics of the liquefied natural gas industry.