U.S. Weighs Suspension of Crude Exports as Global Oil Prices Surge Amid Iran Conflict

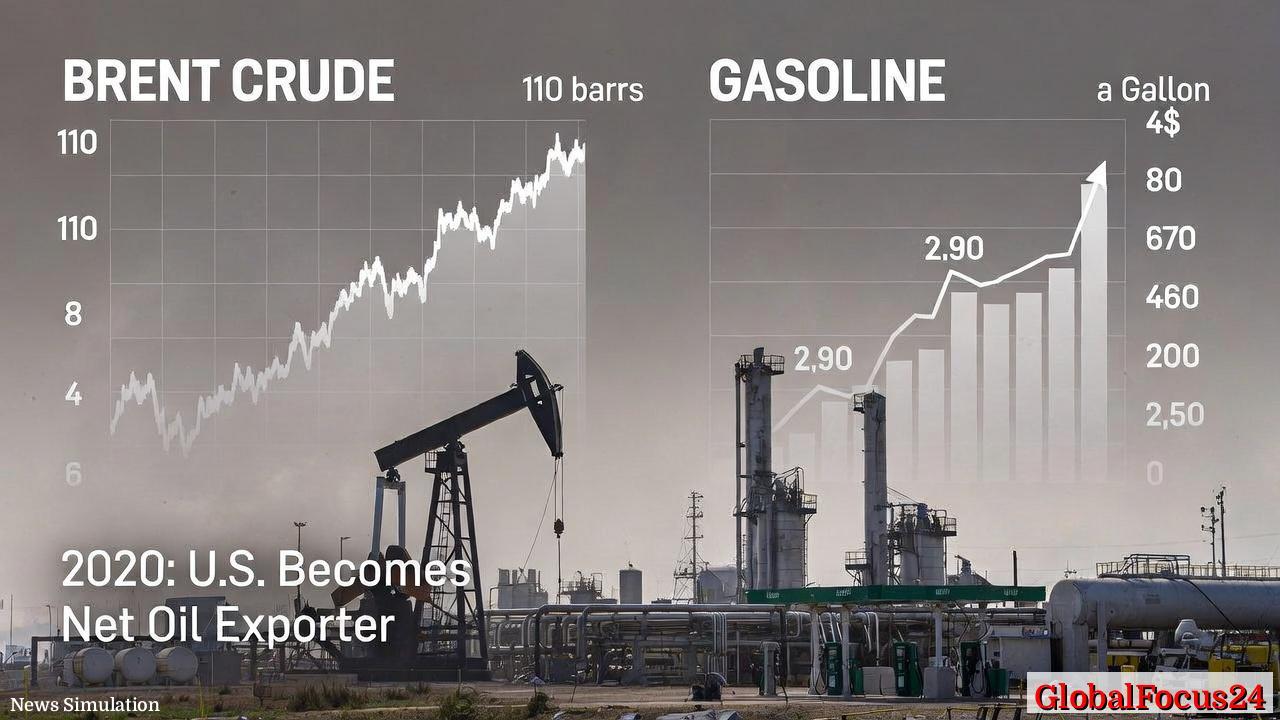

Amid volatile energy markets and heightened geopolitical tensions, American policymakers are weighing a temporary suspension of crude-oil exports. The consideration comes as Brent crude prices have surged past 110 dollars per barrel and U.S. gasoline prices have climbed from 2.90 to nearly 4 dollars per gallon within weeks—levels not seen since the early 2020s. The move underscores the United States’ complex position as both a major oil producer and refined product exporter, and its growing struggle to balance domestic fuel security with global market participation.

A Shift Decades in the Making

The United States became a net exporter of oil in 2020 for the first time since the 1940s, marking a turning point in the global energy balance. Driven by the shale revolution, domestic production soared through the mid-2010s, allowing the country to reduce dependency on foreign oil. The lifting of a decades-old export ban in 2015 opened new markets for U.S. crude—particularly in Europe and Asia—solidifying its role as a swing supplier in the global system.

However, the prospect of temporarily reinstating export restrictions now reflects both strategic caution and domestic political pressure. Rising fuel costs are straining household budgets and prompting renewed calls for government action. The challenge for officials lies in identifying measures that relieve consumers without undermining the fragile equilibrium that keeps U.S. refineries running efficiently and global oil flows stable.

Understanding the Export Dilemma

A suspension of crude exports would likely flood domestic markets with a surplus of light, sweet crude—the type most commonly produced by U.S. shale fields in Texas, New Mexico, and North Dakota. In theory, that oversupply could bring short-term relief to American drivers, as crude prices dip and refiners access cheaper feedstock.

But the nation’s refining system presents a structural mismatch. Many U.S. refineries, particularly those along the Gulf Coast, are configured to process heavier, sour crude imported from countries such as Venezuela, Mexico, and Canada. Light crude can be refined more easily into gasoline, but yields less diesel and jet fuel—products that remain in high demand domestically and abroad. The potential imbalance could send shockwaves across the broader fuel supply chain.

Short-Term Gain, Long-Term Disruption

If Washington moves forward with a temporary export halt, the immediate effect could indeed be a pullback in retail gasoline prices. Consumers might see a short-lived drop at the pump as refineries process the surplus. Yet analysts warn that such a reprieve would come at a cost.

A glut of gasoline would quickly build up, forcing refiners to export the excess in order to avoid storage bottlenecks. Meanwhile, the decline in diesel and jet fuel production could create new shortages, driving up costs for trucking, aviation, and manufacturing industries reliant on middle distillates. Refinery margins—typically driven by the spread between crude costs and product prices—would tighten sharply. Within weeks, reduced profitability could prompt output cuts and even temporary shutdowns, undermining the policy’s intended benefits.

Historical Lessons from U.S. Energy Policy

Energy export restrictions are not new to the American experience. During the 1970s oil crises, Washington imposed various controls on exports and pricing to stabilize domestic markets. While those actions provided temporary relief, they also discouraged investment, distorted market signals, and deepened dependence on external suppliers over the long term.

When Congress lifted the crude export ban in 2015, it was largely a recognition that market-driven trade had become a more effective stabilizer than government intervention. The improved flexibility allowed U.S. producers to respond to global shifts—such as OPEC’s production cuts or disruptions in the Middle East—without triggering domestic shortages. Today’s policy debate echoes many of the same dilemmas from that era: intervention may protect consumers in the short run but at the risk of market instability down the line.

Economic and Strategic Stakes

Despite the temptations of short-term price relief, the economic consequences of reinstating export restrictions could be severe. Energy exports have become a critical pillar of the U.S. trade balance, helping offset deficits in other sectors. In 2023, crude oil and petroleum products accounted for a significant share of total American exports, supporting thousands of jobs across production hubs like the Permian Basin, Bakken region, and Gulf Coast refining corridor.

A suspension would likely dampen upstream investment, as shale producers face shrinking profit margins and reduced access to global buyers. That could lead to slower production growth just as other major suppliers—such as Saudi Arabia and Russia—continue to manage their output strategically. In the longer term, diminished investment could cap domestic capacity, leaving future consumers more vulnerable to supply shocks.

Moreover, a policy pullback could sour relations with key trading partners who have come to rely on U.S. crude as a stable alternative to politically riskier sources. European refineries, many of which adapted their operations to handle lighter American oil after reducing imports from Russia, would face immediate feedstock shortages. This could tighten the global market further, ironically driving world prices even higher.

Comparing Global Responses

Other regions have faced similar conundrums. For instance, when Indonesia temporarily restricted palm oil exports in 2022 to contain local cooking oil prices, the move disrupted global supply chains and ultimately backfired domestically as market distortions deepened. Likewise, Argentina’s historical use of grain export taxes and restrictions often led to weaker farm output and smuggling rather than lasting price stability.

Energy market dynamics function similarly, though at far larger scale and complexity. Global oil flows are intertwined; disruptions in one hub rapidly propagate through pricing mechanisms worldwide. In this context, analysts caution that isolating U.S. crude from international markets—even briefly—could amplify global volatility rather than contain it.

Energy Independence vs. Market Integration

The debate also exposes the nuanced difference between “energy independence” and “energy security.” Achieving net-exporter status gave the United States a psychological boost, suggesting reduced vulnerability to foreign supply shocks. Yet true energy security depends not only on self-sufficiency but also on flexible markets, diversified supply routes, and resilient logistics.

The modern oil system operates as a global network, where supply and demand continuously adapt through trade. By participating fully, the United States enhances its influence over pricing and stability. Voluntarily stepping back could erode that influence, yielding ground to other producers eager to fill the gap.

Capacity and Refining Constraints

Underlying the policy debate is a physical limitation: refining capacity. Despite strong production growth, U.S. refining throughput has plateaued in recent years as environmental regulations, labor costs, and limited investor appetite curbed expansion. Several older refineries have been converted to renewable diesel or biofuel facilities, further tightening the system’s flexibility.

Introducing large new volumes of light crude into an already constrained network could overwhelm existing configurations. Adjusting facilities to process different crude grades requires time, capital, and technical reengineering—not a feasible short-term fix. As a result, even if export bans boosted domestic crude availability, refineries might struggle to utilize it efficiently.

Consumer and Industry Reactions

Public response has been mixed. Consumers and advocacy groups frustrated by high gasoline prices largely support aggressive measures to bring relief. Industry stakeholders, however, warn that government intervention could have unintended ripple effects. Energy executives emphasize that stable policy and open markets remain crucial for ensuring both affordability and long-term reliability.

Market analysts also note that price spikes driven by geopolitical tension often recede once supply expectations stabilize. If the Iran conflict de-escalates or alternative production enters the market, crude prices could normalize without heavy-handed action. Policymakers, then, face the delicate task of determining whether the recent surge represents a transient shock or a sustained disruption.

Balancing Pressure and Prudence

As officials deliberate, several alternatives are on the table. These include releasing additional barrels from the Strategic Petroleum Reserve, adjusting refinery blending mandates, and encouraging temporary production increases in key basins. Each option carries tradeoffs, but collectively they could mitigate the immediate consumer pain without distorting global trade patterns.

Ultimately, the decision will hinge on balancing domestic political imperatives with long-term strategic stability. The United States occupies a unique position: both vulnerable to global prices and instrumental in shaping them. Policymakers must weigh whether insulating consumers in the short term is worth the potential cost of global market fragmentation.

A Test of U.S. Energy Leadership

The current situation serves as a stress test for America’s energy strategy in an interconnected world. The export debate highlights enduring structural tensions between national self-interest and global economic integration. As recent history shows, energy markets often punish isolation and reward adaptability.

If the U.S. proceeds with an export suspension, it would mark a symbolic reversal of decades of liberalization and market openness. If it resists that impulse, it reaffirms a commitment to market principles, even under political pressure. Either way, the coming weeks will determine how resilient America’s energy transformation truly is—and whether its newfound exporter status can withstand the next wave of global uncertainty.