U.S. Stocks Surge as Markets Defy Strait of Hormuz Closure and Eye Further Gains

Wall Street Rallies Despite Global Energy Disruption

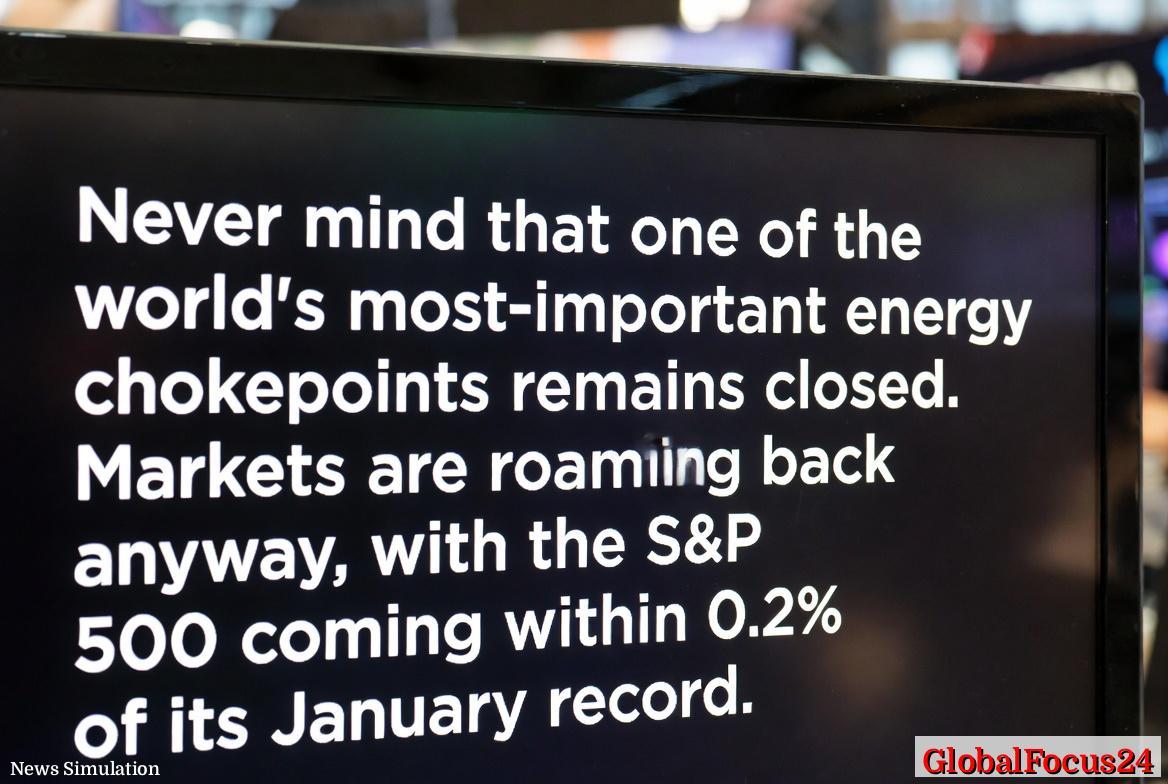

U.S. stock markets surged on Wednesday, extending a powerful rally that pushed the Nasdaq Composite to its longest winning streak since 2021. The advance came even as the closure of the Strait of Hormuz — one of the world’s most critical energy chokepoints — sent shockwaves through global commodity markets earlier in the week. Investors instead focused on robust corporate earnings and signs of economic resilience at home, brushing off geopolitical concerns that might have rattled markets in years past.

The S&P 500 ended the day just 0.2% shy of its all-time high set in January, while the Dow Jones Industrial Average climbed firmly higher on a wave of optimism surrounding corporate performance and easing energy pressures. The tech-heavy Nasdaq outperformed all major indexes, driven by gains in semiconductor, software, and cloud-computing shares.

Oil prices, which initially spiked following the Strait’s closure, retreated after reports suggested a potential peace agreement could restore the crucial waterway’s operations within days. The pullback in crude relieved inflation fears and reinforced investor confidence that the U.S. economy could power through geopolitical turbulence.

The Nasdaq’s Longest Winning Streak Since 2021

The Nasdaq Composite’s latest run marks its most sustained upswing in nearly five years. Companies in the artificial intelligence, cloud computing, and consumer electronics sectors led the charge, underscoring the market’s continued enthusiasm for growth-oriented technology stocks. Investors have rewarded firms showing consistent revenue growth and margin expansion despite higher financing costs and global uncertainty.

Market strategists noted that sentiment surrounding megacap tech companies remains upbeat, fueled by strong capital investment trends and an expectation that AI integration will sustain productivity and profit gains. This performance echoes the momentum of 2021 when optimism surrounding pandemic-era digital transformation spurred a surge in valuations across the technology landscape.

The difference in 2026, however, lies in the broader economic backdrop. Unlike earlier speculative phases, the current rally is underpinned by tangible corporate earnings and a resilient labor market. Unemployment remains below 4%, household consumption continues to rise, and productivity gains have tempered inflation pressures that once threatened to derail growth.

Energy Markets Settle as Diplomatic Hopes Rise

The closure of the Strait of Hormuz — through which roughly 20% of global petroleum passes — briefly rattled commodity markets, highlighting the waterway’s strategic importance. Historically, even temporary disruptions in the strait have triggered sustained spikes in crude oil prices and energy-related inflation worldwide.

This week’s developments initially pushed Brent crude above $100 per barrel, its highest level since late 2023, but prices later eased as diplomatic overtures signaled progress toward reopening the channel. The West Texas Intermediate benchmark followed a similar path, retreating to the mid-$80 range as traders recalibrated expectations.

Energy analysts noted that refined product supplies in Asia and Europe appeared sufficient to buffer short-term disruptions. U.S. energy producers, particularly in the Permian Basin, have also benefited from new export terminals and pipeline capacity, allowing domestic supply chains to absorb volatility more effectively than in past global crises.

The relatively measured market response underscored how improved logistics and diversified supply routes have dampened the impact of regional conflicts on global energy flows. For context, during earlier crises such as the 2019 tanker attacks and the 2011 Arab Spring, oil price surges persisted for weeks, significantly straining global equities. Today’s quick stabilization reflects both stronger inventory management and coordinated diplomatic pressure to prevent prolonged instability.

Wall Street’s Earnings Bonanza Fuels Optimism

Adding fuel to the rally, major U.S. banks posted blockbuster first-quarter earnings that exceeded Wall Street expectations. Institutions such as JPMorgan Chase, Goldman Sachs, and Bank of America reported double-digit profit growth, driven by robust trading volumes, dealmaking, and rising interest income.

Executives emphasized a healthy credit environment, with delinquency rates remaining low and consumer spending patterns solid. Corporate lending also showed renewed vigor, particularly among mid-sized firms expanding operations after last year’s slowdown. Analysts said the results suggest a financial system on firm footing, an encouraging signal for investors wary of credit cracks after the regional bank stresses seen in early 2023.

The results extended beyond the financial sector. Early reports from industrial and consumer companies revealed steady demand and improving margins, aided by easing input costs and continued automation. The broad-based strength lent credibility to the view that the U.S. economy remains exceptionally resilient compared with peers in Europe and Asia, where growth has been uneven.

U.S. Economic Outlook: Strength in Contrast

This week’s trading action underscored a growing divergence between U.S. economic momentum and slower recoveries in other major regions. Europe faces continued manufacturing weakness and persistent energy dependencies, while China’s post-pandemic rebound has struggled to regain its earlier pace amid soft global demand and cautious lending policies.

By contrast, U.S. business investment continues to expand, helped by infrastructure spending and onshoring incentives introduced over the past few years. The country’s energy independence, bolstered by record oil and gas output, further insulates it from global supply shocks. This contrast has fueled renewed foreign interest in U.S. equities and the dollar, contributing to upward pressure on asset prices.

Economists cited several structural advantages supporting U.S. growth: a flexible labor market, advanced technology ecosystem, and relatively stable political institutions. Together, these factors have encouraged long-term investors to maintain exposure to U.S. assets despite geopolitical volatility. The Federal Reserve’s cautious but transparent policy stance has also reassured markets, allowing equities to respond to data rather than speculation.

Historical Echoes and Inflation Context

Stock market rallies following global crises are not new in U.S. history. During the 1990 Gulf War, for instance, equities wavered as oil prices spiked but later rebounded strongly as diplomatic solutions took hold. A similar pattern emerged in 2003 and 2011, when energy disruptions and regional conflicts briefly unnerved investors before broader economic fundamentals reasserted control.

Currently, inflation remains a focus for policymakers and investors alike. The temporary rise in energy prices this month could liftinflation measures, but analysts expect any uptick to be contained if the Strait of Hormuz reopens as anticipated. Core inflation, which excludes food and energy, has already shown signs of slowing thanks to moderating wage growth and supply chain normalization.

The Federal Reserve faces a delicate balance: maintaining inflation progress while avoiding unnecessary tightening that could choke the recovery. For now, markets are betting that stable energy markets and robust corporate earnings will allow the central bank to proceed cautiously, possibly holding rates steady through the summer.

Investor Sentiment and Market Dynamics

Investor sentiment, buoyed by strong fundamentals and a steady stream of positive data, has improved markedly since late last year. Market volatility, as measured by the VIX index, has fallen to its lowest level in 18 months, reflecting reduced fear and a renewed appetite for risk.

Retail participation has also grown, with trading activity on major brokerage platforms rising as confidence returns. Institutional investors have increased allocations to U.S. equities, emphasizing technology, energy, and industrial sectors expected to benefit most from ongoing economic expansion.

However, some analysts warn that complacency may be creeping in. Equity valuations, particularly in the tech sector, have reached levels reminiscent of previous peaks. While earnings growth justifies part of the rally, sustained gains may depend on continued macroeconomic stability and the swift resolution of geopolitical tensions in the Gulf.

Regional Comparisons Highlight U.S. Leadership

Comparisons with other major markets underscore Wall Street’s relative strength. The MSCI Europe Index has lagged behind the S&P 500 by roughly 8% year-to-date, while Asian indexes have seen mixed performance amid uneven policy support and currency headwinds. The resilience of the U.S. consumer — still spending, earning, and saving at healthy rates — stands in contrast to more cautious households abroad.

In emerging markets, currency fluctuations and elevated borrowing costs have constrained equity performance, further reinforcing America’s role as the preferred destination for capital. The reopening optimism surrounding the Strait of Hormuz could ease global trade tensions and support energy-importing economies, but for now, U.S. markets remain the clear outperformers.

Outlook: Momentum Carries Forward

With earnings season off to a powerful start and energy markets calming, investors appear confident that the rally could extend into the second quarter. The prospect of a peace deal in the Gulf, combined with consistent economic data, has set the stage for another leg higher in U.S. equities.

Market observers remain attentive to potential risks — from interest rate shifts to geopolitical flare-ups — but optimism dominates trading desks. For now, Wall Street’s message is clear: despite global uncertainty, the American economy continues to lead, its markets resilient and its momentum intact.