EU Auto Tariff Push: U.S. hike on Cars and Trucks Signals Timely but Contested Trade Shift

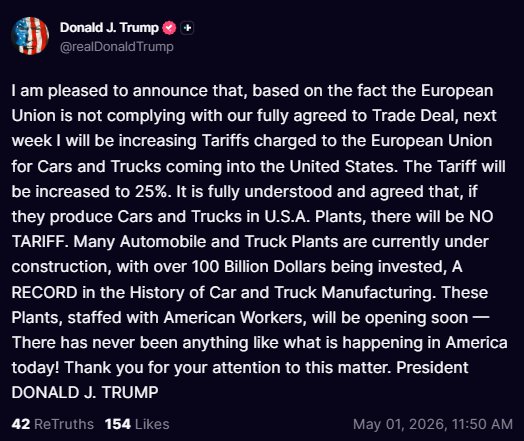

In a move that heightens the stakes of transatlantic trade, the White House announced a 25% tariff on automobiles and light trucks imported from the European Union. The decision, framed by the administration as a response to what it characterizes as noncompliance with a fully agreed trade framework, aims to recalibrate U.S.-EU economic relations at a moment of renewed focus on supply chains, domestic manufacturing capacity, and broader geopolitical alignment.

Context and historical thread

Automotive trade has long been a litmus test for the health of global commerce between the United States and Europe. The sector’s volume reflects decades of integrated manufacturing, cross-border investment, and complex regulatory alignment. After World War II, trade liberalization gradually deepened links between American carmakers and European suppliers, with harmonization efforts spanning safety standards, emissions rules, and labor practices. The current tariff move arrives within a broader historical arc of tariff policy where administration officials have alternated between tariff leverage and negotiated settlements to address perceived imbalances or noncompliance.

From a historical vantage point, the region’s automotive supply chain operates as a high-stakes, multinational puzzle. U.S. automakers rely on European hubs for engines, electronics, and specialized components, while EU manufacturers export advanced vehicles and technology to North American consumers. Any significant tariff shift reverberates through tiered suppliers, logistics networks, and showroom pricing, often prompting a rapid reassessment of sourcing strategies and capital deployment.

Economic rationale and potential impact

The 25% tariff targets imported cars and light trucks from EU member states, a category that includes vehicles from major European brands with significant U.S. market share. Proponents of the tariff frame it as a response to perceived noncompliance with an agreed framework designed to maintain fair competition and protect domestic manufacturing. Critics, however, warn of a broader economic ripple effect, arguing that higher import costs could elevate vehicle prices for American consumers, slow the pace of automotive investment, and ripple through related industries—from financing and insurance to road infrastructure funding and consumer goods sectors that rely on vehicle mobility.

Analysts expect several distinct channels of impact:

- Vehicle prices: A direct tariff would raise landed costs for imported cars and trucks, potentially translating into higher consumer prices at dealerships and a slower rate of price decline for domestic models that compete with European imports.

- Domestic manufacturing: U.S. automakers may respond by accelerating production in domestic plants or expanding capacity in regions with favorable logistics, labor, or incentives. Investment in electric vehicle (EV) ecosystems and related components could receive renewed policy emphasis as companies seek to diversify near-term risk.

- Supply chain recalibration: Suppliers that deliver European-origin components to U.S. assembly lines could experience shifts in demand, with potential localization trends or new sourcing agreements to mitigate tariff exposure.

- Trade balance and revenue: Tariffs generate government revenue and can alter the trade balance, but they also risk provoking retaliation or prompting compensatory measures that affect other sectors, creating a complex economic calculus for policymakers.

Regional comparisons and broader market dynamics

The tariff announcement sits alongside parallel global trade dynamics that include other major economies recalibrating their own tariff and subsidy structures. In Asia, manufacturing-led regions have benefited from diversified supply chains and incentive programs around EVs and autos. In Europe, nations with robust automotive industries—Germany, France, Italy, and others—face a balancing act between maintaining export strength and navigating the policy environment of a protectionist-era dialogue. Comparisons across regions highlight several trends:

- North American integration versus European diversification: The United States has historically favored near-shoring and regional supply security, while Europe emphasizes a larger, integrated internal market. Tariffs on EU vehicles could accelerate near-term localization in the U.S. but may also prompt European manufacturers to seek stronger footholds in other markets.

- EV transition pressures: As the auto industry pivots toward electric propulsion, control over battery supply chains and critical minerals becomes a strategic factor. Tariffs on conventional internal combustion engine vehicles could shift investment toward electric platforms that mitigate some exposure to cross-border costs, though batteries and materials may face their own tariff regimes.

- Consumer behavior under tariff uncertainty: Shoppers may respond to price signals with delayed purchases or a tilt toward domestically produced models, which could influence showroom dynamics, incentives, and financing conditions across the auto sector.

Industry and public reaction

Industry groups and labor unions have signaled a spectrum of responses. Manufacturers with substantial exposure to European-origin components express cautious optimism that the tariff could create a more level playing field, while warning that broad price increases could dampen demand. Automotive dealers, who operate on thinner margins than the big brands, are particularly attentive to any sustained price shifts that could erode consumer confidence and foot traffic.

Public sentiment typically hinges on the tangible cost impact. For many American households, a tariff increase on imported cars translates into higher sticker prices and potentially longer wait times if supply chains tighten or production retools are required. For regions with robust domestic assemblers and a skilled workforce, the tariff carries a narrative of protecting local jobs and investment, even as consumers weigh the trade-off against higher household expenditures.

Policy mechanics and next steps

Tariffs of this scope are typically accompanied by ongoing administrative processes, including trade remedy investigations, potential exemptions for specific models or components, and periodic reviews. The decision-making framework often considers:

- Compliance judgments: The basis for the tariff hinges on assessments of noncompliance with a broader agreement. The specifics of that assessment, including which elements are believed to be unmet and how they are measured, will influence subsequent policy refinements or negotiations.

- Retaliation risk: Historically, cross-border tariffs risk provoking retaliatory measures. European policymakers could respond with targeted duties on U.S. exports, which would complicate the macroeconomic outlook for sectors beyond autos.

- Negotiation pathways: The tariff could coexist with renewed talks intended to address the friction points cited by both sides. In such cases, timelines for concessions, verification mechanisms, and enforcement terms become critical negotiation levers.

- Domestic policy alignment: The tariff decision interacts with a broader set of domestic priorities, including manufacturing incentives, infrastructure modernization, and green energy strategies that are aimed at strengthening resilience and reducing long-run costs for consumers.

Historical context informs a cautious interpretation of immediate outcomes. Tariff actions in the automotive sector have proved time-limited, contingent on follow-on negotiations, sectoral exemptions, or shifts in the global economy. Policymakers often balance the desire to compel compliance with the need to prevent negative spillovers into inflation, consumer demand, and broader economic growth.

Regional and global considerations

Within the United States, diverse regions experience varying degrees of auto industry intensity. States with long-standing manufacturing hubs—Midwestern and Southern regions with established assembly plants and supplier networks—may experience more pronounced economic effects from tariffs due to higher local employment directly tied to auto production. Coastal regions, which typically house major ports and distribution centers, could see shifts in import patterns and logistics costs that ripple into retail prices and consumer access.

Beyond North America, global automakers have adapted to a landscape that includes shifting regional preferences, regulatory frameworks, and consumer tastes. In some markets outside the EU, automakers are increasingly leveraging local production to circumvent cross-border trade barriers and to capitalize on regional demand. The tariff decision could influence these strategic moves, accelerating localization or diversification of supply chains across continents.

Market-facing considerations for investors

For investors, the tariff announcement introduces an element of near-term uncertainty paired with longer-term strategic implications. Markets generally weigh:

- Short-term price effects: Expect potential volatility in auto equities and supplier stocks as traders price in the immediate impact on margins, input costs, and demand.

- Long-term structural shifts: If tariffs spur a sustained push toward domestic production and regionalized supply chains, equity valuations may tilt toward companies with greater local content, resilient balance sheets, and scalable EV platforms.

- Commodity and logistics exposure: Components such as steel, aluminum, and semiconductors, along with shipping and port services, can respond to tariff-driven shifts in demand and pricing.

Conclusion: A pivotal moment with cascading consequences

The 25% tariff on EU-origin cars and light trucks marks a pivotal moment in the ongoing evolution of transatlantic trade. It underscores the balancing act policymakers face between enforcing compliance, protecting domestic manufacturing, and preserving the affordability of automobiles for American buyers. As the policy sets in, the automotive ecosystem—from assembly lines and suppliers to dealers and consumers—will navigate a period of adjustment. The unfolding response from European partners, the direction of subsequent negotiations, and the broader trajectory of global trade policy will collectively shape how this tariff reshapes markets, regional competitiveness, and the everyday experience of choosing a vehicle in the United States.

In the weeks ahead, observers will monitor the tariff’s implementation details, potential exemptions, and any policy moves designed to stabilize prices for consumers while addressing the administration’s stated objectives. The outcome will likely influence future trade dialogues, setting a precedent for how the United States negotiates and enforces commitments within a highly interwoven global automotive sector.