China’s Industrial Sector Faces Deepening Losses as Profit Pressures Mount Amid Historic Deflation

A Historic Slide in Industrial Profits

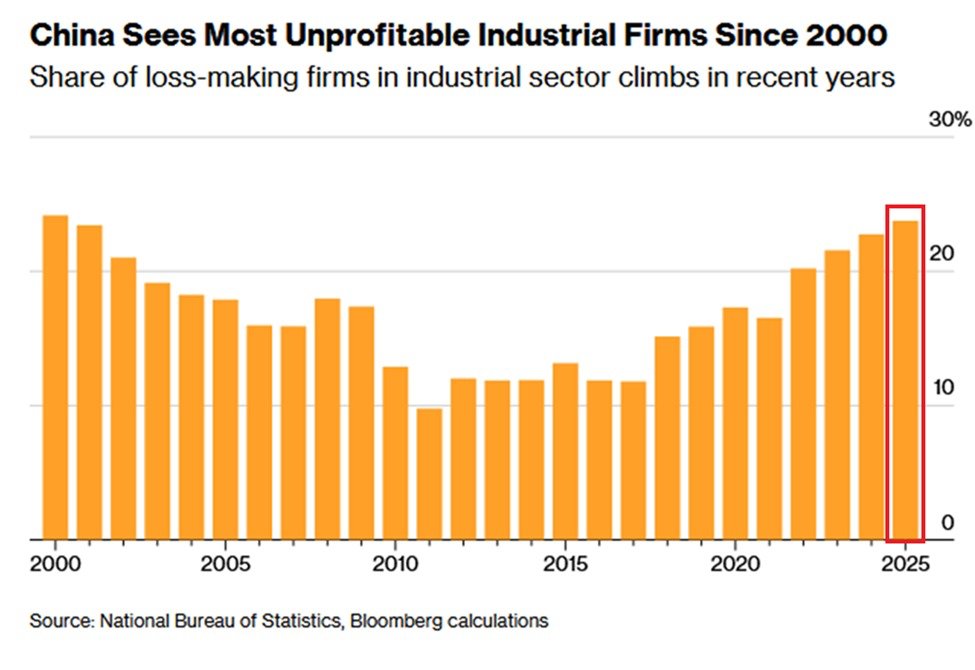

China’s industrial economy ended 2025 under the heaviest strain in more than two decades, with 23.8% of manufacturing and industrial firms reporting losses—the highest proportion since 2000. The figure, double the level recorded in 2017, underscores the breadth of the financial stress gripping the country’s once-dominant growth engine.

This marks the fourth consecutive year of rising losses across China’s vast industrial base, a streak unparalleled in modern records. Profit margins at privately owned industrial companies fell to just 4.5%, their weakest showing since at least 2014. Taken together, the data point to a sustained erosion in corporate earnings capacity and a decline in overall competitiveness at a time when the broader economy is battling persistent deflation and sluggish domestic consumption.

Deflation Tightens Its Grip

In 2025, China entered its longest deflationary stretch on record. Producer prices—an indicator of factory gate inflation—remained in negative territory for most of the year, driven by soft demand, excess capacity, and mild declines in global commodity costs. The deflationary spiral has left companies caught between falling sales prices and stubbornly high fixed costs, squeezing cash flow and diminishing appetite for investment.

At the consumer level, subdued wage growth and job insecurity have tempered spending. Although targeted government stimulus, including infrastructure investment and credit support to manufacturing, offered some reprieve, it failed to arrest the downward momentum in industrial profitability. The combination of weak pricing power and lower turnover has created a feedback loop that continues to weigh on corporate balance sheets.

The Shadow of War and Energy Costs

Compounding the domestic malaise are external shocks, most notably the surge in global energy volatility tied to the ongoing Iran War. After hostilities broke out in late 2024, oil prices fluctuated wildly, at times exceeding $120 per barrel before retreating as global output adjusted. For China—a country reliant on energy imports for roughly three-quarters of its crude oil needs—the conflict injected a new layer of uncertainty into industrial operations.

High energy costs, particularly for heavy industries such as steel, cement, and chemicals, eroded profit margins even further. Firms in these sectors have long depended on thin spreads and scale economies to stay profitable. The unpredictable cost base in 2025 made long-term production planning increasingly difficult, driving some state-owned enterprises to temporarily halt output or reduce capacity utilization.

A Weak Private Sector Undermines Recovery

Private manufacturers, often the most nimble segment of China’s economy, have been hit hardest by the deteriorating environment. While state-owned enterprises enjoy greater access to credit and policy support, smaller privately held firms struggle to secure sustainable financing. Many operate in competitive low-margin industries where pricing flexibility is limited.

The 4.5% profit margin recorded by private firms represents a steep drop from levels seen a decade ago, when industrial dynamism from consumer electronics, machinery exports, and automotive components powered China’s ascent as the “world’s factory.” Today, intense price competition—both domestically and from emerging manufacturing hubs in Southeast Asia—has eroded that advantage. Economists warn that without meaningful structural reforms, the gap in profitability between private and state-owned firms will likely persist or even widen.

The Weight of Overcapacity

Industrial overcapacity remains one of the most persistent obstacles to recovery. Years of aggressive investment during China’s post-2008 stimulus era created excess production capability in sectors ranging from aluminum to shipbuilding. Even after multiple policy campaigns to curtail obsolete plants and consolidate smaller operators, significant slack remains.

Global demand has shifted toward higher-value goods, renewable technologies, and service-based consumption, leaving many traditional factories underutilized. With overcapacity suppressing prices, firms face difficult choices: either scale back operations or sell at a loss. In 2025, officials in several provinces, including Hebei and Shandong, reported a resurgence in dormant projects as local governments sought to protect employment, inadvertently exacerbating supply-side imbalances.

Domestic Demand Fails to Reignite

China’s domestic market, once considered the key buffer against external shocks, has not delivered the expected lift. Consumers remain cautious amid property market weakness and uneven job recovery in the private sector. Retail sales growth slowed through 2025, while housing investment—a major driver of upstream industries such as steel, glass, and cement—continued to contract.

Industrial firms supplying the construction and consumer goods sectors have faced declining order volumes. Even in advanced manufacturing segments, such as electric vehicles and green energy components, price competition has intensified. Battery producers, for instance, have seen input costs fall but selling prices fall faster, offsetting potential margin benefits.

While the government’s emphasis on energy transition and “smart manufacturing” offers a long-term pathway to stability, these industries remain too small to fully counterbalance the drag from legacy sectors.

Comparative Regional Context

When compared with other major manufacturing economies, China’s predicament appears particularly acute. Across East Asia, economies such as South Korea and Japan also faced industrial slowdowns in 2025, but neither experienced deflation on China’s scale. South Korea’s industrial profits dipped modestly amid weaker semiconductor demand, yet energy subsidies and currency depreciation helped cushion the blow.

In Vietnam and Indonesia, meanwhile, foreign investment in export-oriented manufacturing continued to rise, partly benefiting from supply chain diversification away from China. These shifts further underscore Beijing’s challenge: as global companies optimize regional production networks, China’s traditional dominance as a low-cost exporter erodes.

Europe’s industrial heartland offers another instructive comparison. Germany, battling its own energy and geopolitical shocks, endured a manufacturing slump but maintained more stable profit margins—thanks to its diversified export base and advanced machinery sectors. In contrast, China’s greater exposure to cyclical heavy industry and construction amplifies vulnerability to both domestic and global downturns.

Policy Response and Economic Outlook

Faced with these pressures, Chinese policymakers have adopted a mix of targeted stimulus and gradual easing. The central bank maintained an accommodative stance through 2025, cutting reserve requirements and providing liquidity to banks that lend to industrial manufacturers. Local governments rolled out tax relief programs and subsidies for equipment upgrades, hoping to spur investment in high-tech and green production capacity.

Yet these efforts have struggled to restore confidence. The key obstacle remains lackluster demand—both within China and abroad. Analysts expect industrial profits to remain subdued through 2026 unless consumer spending and export orders rebound significantly. Some financial institutions predict industrial output growth of just 3% this year, a pace well below pre-pandemic averages.

Capital Flight and Investor Anxiety

The prolonged weakness has also affected investor sentiment. Foreign direct investment in manufacturing declined for a second consecutive year in 2025, as multinational firms redirected capital toward Southeast Asia, India, and Mexico. Global investors remain cautious about China’s industrial earnings prospects, citing uncertain policy direction, currency volatility, and deflation risk.

Domestically, stock market valuations of industrial firms have trended lower, reflecting expectations of tighter profit margins and slower turnover. Several listed companies in the machinery and chemical sectors issued warnings of further losses in early 2026, citing persistent cost pressures and soft order books.

Pursuing Long-Term Structural Reform

In the longer term, China’s path to industrial recovery may depend on how quickly it can accelerate structural reforms. Key priorities include shifting toward higher-value manufacturing, enhancing digital production technologies, and expanding domestic consumption through wage growth and labor mobility. The transition will not be immediate; entrenched inefficiencies and uneven regional development continue to impede progress.

Some progress is visible in strategic industries such as semiconductors, renewable energy, and electric vehicles—areas where China is investing heavily to modernize its industrial footprint. However, these sectors require massive capital outlays and yield delayed financial returns. Balancing short-term stabilization with the pursuit of innovation remains one of the government’s most formidable challenges.

A Fragile Balance for the World’s Factory

As 2026 unfolds, China’s industrial landscape stands at a crossroads. The numbers from 2025 paint a stark picture: falling profit margins, rising losses, and a deflationary environment that shows few signs of easing. Although Beijing has demonstrated resilience in past crises—such as the global financial meltdown of 2008 and the pandemic disruptions of the early 2020s—this moment is different.

The convergence of shrinking demand, structural overcapacity, and energy uncertainty has created a perfect storm. Without a broad-based revival in profitability, the world’s largest industrial ecosystem could face a prolonged period of stagnation. For now, China’s role as the “factory of the world” endures, but its foundations are under increasing strain, forcing both policymakers and companies to adapt to a markedly more uncertain era of industrial growth.