Chinese Battery Makers Tighten Grip on Global EV Market as Share Hits Record 70.4%

China’s Expanding Lead in the Electric Vehicle Battery Race

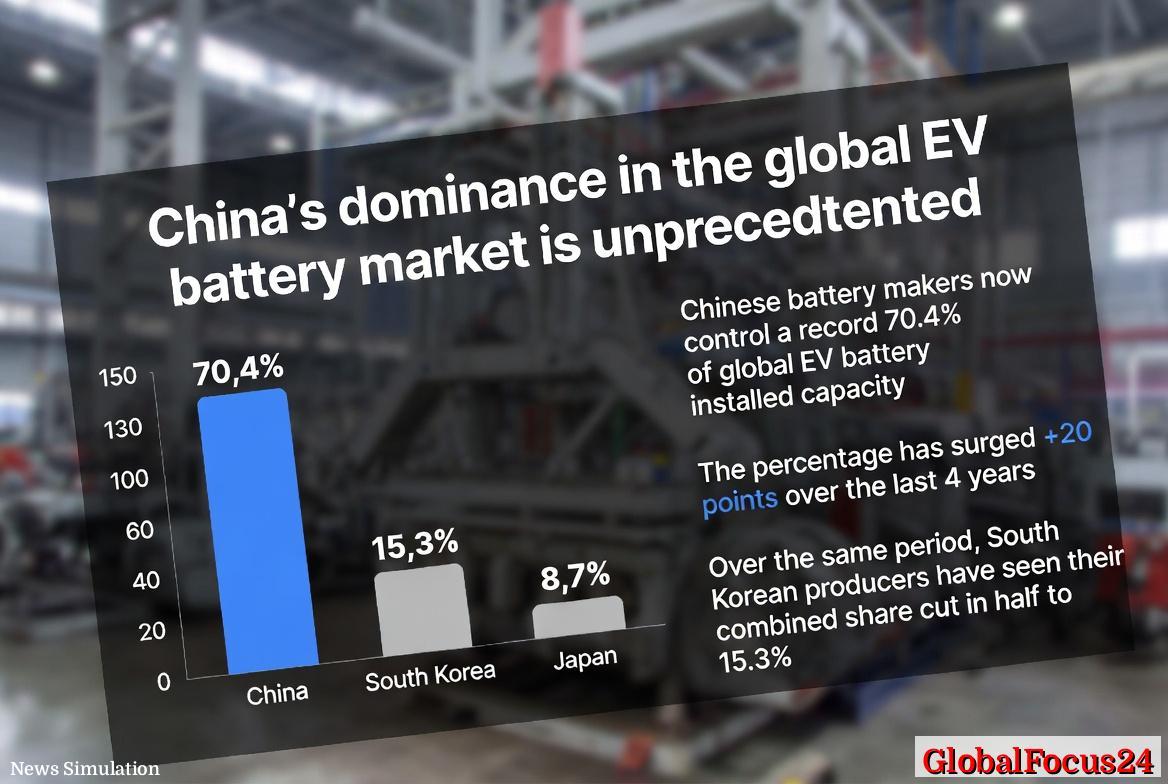

Chinese battery manufacturers have cemented their position as the undisputed leaders in the global electric vehicle (EV) battery industry, now commanding a record 70.4 percent of total installed capacity worldwide. This milestone reflects a dramatic rise of 20 percentage points in just four years, a shift that underscores the growing dominance of China in one of the most crucial sectors shaping the future of transportation and clean energy.

At the center of this dominance stands Contemporary Amperex Technology Co. Limited (CATL), which alone accounts for an astonishing 39.2 percent of the global market — a share greater than the combined total of South Korea and Japan. The rapid ascent of Chinese battery producers comes amid surging global demand for EVs and intensifying competition among automakers to secure stable supply chains for critical components.

The Steep Decline of Korean Battery Producers

While China’s rise appears unstoppable for now, it has come at the expense of rivals in South Korea. Collectively, South Korean battery makers — including major players such as LG Energy Solution, Samsung SDI, and SK On — have seen their global market share cut in half, dropping to just 15.3 percent. Four years ago, the trio commanded nearly one-third of the global market, powered by expansive supply contracts with U.S. and European carmakers.

Analysts attribute the decline to several converging factors. Chief among them is China’s aggressive scaling of production capacity, focused industrial policies, and the establishment of vast domestic ecosystems uniting manufacturers, suppliers, and end users. In contrast, South Korean firms have faced persistent cost pressures, raw material supply bottlenecks, and tightening competition in Europe and North America — regions where China’s presence has rapidly expanded despite trade restrictions.

Historical Context: From Start-Up Rivalry to Global Dominance

The story of China’s battery industry began nearly two decades ago, when companies like CATL and BYD were still emerging players competing with established Japanese giants such as Panasonic and South Korea’s LG Chem. In the early 2010s, Japan dominated global EV battery supply thanks to its pioneering role in lithium-ion technology, with Panasonic riding high on Tesla’s initial growth.

However, China’s swift industrial policy intervention — particularly under the government’s “Made in China 2025” initiative — changed the trajectory of the market. Substantial government subsidies, tax incentives, and targeted support for research and development fueled a rapid scale-up of production. By 2020, Chinese manufacturers had overtaken Japan and South Korea combined, and the gap has widened each year since.

The combination of domestic demand — from hundreds of new EV brands — and a vertically integrated supply chain centered on lithium and rare earth processing allowed China to dominate every stage of battery production, from raw material refining to cell assembly and recycling.

Market Concentration Reaches New Heights

As of 2025, six of the world’s ten largest EV battery manufacturers were Chinese firms. In addition to CATL and BYD, companies such as CALB, Gotion High-Tech, EVE Energy, and Sunwoda have emerged as major suppliers to automakers across Asia, Europe, and Latin America. These players are united by their ability to rapidly scale output, reduce cost per kilowatt-hour, and establish flexible production networks close to their automotive customers.

Data from market analysts indicate that China’s top manufacturers collectively grew their global installed capacity by an additional four percentage points in 2025, driven by new partnerships with European automakers seeking more affordable lithium-iron-phosphate (LFP) batteries. Chinese LFP cells are now favored for their safety, durability, and lower costs — key advantages as global automakers push to make EVs more affordable for mass-market consumers.

Regional Contrasts in Battery Investment

The global distribution of EV battery production highlights stark regional contrasts. China now produces more than two-thirds of all global EV batteries, followed by South Korea and Japan, which together account for about a quarter. Meanwhile, the U.S. and European Union have intensified efforts to localize battery manufacturing, but their combined market share remains below 10 percent.

South Korea’s decline has been particularly striking compared to the early 2020s, when it briefly challenged China for leadership in high-performance NCM (nickel-cobalt-manganese) chemistries. Today, many of those advantages have eroded as Chinese producers perfected mass production of both high-nickel and low-cost iron-based chemistries, giving them flexibility to serve both premium electric models and budget compact vehicles.

Japan, once the pioneering nation in lithium-ion innovation, continues to hold a niche role in supplying specialty cells for hybrids and high-end EVs. However, its global market share has stagnated amid slow expansion and high domestic production costs.

Economic Implications for the Global Supply Chain

China’s near-total dominance of EV battery manufacturing carries far-reaching implications for global industry and trade. The country’s control over refining, precursor materials, and cathode production positions it as a gatekeeper within the broader clean energy value chain. Analysts warn that this degree of concentration presents challenges for energy security and business strategy, particularly for Western automakers seeking diversified suppliers.

For economies like South Korea, Japan, and the United States, the erosion of battery market share signals a potential setback in the race to secure leadership in next-generation energy storage. Governments in these regions have responded by promoting domestic “gigafactory” initiatives and subsidizing local battery cell production, but Chinese firms are simultaneously expanding their own overseas operations — including new facilities in Hungary, Indonesia, and Morocco.

In practical terms, China’s manufacturing muscle means lower costs for automakers and potentially faster global adoption of electric vehicles. Yet it also leaves the global automotive industry increasingly dependent on Chinese technology and logistics, posing a strategic dilemma reminiscent of the semiconductor industry’s geographic concentration in East Asia.

The Role of Technological Innovation

Beyond scale, China’s edge lies in relentless innovation. CATL’s recent development of semi-solid and sodium-ion batteries demonstrates its push to reduce dependency on scarce resources like lithium, nickel, and cobalt. Meanwhile, BYD’s Blade Battery introduced a safer, more stable LFP format aimed at reducing thermal runaway risks, winning contracts with global brands like Tesla and Toyota.

In contrast, Korean and Japanese companies have traditionally prioritized high energy density and performance for premium EV models, but this segment remains smaller globally compared to mass-market vehicles. As the market shifts toward affordability and reliability, China’s focus on simplifying manufacturing processes and optimizing local supply chains has proven decisive.

Moreover, Chinese firms have taken the lead in recycling technologies, allowing materials such as lithium carbonate and cobalt sulfate to be recovered and reused at scale — a move that aligns with circular economy goals and further consolidates their cost advantage.

Global Automakers Reassess Supply Strategies

Faced with such dominance, global automakers are recalibrating their strategies. European manufacturers including Volkswagen, BMW, and Stellantis have turned to partnerships with Chinese firms to accelerate their EV transitions. In North America, Chinese investments remain sensitive amid regulatory scrutiny, yet demand for cost-effective battery cells continues to drive cross-border collaboration through joint ventures or indirect sourcing.

For South Korea’s LG Energy Solution and its peers, the path forward lies in high-performance and next-generation solid-state battery technologies, which promise greater range and safety. Achieving commercial success in those areas, however, will require significant technological breakthroughs and stable access to raw materials — areas where Chinese companies currently have built-in advantages.

A Shifting Balance in the Global Energy Transition

China’s 70.4 percent global share of EV battery capacity marks more than just a numerical milestone; it represents a broader structural realignment within the clean energy economy. With the world accelerating toward decarbonization, control over battery manufacturing translates directly into influence over how, where, and when electric vehicles become the global standard.

While other countries continue to invest heavily in domestic production and innovation, China’s early head start, scale, and cohesive policy support have entrenched its leadership. Whether this dominance endures will depend on how effectively competitors adapt to evolving technologies and market expectations.

For now, the data offer a clear message: China’s grip on the EV battery market has never been stronger, reshaping global industry dynamics as the world moves deeper into the electric age.