Buy Now, Pay Later Delinquencies Rise Sharply as Consumers Turn to Debt for Essentials

Delinquencies Surge to Record Levels

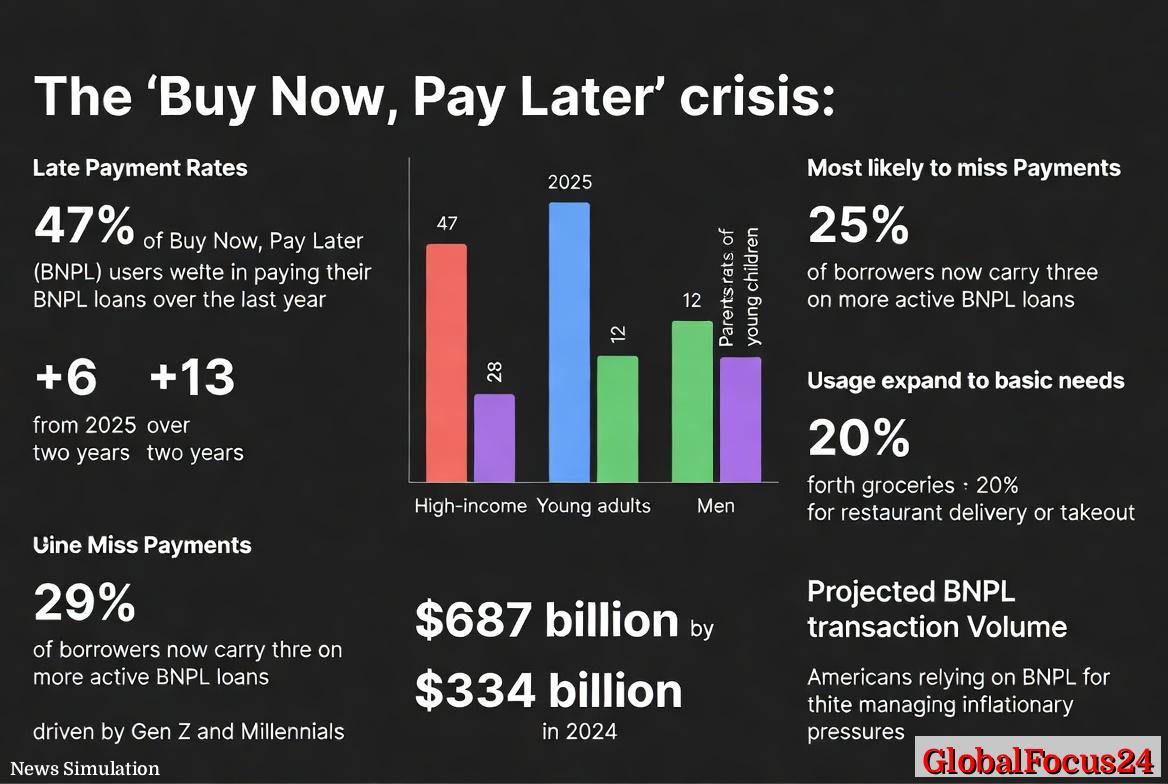

Buy Now, Pay Later (BNPL) services—once hailed as a flexible way for shoppers to spread out payments on discretionary purchases—have entered a new and more troubling chapter. Nearly half of BNPL users in the United States were late on at least one payment over the past year, with the delinquency rate reaching 47 percent. That represents a six-point increase over 2025 and a 13-point jump since 2024, signaling the growing strain on household finances amid stubborn inflation and elevated living costs.

The data point to a structural shift in how Americans use and manage short-term credit. Once concentrated in retail and travel spending, BNPL loans are now increasingly financing everyday essentials—from groceries and gas to takeout meals. As consumers stretch their budgets further, experts warn of rising financial fragility and potential reverberations through broader credit markets.

Everyday Debt Becomes a Lifeline

BNPL lending was originally marketed as a budgeting tool, enabling consumers to split mid-size purchases into manageable installments without adding credit card debt. But as economic pressures have intensified, that promise has reshaped the product’s role. According to recent reports, 29 percent of BNPL customers now use these payment plans to cover groceries, while 20 percent rely on them for restaurant delivery or takeout.

The expansion into daily necessities reveals deeper financial stress across households. Wage growth has slowed relative to inflation, while rents, utility costs, and medical expenses remain high. Traditional credit cards—long the primary safety net for American consumers—carry average interest rates exceeding 22 percent, pushing many toward interest-free or low-fee BNPL options.

What began as a convenience for e-commerce has evolved into a lending mechanism propping up day-to-day consumption. Analysts describe this trend as a “credit shift,” one that reflects both consumer resilience and vulnerability: the desire to maintain routine living standards despite tighter financial margins.

Who Is Falling Behind

The wave of missed payments has not been confined to lower-income borrowers. In fact, high-income individuals, young adults, men, and parents of young children are among the most likely to be delinquent on their BNPL loans. Economists suggest that this pattern underscores a broader normalization of debt reliance across demographic groups.

For higher earners, the problem often stems from overleveraging—holding multiple loans across different platforms. Recent data show that one in four BNPL borrowers now carry three or more active plans simultaneously, with Gen Z and Millennials leading the trend. Among younger users, BNPL's frictionless digital design and integration into social shopping platforms blur the boundaries between spending and borrowing.

Consumer advocates have raised concerns that the lack of visible costs or credit checks in BNPL can mask the true burden of these loans. Because payments are automatically deducted from debit cards or bank accounts, overdrafts and missed payments can escalate quickly. The financial fallout can range from mounting late fees to damaged credit scores, even when the initial purchase was modest.

BNPL Industry Expansion and Market Outlook

Despite rising delinquencies, the BNPL industry continues to expand rapidly. Market projections estimate total BNPL transaction volume will exceed $687 billion by 2028, more than doubling from $334 billion in 2024. The explosive growth has been driven by widespread adoption among merchants seeking to boost conversion rates and by consumers drawn to flexible terms in an era of tightening budgets.

Major players in the sector have diversified their offerings, entering partnerships with grocery chains, fuel retailers, and even healthcare providers. The technology underpinning BNPL—instant approvals, minimal friction, and AI-powered risk assessment—has lowered barriers to borrowing. Yet, as volumes surge, regulators and economists are increasingly attentive to systemic risks.

BNPL firms typically fund short-term consumer credit through longer-term financing arrangements, which can become strained if repayment rates deteriorate. While these companies argue that their models remain sound, the parallels to early credit card adoption in the late 20th century are striking. Then, as now, innovation outpaced oversight until rising defaults forced a regulatory reckoning.

Historical Context: Lessons from Past Credit Booms

The current BNPL cycle echoes earlier waves of consumer credit expansion in American history. In the 1950s, installment financing fueled car and appliance sales, igniting economic growth but eventually leading to tighter credit standards. The rise of credit cards in the 1980s similarly democratized access to borrowing but also set the stage for chronic household debt accumulation.

BNPL represents the digital-age iteration of this cycle: a technology-driven credit model embedded seamlessly into modern commerce. Its accessibility resembles the early days of subprime credit before tighter regulation followed crisis and consolidation. Economists note that what distinguishes BNPL today is its velocity—the ease and frequency with which borrowers can layer debt across multiple purchases within days or weeks.

The result is a form of invisible leverage spreading through consumer finances. Unlike credit cards, many BNPL providers do not report to major credit bureaus, leaving regulators and lenders with limited visibility into total household liabilities. That opacity complicates efforts to gauge the overall health of consumer credit markets.

The Economic Ripple Effect

The surge in BNPL delinquencies hints at broader economic ripples. High default rates can tighten liquidity for lenders, prompting stricter underwriting and reduced access to financing. For consumers, the erosion of credit reliability may curtail discretionary spending—a potential drag on retail and e-commerce sectors that have come to depend on BNPL-driven transactions.

Retailers face a delicate balancing act. On one hand, BNPL services have boosted average order values and conversion rates. On the other, rising delinquency rates threaten those very sales channels, particularly if providers tighten lending criteria or increase merchant fees to offset losses. For smaller businesses, dependent on thin margins, even slight shifts could have disproportionate effects.

If households continue substituting short-term BNPL debt for longer-term financial stability, consumer vulnerability may deepen further. That, in turn, could dampen economic growth in the second half of the decade, especially if wage growth falters or inflation reaccelerates.

Regional and Global Comparisons

The United States is not alone in facing rising BNPL stress. In the United Kingdom, Australia, and Canada, similar patterns have surfaced, though with varying intensity. Australia—where BNPL adoption first gained traction globally—has seen delinquency rates climb amid cost-of-living increases and central bank rate hikes. British regulators have already proposed new disclosure requirements and affordability checks to curb overuse among vulnerable consumers.

By contrast, European Union markets where BNPL is treated as a formal credit product under stricter lending rules have experienced more moderate rises in defaults. This contrast underscores the role that regulation and consumer education play in stabilizing emerging financial technologies.

In the U.S., regulators are beginning to follow suit. The Consumer Financial Protection Bureau has called for standardizing disclosure practices and ensuring that BNPL debts are incorporated into credit reporting systems. Industry leaders, while cautious of heavier regulation, increasingly acknowledge the need for transparency to maintain consumer trust and institutional confidence.

Inflation, Employment, and the Debt Balancing Act

The interplay between inflation, employment, and short-term debt will define the next phase of the BNPL story. Even with steady job growth, real wages have not kept pace with household expenses. The reliance on BNPL for essentials reveals that many consumers are managing not prosperity but precarity—assembling temporary financial bridges month by month.

If inflation pressures persist through 2026, more households may treat BNPL not as a convenience but as a survival strategy. That could distort both consumer sentiment and traditional credit metrics, obscuring early warnings of financial distress. Conversely, a sustained decline in inflation coupled with real income growth could stabilize repayment behavior and restore BNPL’s original niche as a budgeting tool rather than a borrowing crutch.

The Future of Consumer Credit

BNPL’s trajectory over the next few years will test how quickly financial ecosystems can adapt to new forms of debt. As technology and consumer expectations evolve, so too must credit infrastructure—balancing innovation with prudence.

Industry observers predict consolidation ahead. Larger firms may absorb smaller or riskier providers as capital costs rise, mirroring the historic consolidation of credit card issuers in the 1990s. Meanwhile, data-sharing agreements and enhanced transparency could bring BNPL closer to traditional credit frameworks without undermining its appeal.

Ultimately, the surge in BNPL delinquencies serves as both warning and opportunity. It highlights the fragility of household finances after years of inflation and uneven recovery, but it also signals the chance to build a more modern, consumer-centric financial system—one that supports flexibility without sacrificing responsibility.

As the nation’s debt habits evolve, the question facing lenders and policymakers alike is no longer whether consumers will borrow to meet their needs, but how sustainable that borrowing will be in the years ahead.