Top 20% of U.S. Households Command Record $49.1 Trillion in Equities as Wealth Gap Widens

Surge in Equity Ownership Reaches Historic Highs

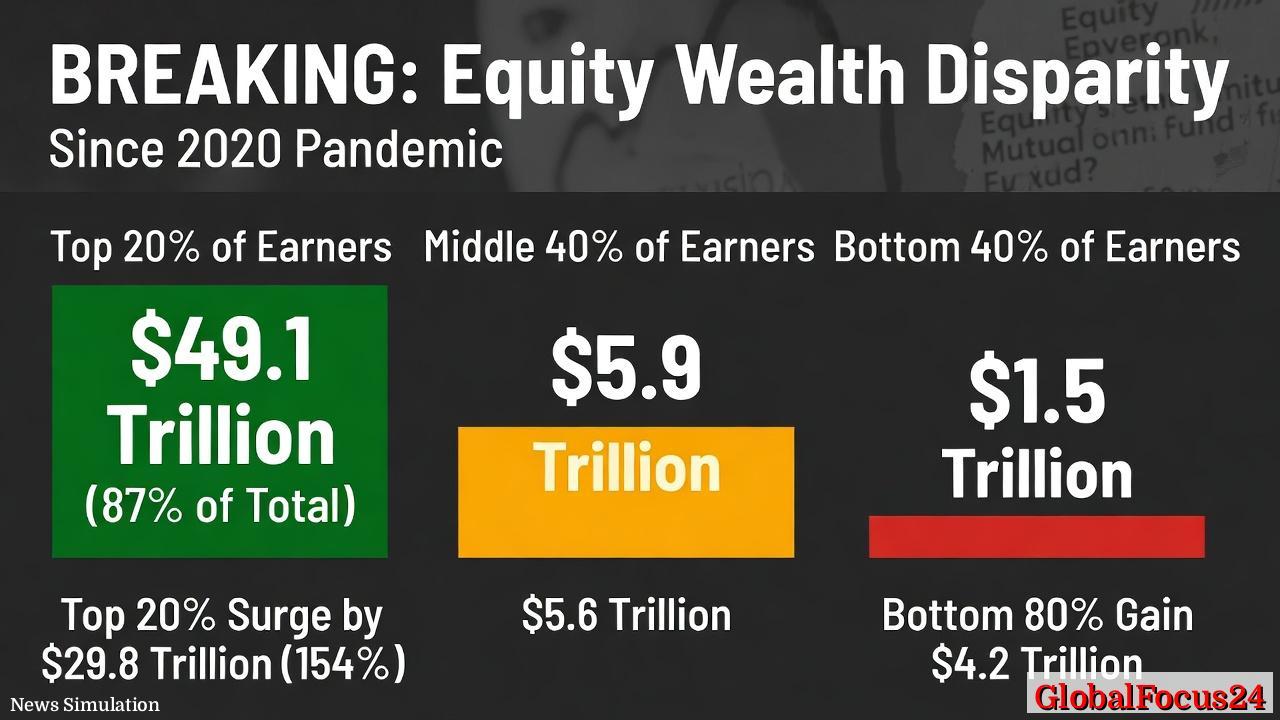

The concentration of wealth in U.S. financial markets has reached a new peak, with the top 20 percent of earners now holding a record $49.1 trillion in equities and mutual funds. This figure represents approximately 87 percent of all such holdings, underscoring a dramatic imbalance in asset ownership that has accelerated in the years following the COVID-19 pandemic.

By contrast, the middle 40 percent of households collectively own $5.9 trillion in equities, while the bottom 40 percent hold just $1.5 trillion. The disparity highlights a long-standing structural divide in access to financial markets, one that has deepened as equity valuations surged over the past five years.

Since early 2020, the top quintile has added $29.8 trillion in equity wealth, a 154 percent increase. Over the same period, the bottom 80 percent combined gained only $4.2 trillion, meaning the top group captured roughly six times more wealth in absolute dollar terms.

Pandemic-Era Policies and Market Dynamics

The sharp rise in equity wealth among higher-income households is closely tied to the extraordinary market conditions that followed the onset of the pandemic. In 2020, central banks introduced aggressive monetary easing measures, including near-zero interest rates and large-scale asset purchases, which drove investors toward equities in search of returns.

Major stock indices rebounded rapidly after the initial pandemic shock, fueled by fiscal stimulus, corporate earnings resilience, and a surge in technology sector valuations. Households already invested in financial markets—predominantly those in the top income brackets—benefited disproportionately from this rebound.

At the same time, lower-income households faced more immediate economic pressures, including job losses, reduced hours, and rising living costs. While stimulus payments and expanded unemployment benefits provided temporary relief, they did not translate into sustained participation in equity markets at the same scale.

Long-Term Trends in Wealth Concentration

The current distribution of equity ownership reflects decades of gradual concentration. Since the 1980s, financial deregulation, the growth of retirement accounts tied to market performance, and the increasing importance of capital gains have all contributed to expanding wealth at the top.

Higher-income households are more likely to hold diversified portfolios, participate in employer-sponsored retirement plans, and invest in individual stocks and mutual funds. These advantages compound over time, especially during prolonged bull markets.

Meanwhile, lower- and middle-income households tend to allocate a larger share of their income to essential expenses such as housing, healthcare, and education, leaving less capacity for investment. Even when participating in the market through retirement accounts, their exposure is often smaller and more vulnerable to withdrawals during financial stress.

Economic Implications of Uneven Asset Growth

The widening gap in equity ownership carries significant implications for the broader economy. Consumer spending patterns, for instance, are influenced by wealth distribution. Higher-income households typically save a larger portion of their gains, while lower-income households are more likely to spend additional income, supporting economic activity.

As a result, when wealth gains are concentrated at the top, the stimulative effect on the economy may be less pronounced than if gains were more evenly distributed. This dynamic has drawn attention from economists analyzing post-pandemic growth trends.

In addition, disparities in financial asset ownership can affect long-term financial stability. Households with limited assets are more vulnerable to economic shocks, while those with substantial portfolios have greater resilience and flexibility.

Housing, Inflation, and Barriers to Entry

One of the key barriers preventing broader participation in equity markets is the rising cost of living. Housing prices have increased significantly in many regions, particularly in urban and coastal areas, requiring households to allocate more income toward mortgages or rent.

Inflationary pressures in recent years have further constrained disposable income, particularly for lower- and middle-income families. With less money available for savings or investment, entering the stock market becomes more difficult.

In contrast, wealthier households often benefit from existing asset appreciation, including both real estate and financial holdings, reinforcing their ability to invest further.

Regional Comparisons and Global Context

The concentration of equity ownership in the United States is more pronounced than in many other advanced economies, though similar trends are visible globally. In Europe, for example, equity ownership tends to be more evenly distributed due in part to stronger social safety nets and different retirement systems, though overall participation rates are lower.

In emerging markets, equity ownership is often limited to a small segment of the population, with large portions of wealth held in real assets such as land or informal businesses. However, as financial markets develop and digital investment platforms expand, participation is gradually increasing.

Within the United States, regional disparities also play a role. Households in high-income metropolitan areas—such as those in California and the Northeast—are more likely to hold significant equity investments, reflecting higher average incomes and greater access to financial services.

The Role of Technology and Retail Investing

The past decade has seen a rise in retail investing platforms, making it easier for individuals to buy and sell stocks with minimal fees. During the pandemic, these platforms experienced a surge in new users, particularly among younger investors.

While this trend has expanded access to financial markets, its impact on overall wealth distribution remains limited. Many new investors enter the market with relatively small amounts of capital, and their gains, while meaningful at the individual level, do not significantly alter aggregate ownership patterns.

Nevertheless, the democratization of investing tools represents a shift in how individuals engage with financial markets, potentially laying the groundwork for broader participation in the future.

Corporate Ownership and Institutional Influence

Another factor contributing to the concentration of equity wealth is the role of institutional investors, including pension funds, mutual funds, and hedge funds. While these entities manage assets on behalf of a wide range of individuals, the underlying ownership often remains skewed toward higher-income households.

Corporate stock buybacks have also played a role in boosting share prices, benefiting existing shareholders. Companies have increasingly used excess cash to repurchase shares, reducing supply and increasing earnings per share, which can drive stock valuations higher.

These dynamics further amplify gains for those already invested in the market, reinforcing existing wealth disparities.

Historical Parallels and Market Cycles

Periods of rapid asset appreciation have historically coincided with increased wealth concentration. Similar patterns were observed during the late 1990s technology boom and the pre-2008 housing market expansion.

However, market downturns can temporarily narrow wealth gaps, as asset prices decline and disproportionately affect those with larger holdings. The extent and duration of such effects depend on the severity of the downturn and the pace of recovery.

The post-2020 period stands out for both the سرعت and scale of equity market gains, driven by unprecedented policy responses and technological shifts that reshaped economic activity.

Looking Ahead: Structural Challenges and Opportunities

The current distribution of equity ownership raises questions about long-term economic inclusivity and financial resilience. Expanding access to investment opportunities, improving financial literacy, and addressing structural barriers to saving are frequently cited as potential pathways to broader participation.

At the same time, market performance will continue to play a central role in shaping wealth dynamics. As interest rates, inflation, and global economic conditions evolve, the trajectory of equity markets—and who benefits from them—remains a critical area of focus.

For now, the data points to a clear reality: the gains of the past several years have been heavily concentrated among the highest earners, reinforcing a trend that has been decades in the making.