US Labor Market Stabilizes on a Fewer-Jobs Breakeven Path, Signaling Structural Shifts

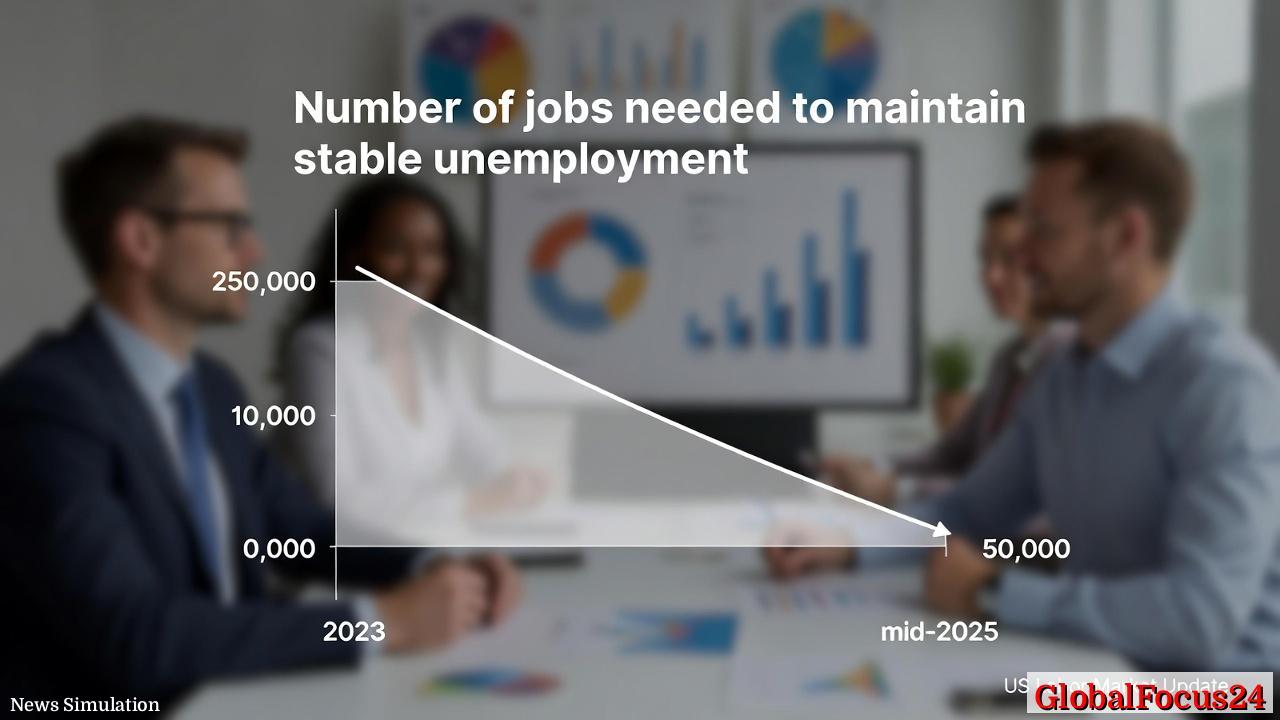

In a notable shift for the U.S. labor market, economists say the breakeven rate of household employment growth—the number of new jobs required each month to keep the unemployment rate from rising—has fallen dramatically. Estimates place the current breakeven around 50,000 jobs per month, a stark contrast to the 200,000–250,000 figure observed in 2023. The change, driven largely by a markedly slower pace of labor-force entrants, points to a broad reconfiguration of the country’s employment dynamics and has wide-ranging implications for workers, businesses, policymakers, and regional economies.

Historical context: a gradual ride to labor-market normalization The United States has long weathered cycles of job growth, unemployment fluctuations, and shifts in the labor force. After the Great Recession, job creation accelerated with strong productivity gains and a gradually expanding workforce. The post-pandemic era introduced new frictions: rapid digitization, reallocation across sectors, and evolving immigration patterns that influence the available pool of workers. In recent years, immigration levels have fluctuated due to policy changes, global events, and labor-market demand, shaping the size and speed of entrants into the labor force. That slower influx, combined with demographic trends such as aging workers and changing participation rates, has contributed to a lower breakeven threshold for sustaining current unemployment levels.

Economic impact: what a lower breakeven means for growth and stability

- A smaller required pace of job creation can translate into greater systemic stability. When the labor market can absorb new entrants more gradually, the risk of acute unemployment spikes during downturns diminishes, potentially reducing the amplitude of business-cycle swings.

- For employers, this condition can ease the pressure to hire aggressively to keep unemployment in check. Firms may gain latitude to focus on productivity, training, and longer-term workforce planning, rather than aggressive headcount expansion in response to cyclical demand.

- For workers, a lower breakeven rate can influence wage dynamics and labor mobility. If the market no longer requires rapid job creation to maintain unemployment near current levels, wage pressure may evolve differently across sectors, with skills aligning more closely to persistent demand rather than opportunistic hiring surges.

- On the policy front, a slower inflow of entrants and a steadier unemployment rate can alter monetary and fiscal considerations. Central banks and government agencies may recalibrate expectations about employment elasticity, the pace of inflation cooling, and long-run potential output.

Regional context: why some areas feel the shift more than others The United States is not monolithic when it comes to labor-market conditions. Regions with robust immigration inflows, strong manufacturing or technology bases, or dynamic service sectors may experience different breakeven dynamics than areas facing aging demographics or slower population growth. Several regional trends have emerged:

- Coastal metros with diversified economies often exhibit resilience when job creation slows, thanks to their broader talent pools and higher initial employment levels.

- Rural and exurban counties tied to industries susceptible to automation or cyclical demand bear watchful eyes on labor-force participation and long-term employment prospects.

- Historically immigrant-heavy regions may see a more pronounced impact on the overall breakeven rate, given the direct contribution of new entrants to the labor supply.

Structural change versus cyclical movement: interpreting the data Analysts emphasize that the current breakeven shift reflects structural changes rather than a temporary blip. While cyclical demand fluctuations will always influence monthly job totals, the persistent lowering of required new jobs to sustain unemployment signals a more permanent recalibration in the economy’s growth trajectory. Contributing factors include:

- Demographic dynamics: an aging workforce and evolving retirement patterns reduce the pool of readily available entrants without necessarily triggering immediate unemployment volatility.

- Participation rate adjustments: changes in labor-force participation by prime-age workers, students, caregivers, and those returning to work after layoffs influence the overall employment baseline.

- Productivity and automation: continued gains in output per worker can offset slower hiring, allowing the economy to grow even when job growth slows.

- Global labor-market shifts: immigration policy, border dynamics, and international labor mobility indirectly shape domestic hiring pace by determining the size of the pool available to fill openings.

Economic indicators to watch

- Unemployment rate: stability in unemployment while job creation slows may indicate a re-controlled labor market, but sustained weakness could suggest hidden slack or regional disparities.

- Labor-force participation: trends in participation help explain why breakeven needs have fallen; a rising participation rate could push the breakeven higher as more people enter seeking work.

- Wage growth: the relationship between the lower breakeven rate and wage pressures will reveal how employers price skills in a slower-hiring environment.

- Sectoral employment: knowledge of which industries are expanding versus contracting will illuminate where the most durable opportunities lie and where risks are concentrated.

Regional comparisons: a closer look

- Technology and professional services hubs: these areas often experience tighter labor markets with higher qualification requirements. A lower breakeven rate may align with continued demand for specialized skills, yet competition for talent can keep wage growth firm.

- Healthcare and social assistance: long-standing employment growth in these sectors provides a buffer against shocks, as demand trends are less sensitive to economic cycles and more tied to demographic needs.

- Manufacturing and logistics corridors: supply-chain realignments and reshoring efforts can influence regional job creation, potentially moderating or amplifying breakeven shifts depending on automation and investment cycles.

- Tourism and hospitality belts: these regions may be more exposed to seasonal patterns, with a breakeven rate that fluctuates based on visitor demand and labor-force availability.

Public reaction: how households perceive the shift In communities across the country, households have interpreted the evolving labor-market dynamics in ways that color daily life. Some workers view the stability of unemployment as a reassuring backdrop against which to plan education, training, or career transitions. Others worry about wage growth not keeping pace with living costs or about regional disparities in opportunities. Employers, meanwhile, weigh the benefits of investing in workforce development, upskilling programs, and retention strategies to weather periods of slower hiring.

Historical comparisons: how today stacks up against past cycles Looking back across decades, the current breakeven trajectory shares similarities with periods following major immigration reforms or macroeconomic normalization, where the labor supply adjusts gradually to a new equilibrium. Yet the combination of slower natural growth in entrants, continued productivity gains, and sectoral transformations creates a unique moment in time. The result is a labor market that can endure modest shifts in job creation without triggering sharp unemployment spikes, a sign of a more resilient, albeit more complex, economy.

Policy considerations: guiding a stable path forward

- Workforce development: targeted training and apprenticeship programs can align skills with persistent demand, helping workers transition into growing sectors even as hiring pace cools.

- Immigration policy implications: policymakers might weigh how immigration levels influence the labor supply and subsequent breakeven dynamics, balancing economic needs with broader social considerations.

- Regional development: investments in infrastructure, education, and industry-specific incentives can stimulate job creation where it matters most, supporting balanced regional growth.

- Inflation and monetary policy: central banks will monitor how a slower job-creation pace interacts with inflation trajectories, adjusting interest-rate paths to maintain price stability without sacrificing growth.

Bottom line: a nuanced evolution rather than a drama of disruption The current landscape suggests a labor-market evolution rather than a dramatic upheaval. A lower breakeven rate for employment growth signifies that the U.S. economy can maintain unemployment around current levels with fewer fresh job openings each month. This development reflects deeper structural adjustments—shaped by demographics, participation, and productivity—rather than a one-off shock. For workers, businesses, and policymakers, the focus shifts toward sustainable skill development, efficient labor-market matching, and regional strategies that capitalize on enduring demand patterns.

Public interest remains high as communities watch for how these shifts translate into wages, opportunities, and long-term economic health. While thenumbers may suggest a calmer rhythm, the underlying forces at work point to a dynamic balance between supply, demand, and the evolving texture of work in America.