U.S. Inflation Expectations Surge to Three-Year High as Markets Enter Tumultuous Phase

Inflation Jumps Back Into Focus

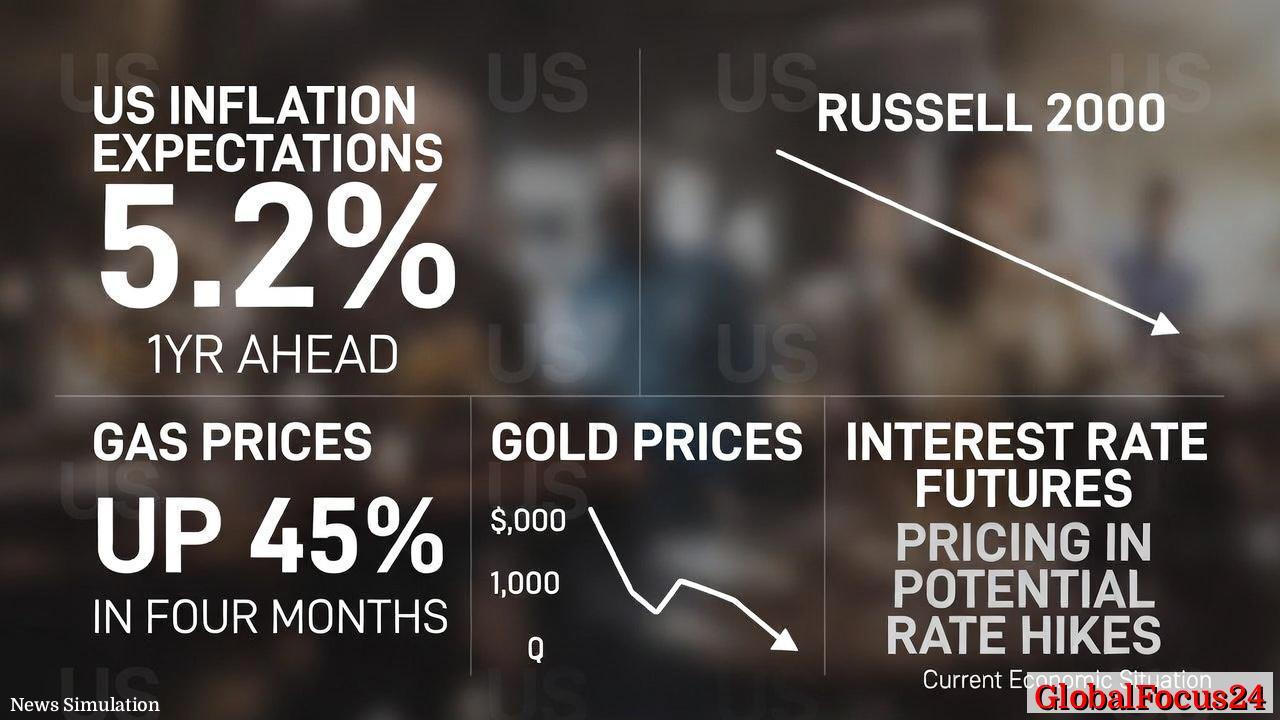

The U.S. economy is facing a renewed wave of inflationary pressure as consumer and market expectations for future price growth have climbed to 5.2 percent — the highest level in three years. This unexpected surge marks a sharp reversal from the steady cooling trend seen through much of 2024 and early 2025. The move has reignited concern that the Federal Reserve could take a more aggressive stance on interest rates in the coming months.

Over the past four months, consumer costs have steadily climbed, led by a 45 percent jump in gasoline prices. Higher transportation and energy costs have rippled across sectors, from manufacturing and agriculture to retail and logistics. For consumers already burdened by elevated housing costs, the climb in everyday expenses has magnified financial strain and weakened purchasing power across wide segments of the population.

The Russell 2000 Enters Correction Territory

Amid the resurgence of inflation fears, the Russell 2000 index — widely seen as a barometer for small-cap U.S. companies — has officially entered a technical correction, falling more than 10 percent from its recent peak. The sell-off highlights growing investor unease about tighter financial conditions and the potential impact of higher borrowing costs on smaller, domestically focused businesses.

Historically, small-cap equities tend to underperform during late-cycle inflationary periods, when rising costs and slowing credit availability weigh on margins. The last time the index fell into correction territory, in 2022, similar inflation anxieties prompted a swift repricing across asset classes. Analysts now worry that this emerging correction could foreshadow broader market volatility through mid-2026.

Rate Hike Expectations Return

Interest rate futures are now signaling a notable shift in market sentiment. Traders are pricing in additional rate hikes as early as the next two Federal Reserve meetings, suggesting that policymakers may confront renewed pressure to curb inflation momentum.

While the Federal Reserve has not yet issued forward guidance indicating an immediate tightening move, recent data may alter its tone. Wage growth has remained resilient, unemployment sits near multi-decade lows, and service-sector inflation has shown limited signs of moderation. Economists note that if inflation expectations continue to rise, the Fed may face a more complex balancing act between stabilizing prices and preventing an unnecessary slowdown in growth.

Energy Price Shock Drives Momentum

The near-45 percent jump in gasoline prices since late 2025 has caught both policymakers and consumers off guard. Several factors have driven the surge: reduced OPEC+ output, seasonal refinery maintenance across the U.S. Gulf Coast, and geopolitical disruptions in Eastern Europe and the Middle East. Domestic crude inventories have also declined sharply in recent weeks, amplifying the upward pressure on fuel costs.

Energy price spikes often have an outsized impact on inflation expectations because gasoline and heating costs directly affect consumer sentiment and transportation spending. In previous cycles, such as during the 2008 and 2022 energy shocks, elevated fuel costs contributed significantly to inflation persistence even after broader price growth began to slow.

Gold Retreats Despite Inflation Fears

In a surprising twist, gold — historically a safe haven during times of inflation — has fallen sharply. Prices have dropped roughly $1,000 per ounce from their record highs set earlier this year, marking one of the steepest declines in over a decade. The pullback suggests that investors are shifting toward cash and high-yield bonds amid expectations of higher interest rates, which tend to diminish gold’s appeal by raising the opportunity cost of holding non-yielding assets.

Analysts describe the move as a sign of market uncertainty rather than confidence. Rising yields and inflation typically pull gold in opposite directions: while inflation boosts demand for hedges, higher yields strengthen the dollar and make gold less attractive to institutional investors. If rate hikes materialize later this year, bullion prices may face continued downward pressure through the third quarter.

Housing and Mortgage Rates Hit New Highs

Mortgage rates have surged more than 50 basis points in recent weeks, reaching their highest level of 2026. The upward climb has pushed housing affordability to its lowest point in four decades, particularly in high-demand markets such as California, Texas, and Florida. Home sales have slowed markedly since January, while refinancing activity has nearly vanished.

This tightening housing picture evokes parallels with earlier phases of the 1980s and early 2020s, when rapid jumps in mortgage rates pressured new buyers and cooled construction activity. Real estate experts note that continued rate escalation could delay recovery in residential investment, which had shown signs of revival late last year before the latest spike in borrowing costs.

Economic and Regional Ripple Effects

The impact of these trends has not been uniform across the country. Energy-producing regions, including Texas, North Dakota, and parts of the Rockies, have benefited from higher oil and gas prices. In contrast, manufacturing-heavy states in the Midwest and Great Lakes region face higher input costs and tighter credit conditions. Coastal states, where the cost of living is already steep, are seeing accelerated rent increases and rising transportation expenses that strain household budgets.

Compared with Europe and Asia, the U.S. inflation rebound stands out for its intensity and speed. While the eurozone has also seen moderate price growth amid energy imports and labor shortages, its inflation expectations remain near 3 percent. In Japan, monetary policymakers continue to grapple with the opposite challenge — sustaining inflation near their target despite recent wage increases. The U.S. economy’s resilience has kept domestic demand high, but that same strength now fuels concern that inflation could become embedded once more.

Historical Perspective on Economic Resets

Episodes of surging inflation expectations often precede structural economic shifts. The sharp inflation bursts of the late 1970s and early 1980s reshaped monetary policy frameworks worldwide, leading to a decades-long emphasis on price stability. More recently, the post-pandemic inflation wave from 2021 to 2023 tested the limits of fiscal stimulus and supply chain resilience.

The current moment carries echoes of those transitions. While the U.S. is not in a stagflationary environment, the combination of high fuel costs, elevated rates, and weakening equity sentiment points to a complex phase of adjustment. Economists describe this as a “mini-reset,” in which market expectations and policy responses recalibrate to a new equilibrium.

Investor Response and Market Sentiment

Investors have grown increasingly cautious, rotating away from growth and speculative stocks toward dividend-paying sectors, utilities, and cash equivalents. The yield on two-year Treasury notes has climbed in tandem with futures pricing, signaling expectations for a protracted period of higher policy rates.

At the same time, volatility indexes have crept upward, reminiscent of conditions during 2022’s mid-year inflation panic. Asset managers report renewed client inquiries about inflation-protected securities and short-duration bond funds — a defensive stance suggesting that investors see more short-term turbulence ahead.

Business and Consumer Outlook

Corporate leaders have begun warning of higher input costs cutting into profit margins for the second half of the year. Consumer-facing brands in retail, dining, and travel industries report that spending remains solid but increasingly concentrated among higher-income households. In lower and middle-income segments, discretionary purchases have slowed, leading to concerns of uneven economic resilience.

Consumer confidence data reflects that divide. Surveys show a decline in expectations for real income growth even as job availability remains high. Economists caution that if inflation expectations continue to rise faster than wages, household sentiment could weaken further, potentially softening demand later in 2026.

Conclusion: A Period of Economic Crossroads

The convergence of rising inflation expectations, higher energy prices, falling gold values, and tightening credit conditions signals that the U.S. economy is entering another pivotal phase. With the Russell 2000 index in correction territory and mortgage rates hitting fresh highs, the balance between growth and stability has become increasingly delicate.

For policymakers, the challenge lies in reinforcing confidence while addressing structural inflation pressures without derailing the labor market or triggering financial strain. For households and investors, the message is equally clear: the era of low inflation and easy money appears definitively behind us. As 2026 unfolds, the pace and direction of these changes will define not only the trajectory of U.S. markets but also the contours of the next economic cycle.