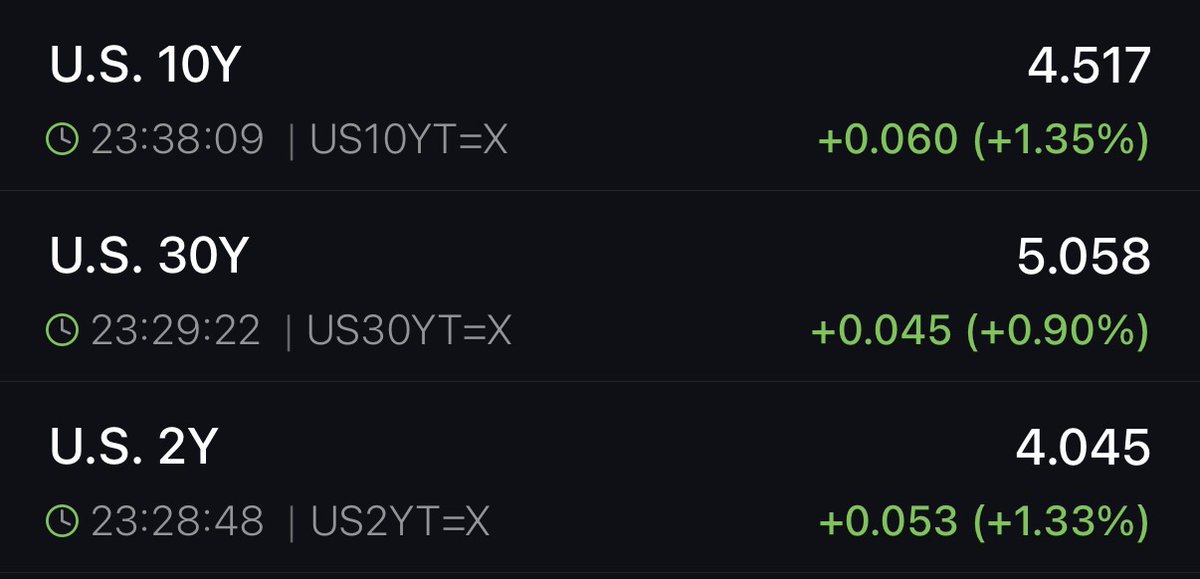

U.S. 10-Year Treasury Yield Breaks Above 4.50% as Markets Assess Higher-For- Longer Path

The benchmark U.S. 10-year Treasury yield surged above 4.50% for the first time since mid-2025, signaling renewed investor expectations of a higher-for-longer interest rate regime and prompting a fresh wave of analysis across financial markets, borrowing costs, and regional economies. The move arrived as inflation pressures persist and economic data reinforce the possibility that the Federal Reserve will maintain higher policy rates for longer than previously anticipated. Market participants are weighing the implications for consumer financing, corporate investment, and the resilience of sectors sensitive to interest rates, including housing and large-scale infrastructure projects.

Historical context: cycles, rates, and the transmission of policy

The 10-year note is a benchmark for long-term interest rates in the U.S. financial system. Its yield reflects the market’s expectations for future inflation, growth, and monetary policy. Historically, crossing the 4.50% threshold has tended to accelerate the repricing of risk across asset classes. In the wake of tight monetary policy in the previous cycle, yields climbed to multi-year highs as the Fed raised rates to curb inflation. The current move carries echoes of those earlier periods, when higher yields translated into higher borrowing costs for households and businesses, thereby shaping investment decisions and economic sentiment.

Investors historically scrutinize the relationship between government debt yields and broader financial conditions. When yields rise, the cost of financing for corporations generally increases, which can dampen capital expenditure and slow stock market valuations due to elevated discount rates. For homeowners and homebuyers, higher yields typically translate into higher mortgage rates, a dynamic that reduces housing affordability and can temper demand in regional real estate markets. The recent advance above 4.50% renews questions about how quickly borrowing costs will adjust to shifting inflation expectations and the trajectory of monetary policy.

The current context includes persistently elevated inflation and a data pattern that has kept market participants vigilant about policy stances. Inflation has remained elevated enough to justify ongoing scrutiny of price stability measures, even as some supply-chain disruptions ease and labor market dynamics show resilience. This combination supports a scenario in which the Fed could adjust its pace of rate increases or holdings, balancing the goal of price stability with the need to avoid a recessionary impulse.

Economic impact: borrowing costs, consumer finance, and business investment

- Mortgage and housing markets: A 10-year yield above 4.50% tends to push 30-year fixed mortgage rates higher, which can cool demand for new home purchases and refinancing activity. Regional housing markets, especially those with high affordability pressures, may experience slower price growth or modest price corrections as financing becomes pricier and monthly payments rise. Builders and developers may adjust project timelines or scale based on anticipated demand shifts, affecting regional construction activity.

- Corporate borrowing: Higher long-term yields raise the cost of issuing corporate bonds and financing large capital projects. Companies may reassess expansion plans, acquisitions, and share repurchase programs in light of elevated hurdle rates. Financial markets, including equities, may price in a higher cost of capital, potentially constraining earnings growth expectations and influencing sector performance—particularly for rate-sensitive industries such as technology, utilities, and industrials.

- Consumer financing: Consumers relying on unsecured credit, auto loans, and other debt instruments can feel a ripple effect from a higher-yield environment. If lenders pass through higher funding costs, household budgets may tighten, reducing discretionary spending and impacting sectors like consumer durables and retail. In regions with elevated household debt levels, the sensitivity to rate moves can be more pronounced.

- Investment and savings behavior: Higher yields generally attract savers searching for income, potentially shifting preferences toward fixed-income investments, money market funds, and other rate-enhanced vehicles. This can influence capital flows, currency dynamics, and regional investment patterns, including cross-border funding for infrastructure and development projects.

Regional comparisons: how different areas feel the yield shift

- Coastal metros with high housing costs: Regions with expensive housing markets often experience a more pronounced effect from rising mortgage rates, potentially slowing price appreciation or increasing inventory turnover as buyers recalibrate budgets.

- Inland and mid-sized cities: Areas with relatively affordable housing might see steadier demand, though rising borrowing costs can still temper investor activity in multifamily and commercial real estate, especially if cap rates compress or financing becomes costlier.

- Resource-rich regions: Areas dependent on energy or commodity cycles may experience mixed effects. Higher financing costs can impact capital-intensive projects, while commodity price cycles can offset some borrowings’ impact through cash flows and investment appetites.

- Small businesses and local lenders: In smaller markets, banks and regional lenders may respond to higher yields with adjusted lending standards, influencing small business expansion, payroll growth, and local entrepreneurship.

Comparisons to prior cycles: lessons from past rate regimes

The 4.50% area is a familiar psychological and practical milestone for investors and borrowers. During prior periods of rate normalization, certain patterns emerged:

- Equity markets often faced near-term volatility as discount rates rose, compressing valuations, particularly for growth-oriented equities with longer-duration cash flows.

- Mortgage markets reacted quickly to shifts in the yield curve, with longer-term rates affecting affordability and demand for housing and refinancing.

- Policy communication from the Federal Reserve, guided by inflation data and labor market strength, played a pivotal role in shaping expectations and market volatility.

While past cycles are not a perfect predictor of future results, the current environment shares common threads: inflation persistence, expectations of policy adjustments, and the sensitivity of consumer and corporate balance sheets to higher funding costs.

Public reaction and the broader financial landscape

Public sentiment often shifts when major benchmark yields cross key thresholds. Homebuyers and renters may feel urgency as monthly payments rise, while investors reallocate portfolios toward assets perceived as better hedges against higher rates. The market’s handling of the move above 4.50% demonstrates ongoing vigilance about the path of inflation, the pace of Fed policy, and the resilience of the economy in a higher-rate environment.

Analysts note that the yield move is not occurring in isolation. It interacts with other market indicators, including wage growth, consumer spending, supply chain normalization, and international monetary conditions. The sensitivity of regional economies to borrowing costs suggests that the macro impact will vary by locality, underscoring the importance of granular, data-driven assessments for policymakers, lenders, and business leaders.

Policy considerations: what to watch next

- Inflation trajectories: Any deceleration or acceleration in core inflation will significantly influence the Fed’s policy stance. Persistent price pressures could reinforce vigilance, while cooling inflation might allow for a less aggressive stance.

- Labor market data: Employment metrics, including wage growth and unemployment rates, will factor into the credibility of price stability goals and policy timing.

- Global rates and capital flows: International monetary conditions influence U.S. yields and demand for U.S. Treasuries. Global investors often balance risk and return across currencies, sovereign debt, and relative inflation expectations.

- Economic growth indicators: GDP growth, manufacturing activity, and consumer confidence will shape the anticipated trajectory of policy rates and the broader borrowing environment.

Looking ahead: potential scenarios for the coming quarters

- Moderation scenario: Inflation eases alongside sustained growth, allowing the Fed to calibrate policy without sudden shifts. Long-term yields could stabilize as markets price in a slower pace of rate increases.

- Tightening scenario: If inflation remains persistent and labor markets stay strong, policymakers may opt for a measured continuation of higher rates, keeping long-term yields elevated and influencing credit cycles across sectors.

- Adjustment scenario: Market expectations could adjust more quickly if data indicates a softer-than-expected inflation picture or if external shocks alter the risk assessment, potentially narrowing spreads between Treasuries and other fixed-income instruments.

Conclusion: navigating a higher-rate environment

The rise of the U.S. 10-year Treasury yield above 4.50% marks a notable moment for investors, borrowers, and policymakers. It reinforces the central theme of a market navigating a higher-for-longer trajectory, with implications spanning housing affordability, corporate investment, consumer finance, and regional economic health. As the data flow continues, households and businesses will watch inflation, growth signals, and policy communications closely, adapting their plans to the evolving landscape of interest rates and financial conditions. The coming weeks are likely to bring renewed scrutiny of upcoming inflation readings, labor market developments, and the Fed’s guidance, all shaping the tempo of borrowing costs and the broader economic outlook.