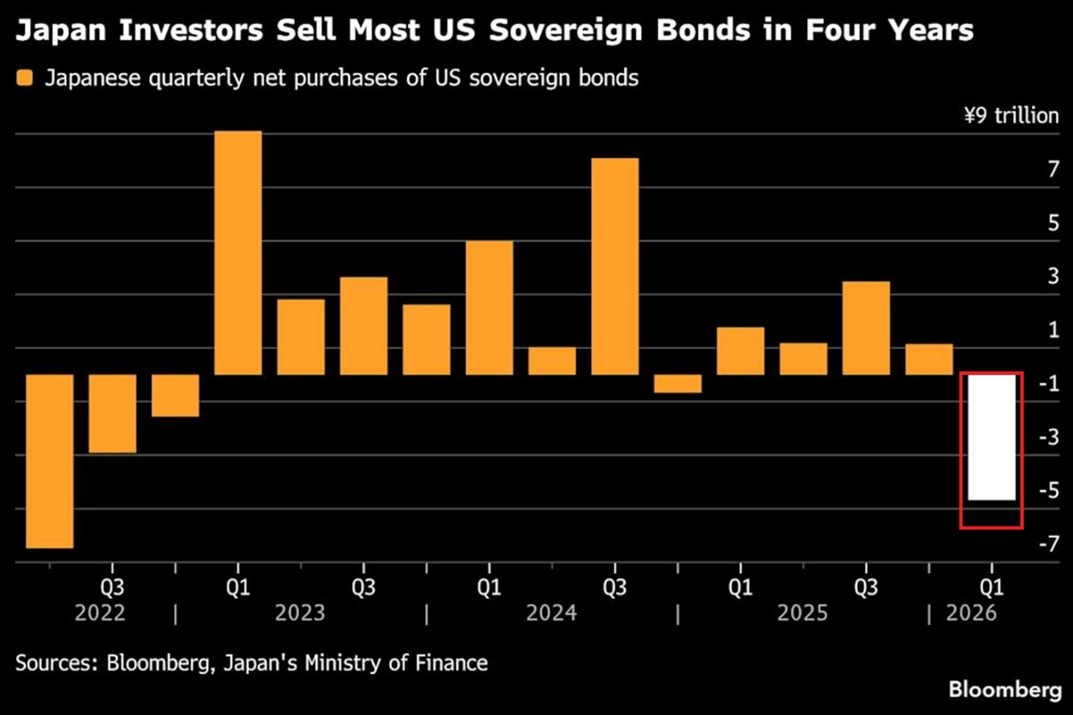

Japanese Investors Sell Record $29.6 Billion in US Debt in Q1 2026

Historical context underscores a pivotal shift in cross-border capital flows as Japanese investors recorded a sweeping exit from several U.S. debt markets in the first quarter of 2026. The $29.6 billion net sale encompassed U.S. Treasuries, agency debt, and local authority debt, marking the largest quarterly divestment since mid-2022 and the first net outflow since late 2024. The move arrived amid shifting expectations for global interest rates, inflation trajectories, and the evolving risk calculus of major international asset holders.

A closer look at the breakdown reveals a multi-faceted dynamic. Treasury securities, with their role as a global benchmark for risk-free yields, have endured a period of elevated volatility as central banks recalibrate policy directions in response to inflation and growth signals. Agency debt, which includes mortgage-backed securities and debt from government-sponsored enterprises, has also faced headwinds tied to changes in mortgage market fundamentals, liquidity conditions, and the broader appetite for riskier fixed-income instruments. Local authority debt—municipal bonds issued by U.S. states, cities, and counties—has historically offered tax-advantaged income but has become more sensitive to rising yields and shifting sectoral credit risks in a higher-for-longer rate environment.

The timing of the sale aligns with a rebound in inflation expectations, which has tempered appetite for long-duration debt in several markets. As investors priced in potentially higher-for-longer policy rates, the opportunity cost of holding fixed-income assets with relatively modest yields increased. In this context, cross-border holders such as Japan—traditionally among the largest foreign owners of U.S. Treasuries—adjusted their portfolios to rebalance risk and liquidity. Japan continues to maintain a substantial position in U.S. debt, standing as the largest foreign holder at roughly $1.24 trillion, followed by the United Kingdom and China. The scale of Japan’s outflows in Q1 2026 therefore reverberates beyond a single market, reflecting global yield dynamics and the interconnectedness of sovereign balance sheets.

Market participants have paid close attention to the spillover effects of such large-scale sales. In the immediate term, declines in demand from a prominent international buyer can contribute to modestly higher yields and broader price volatility in U.S. government debt. While Treasuries are typically considered the most liquid and secure asset class in many investment portfolios, a shift in ownership patterns can influence the slope of the yield curve, the pricing of inflation-protected securities, and hedging costs for international financial institutions. The renewed interest of other buyers—such as domestic institutions, asset managers, and central banks in other regions—will shape how quickly the market absorbs these outflows and whether liquidity remains robust across different segments of the fixed-income universe.

From an economic impact perspective, the decline in foreign demand for U.S. debt interacts with broader macroeconomic narratives. A weaker foreign appetite can exert modest upward pressure on long-term rates, potentially affecting borrowing costs for both governments and the private sector. For the United States, higher yields can influence the cost of funding for infrastructure programs, federal debt issuance strategies, and the affordability of monetized deficits during periods of stimulus or recovery. Conversely, higher yields can also attract domestic investment, support savers, and contribute to a more nuanced balance between growth objectives and debt sustainability.

Regional comparisons help illuminate the broader context. Other major economies with sizable holdings of U.S. debt have faced their own shifts in appetite depending on domestic inflation, currency movements, and policy expectations. For instance, European investors and sovereign wealth funds have managed a mosaic of risk perceptions shaped by eurozone dynamics, energy prices, and economic resilience. In contrast, Asia-Pacific markets—where the U.S. dollar often serves as a global reserve currency anchor—watch currency depreciation or appreciation as part of their own monetary strategies. The Japanese portfolio reallocation thus sits within a larger tapestry of strategic asset reallocation that includes currency hedging considerations, diversification goals, and the enduring appeal of U.S. macro stability.

Historical parallels shed light on possible future trajectories. The second quarter of 2022, when Japan last engaged in a comparable scale of net sales, occurred during a period of aggressive shifts in global monetary policy and heightened volatility in fixed-income markets. The retrospective lens suggests that large sovereign repositionings can create short- to medium-term market fluctuations but do not necessarily signal a lasting trend in long-run debt demand. In 2024, Japan’s buyers had remained a stabilizing force to some extent, absorbing occasional fluctuations while maintaining a measured exposure to U.S. debt. The recent outflow signals a recalibration rather than a wholesale repositioning, pointing to a strategy that weighs currency risk, yield opportunities, and macroeconomic forecasts.

Beyond the numbers, the human dimension of debt markets deserves attention. Investor sentiment, risk tolerance, and horizon-sensing strategies play a significant role in whether institutions pursue duration-heavy assets or pivot toward shorter maturities, inflation-indexed securities, or alternative fixed-income vehicles. The public reaction to such shifts can be mixed: some savers may experience improved investment alternatives as yields rise, while others worry about the implications of higher borrowing costs for public and private sectors. Yet the underlying macroeconomic structure—coping with inflation, managing public debt, and financing growth—remains the central narrative shaping these dynamics.

In terms of policy implications, the data underscore the ongoing interdependence between U.S. fiscal management and international capital flows. For policymakers, understanding the motivations behind sovereign divestment helps inform debt issuance strategies, currency stability measures, and financial market resilience planning. Central banks and finance ministries in other economies watch such movements closely, as they can hint at shifts in risk appetite, domestic inflation trajectories, and the evolving attractiveness of safe-haven assets versus higher-yield alternatives. The balance between maintaining liquidity in government debt markets and ensuring sustainable financing is a delicate one that benefits from transparent communication and prudent risk management.

From a regional perspective, comparisons with other major hubs of fixed-income investment reveal notable contrasts. In Europe, where the sovereign debt landscape is shaped by diverse fiscal policies and structural reforms, demand for U.S. debt can reflect hedging needs against local rate volatility. In emerging markets, central banks often balance the benefits of dollar-denominated assets with the potential currency and capital-flow risks embedded in such holdings. The United States, positioned as a safe harbor for global capital, continually tests the strength and resilience of its debt markets as international investors adjust to evolving economic signals.

In the longer arc of economic history, the pattern of cross-border debt flows tends to be cyclical, driven by the interplay of global growth, inflation, and policy rates. Shifts in Japanese holdings of U.S. debt in 2026 may foreshadow recalibrations that align with a gradual normalization of global funding conditions. While one quarter’s movements do not dictate a permanent course, they contribute to the ongoing dialogue about how nations allocate reserve assets, manage currency risk, and support domestic financial stability while participating in the international monetary system.

Looking ahead, market observers will monitor several key indicators to gauge the durability of the current trend. These include subsequent quarterly data on cross-border debt movements, the trajectory of U.S. inflation and wage data, and policy guidance from major central banks. The health of the U.S. Treasury market—its depth, liquidity, and the spectrum of maturities—will also influence how quickly foreign holders re-enter or adjust their exposure. In addition, developments in the global landscape, such as shifts in commodity markets, geopolitical tensions, and regional growth patterns, will shape the broader environment in which Japanese and other foreign investors make allocation decisions.

The implications for regional economies are nuanced. For Japan, the outflow may reflect a broader strategy to rebalance portfolios amid a fluctuating yen, changing domestic growth expectations, and a need to diversify beyond a heavy reliance on U.S. debt holdings. This reorientation could influence Japanese financial markets, including the performance of domestic fixed-income instruments and the behavior of pension funds and insurance companies that traditionally prioritise long-duration assets. For the United States, the challenge lies in sustaining robust demand for its debt while maintaining prudent fiscal stewardship. The symbiotic relationship between the world’s largest economy and its foreign investors persists, even as the winds of monetary policy and risk sentiment shift.

In sum, the first quarter of 2026 marked a notable turning point in the global fixed-income landscape. Japanese investors’ largest quarterly selloff of U.S. debt in recent memory reflects a confluence of rising inflation expectations, yield repositioning, and strategic portfolio management. While the immediate market impact may include modest yield adjustments and heightened volatility, the longer-term effects will hinge on broader macroeconomic developments, policy messages, and the evolving appetite of international buyers for U.S. Treasuries, agency securities, and municipal debt. As investors digest these moves, the debt market will continue to adapt to a world of interconnected financial systems, where cross-border investments shape the cost of capital and the pace of economic activity across regions.