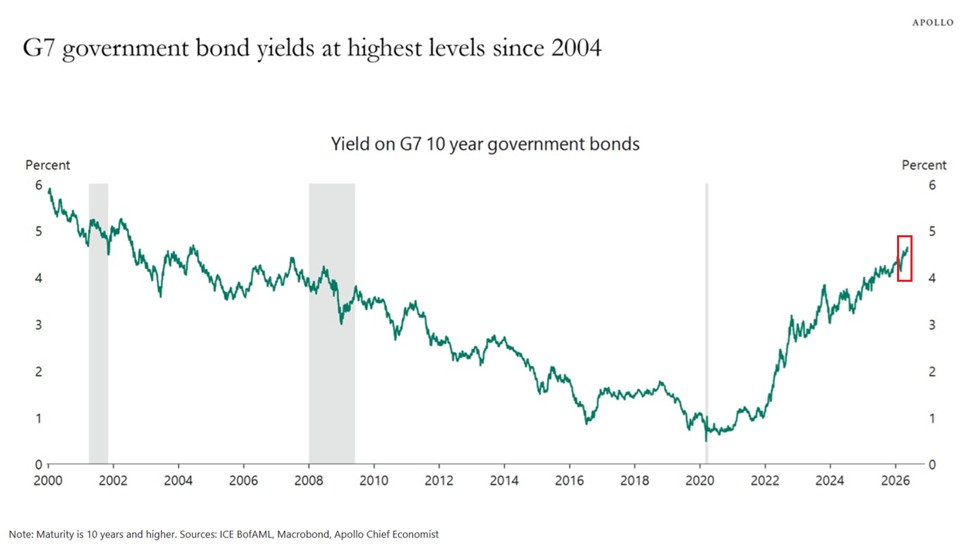

G7 Long-Term Government Bond Yields Surge to Highest Levels Since 2004

Across the Group of Seven economies, long-term government bond yields have surged to roughly 4.7%, the highest level seen since 2004. The move marks a sharp reversal from pandemic-era lows and signals a new environment in which borrowing costs for governments are rising alongside inflationary pressures, shifting the calculus for fiscal policy, pension funds, and financial markets worldwide. As markets adjust to the prospect of higher returns demanded by investors, governments face the twin challenge of financing large deficits while keeping debt sustainability in view.

Historical context: from crisis lows to sustained higher yields

To understand the current environment, it helps to trace the trajectory of sovereign borrowing costs over the past two decades. The early 2000s were characterized by relatively low interest rates and modest inflation, which supported expansive fiscal policies in many advanced economies. The 2008 global financial crisis reshaped risk perceptions and debt dynamics, prompting unprecedented monetary stimulus. Central banks deployed large-scale asset purchases and forward guidance to stabilize markets, pushing yields for long-term debt to historically low levels during the immediate aftermath of the crisis and, in some cases, through the 2010s.

The Covid-19 pandemic intensified this environment, as central banks again slashed policy rates and offered liquidity support to economies under lockdown. The resulting investor demand for safe, long-duration assets contributed to a temporary flattening of yield curves and an environment where real yields remained subdued despite rising nominal yields in the latter stages of the decade. While some inflationary pressures began to reemerge as economies reopened and supply chains faced bottlenecks, policy frameworks generally anchored expectations around gradual normalization.

Now, with inflation proving more persistent and energy prices fluctuating in a higher-priced energy regime, long-term yields have begun to reprice higher. The latest move—an ascent toward 4.7% in the G7—reflects observers’ reassessment of the trajectory for inflation, growth, and the eventual path of central banks’ tightening or tapering of stimulus. This repricing also mirrors concerns about the sustainability of large, ongoing deficits in the context of aging populations and rising public service costs, particularly in areas such as healthcare, pensions, and infrastructure.

Economic implications: debt service, deficits, and fiscal space

The rise in long-term yields has several immediate and longer-term implications for government finances and the broader economy. For the public sector, higher yields translate into higher debt-service costs on newly issued and existing debt that carries long maturities. Countries with substantial debt stocks and wide fiscal deficits could experience upward pressure on annual interest payments, potentially narrowing room for discretionary spending or delaying planned investments in areas like infrastructure and social programs.

This development also interacts with debt sustainability analyses. When borrowing costs climb, the debt-to-GDP ratio can be more challenging to stabilize or reduce, particularly if growth remains uneven or inflation persists. Policy makers may respond with a mix of measures, including targeted spending reforms, revenue enhancements, and adjustments to expenditure priorities. The balancing act involves supporting economic resilience and social objectives while maintaining market confidence in the government's ability to service debt.

Additionally, higher long-term yields influence the cost of private investment. Mortgage rates, corporate lending rates, and other long-duration financing often move in tandem with government bond yields. This can affect housing markets, business investment decisions, and consumer demand. Regions that rely more heavily on external financing or that have higher exposure to interest-rate-sensitive sectors may experience more pronounced spillovers. Conversely, some sectors may benefit from higher risk premia, encouraging prudent lending standards and more selective investment.

Regional comparisons: how different economies are navigating the shift

- United States: As the world’s largest sovereign borrower, the U.S. faces significant debt issuance to fund public services and infrastructure programs. A higher yield environment can increase the cost of new debt and reset expectations for future deficits. However, it can also attract global capital if the risk-reward balance remains favorable and the economy demonstrates resilient growth. The interplay between inflation, wage dynamics, and productivity will be closely watched by policymakers and investors alike.

- European Union members: Within the euro area, long-term yields reflect divergent growth trajectories and structural differences among member states. Countries with stronger fundamental indicators may see greater confidence from investors, while those with higher deficits or weaker growth prospects could face sharper cost pressures. The European Central Bank’s policy stance and its approach to quantitative easing normalization will influence market dynamics and the pace at which yields adjust across the bloc.

- United Kingdom: The UK economy has its own set of inflation pressures and fiscal considerations. Persistent price pressures, coupled with Brexit-related adjustments and energy price volatility, can affect the direction of long-term yields. Market participants will monitor fiscal consolidation plans and central bank communications for signals about the pace of rate normalization.

- Japan and Canada: In these economies, the response to higher yields depends on the balance between domestic growth, inflation, and monetary policy frameworks. Japan’s ultra-low-yield environment has been a distinctive feature for years, while Canada’s commodity exposure can interact with global yield movements, especially when energy and resource prices swing.

Policy responses and market resilience

Central banks are navigating a nuanced landscape. On one hand, higher long-term yields reflect improved inflation expectations and a normalization process after ultra-loose monetary policy. On the other hand, the pace and incidence of further rate adjustments will depend on evidence of durable price stability, wage growth, and the broader macroeconomic backdrop. Communicating a credible path toward inflation control and sustainable growth is essential to maintaining market confidence and preventing abrupt volatility.

Fiscal policy remains a key instrument for managing the divergence between growth prospects and debt burdens. Governments may pursue a mix of revenue-raising measures, targeted spending adjustments, and structural reforms designed to boost productivity and long-term growth. However, these policy choices carry political and social considerations, highlighting the importance of transparent communication and stakeholder engagement to sustain public trust.

Market participants—pension funds, insurance companies, and institutional investors—are recalibrating portfolios in response to higher yields. The longer-dated portion of asset allocations could see renewed demand for duration risk premia, while risk management strategies emphasize diversification and stress testing against scenarios of rising or falling rates. The interplay between asset prices and debt-servicing costs remains a focal point for financial stability analyses.

Public reaction and economic sentiment

Public sentiment around rising yields often centers on the tangible effects of higher borrowing costs. Households may feel the impact through changes in mortgage rates, loan terms, and consumer credit conditions. Businesses respond by adjusting capex plans, supplier contracts, and financing arrangements. In many regions, communities that rely on public sector projects or infrastructure development watch closely for signs that projects will proceed on schedule or encounter financing bottlenecks.

At the same time, observers emphasize resilience and adaptation. Economies display a capacity to absorb near-term shocks if accompanied by steady growth, controlled inflation, and credible policy frameworks. The social contract—how governments allocate resources and address the needs of workers, families, and retirees—continues to shape public response as markets adjust to the evolving debt landscape.

Outlook: what comes next for yields and borrowing costs

Analysts expect yield levels to find a new equilibrium as inflation moderates, growth stabilizes, and central banks refine their policy paths. The pace of normalization will likely vary by country, reflecting differences in fiscal discipline, demographic trends, energy prices, and global demand. If inflation proves to be persistent, yields may maintain higher levels for an extended period, requiring careful macroeconomic management to avoid overheating financial conditions or dampening recovery.

Conversely, if inflation cools more quickly than anticipated and growth remains steady, yields could retreat from current highs, easing debt-service pressures and restoring some fiscal flexibility. The timing and magnitude of any pullback will depend on a complex array of indicators, including wage growth, labor market tightness, energy costs, and the effectiveness of supply-chain stabilization efforts.

Conclusion: navigating a high-yield environment

The recent surge in G7 long-term government bond yields to the highest levels since 2004 underscores a pivotal shift in the global financial landscape. It highlights the enduring challenge of balancing inflation control with sustainable growth and responsible debt management. As governments adjust to higher borrowing costs, markets, institutions, and households will need to adapt to a climate where long-duration risk carries a more significant premium. The coming months will reveal how policy makers coordinate monetary normalization with fiscal prudence, and how regional economies cope with the ripple effects across housing, investment, and public services. Public and private sector actors alike will be watching carefully as the debt landscape evolves in a world where yields have moved decisively higher and the road to financial stability requires careful navigation.