Troubled Tech Debt Swells on AI Fear

In recent months, a wave of stress has swept through the US technology finance landscape, signaling tighter credit conditions and mounting concern over tech-sector leverage. The latest metrics show that distressed lending in the tech arena is at levels not seen since the 2022 bear market, underscoring how fear surrounding artificial intelligence, platform shifts, and cyclical demand has rippled through lenders and borrowers alike. This development arrives at a moment when the broader economy remains sensitive to rate expectations, inflation dynamics, and the evolving capital needs of digital modernization.

Historical context: a cycle of leverage and risk To understand the current environment, it helps to place it within a longer arc of tech credit cycles. The late 2010s and early 2020s saw a period of rapid funding for software, cloud services, and semiconductor development, often underpinned by generous loan covenants and sizable bond issuance. As AI-related investments intensified, borrowing continued to expand, supported by a belief that product maturities would accelerate returns and that technology demand would remain resilient even amid macro headwinds. The ensuing market volatility, however, has exposed some vulnerabilities in segments where financing was most aggressive.

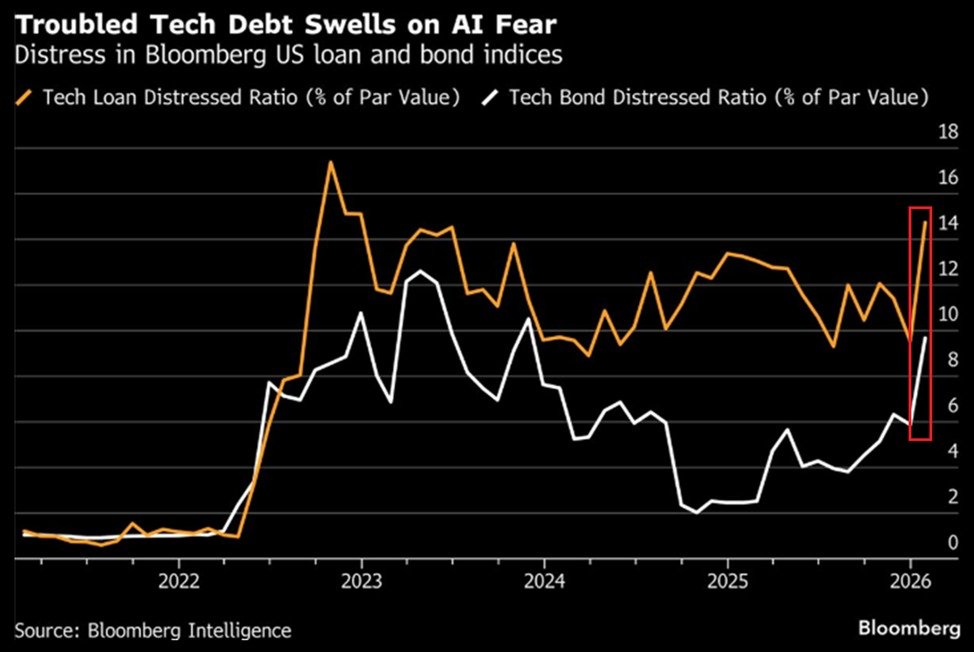

The latest data point—distressed loans at 14.5% within the tech loan book—marks a notable deterioration. This is the highest share of distressed loans in the tech sector since the 2022 downturn, when capital access tightened and equities repriced risk across growth-oriented businesses. A parallel measure, the tech bond distressed ratio at 9.5%, has also advanced to its highest level since late 2023. Taken together, these indicators reflect rising risk of default or near-default conditions in both syndicated and private debt markets tied to technology firms.

Economic impact: cascading effects from credit to deployment The pressures in tech credit markets reverberate across several layers of the economy. First, higher distress levels tighten liquidity for software developers, hardware manufacturers, and AI-focused startups. When lenders classify a growing share of loans as distressed, they respond with tighter covenants, higher borrowing costs, and more stringent collateral requirements. That, in turn, can slow deployment of AI initiatives, delay capital expenditures, and compress investment timelines for firms pursuing aggressive digital transformation architectures.

Second, the credit squeeze can influence vendor ecosystems and procurement decisions. Software and services suppliers—especially those operating on leveraged financing or revolving credit facilities—may experience reduced access to capital, leading to slower product rollouts, delayed maintenance cycles, or the postponement of strategic upgrades. In the short term, this deters some enterprise buyers from undertaking ambitious AI integrations, potentially dampening near-term demand for cloud-based AI platforms and related services.

Third, regional capital markets feel the toll through collateralized loan obligations and leveraged loan instruments. Software debt in collateralized loan obligations has posted a notable decline, with January recording the sharpest drop in at least a year and marking the worst performance among represented sectors. Since software accounts for a meaningful portion of the US Leveraged Loan Index, stress in this area can influence broader market dynamics, including pricing, liquidity, and investor appetite for higher-yield tech credit products.

Regional comparisons: how tech credit stress plays out across markets While the United States remains the central focus of these metrics, regional dynamics offer useful contrasts. In major tech hubs, where venture-backed start-ups and mid-market firms rely heavily on credit lines to sustain growth between funding rounds, the impact of rising distress can be more pronounced. Regions with greater exposure to AI-enabled manufacturing, data center expansion, or software-as-a-service growth tend to see amplified sensitivity to changes in lending standards and bond market sentiment.

By comparison, markets with a more diversified industrial base or stronger balance-sheet discipline among lenders may exhibit slightly more resilience. Banks and non-bank lenders in these areas often maintain tighter risk controls and more robust tier-one capital, enabling a measured response to changing risk appetites. Yet even these markets are not immune to a broad tightening of financial conditions, especially when expectations for technology demand shift or when financing costs rise due to macroeconomic uncertainty.

Implications for policy, enterprises, and investors Policy conversations and regulatory considerations continue to intersect with tech credit markets in several meaningful ways. Regulators may monitor whether elevated distress signals in the tech sector foreshadow broader financial stress or systemic risk, prompting issuers and lenders to reassess underwriting standards and stress testing. For policymakers, the balance lies in encouraging responsible innovation while ensuring capital markets function efficiently to support productive, technology-driven growth.

For enterprises, the uptrend in distress metrics translates into a cautious approach to capital structure management. Companies are likely to prioritize debt refinancing, covenant clarity, and liquidity buffers to weather tightening conditions. Firms pursuing AI and cloud initiatives may need to demonstrate clear path-to-value projections, robust cost controls, and realistic timelines for monetization to secure favorable financing terms.

Investors looking at technology credit spaces should calibrate expectations for yields, default risk, and volatility. Distressed debt metrics suggest elevated risk premia, particularly in segments linked to software debt in leveraged structures. However, there remains potential for selective opportunities among well-capitalized issuers with strong cash flows, disciplined capex plans, and durable competitive advantages in high-growth domains such as AI-enabled software, cybersecurity, and data infrastructure.

Interpreting the current trajectory: signals and cautions The convergence of higher distress levels in tech loans and the peak distress in certain bond instruments points to a synchronized tightening across both bank-led and market-based credit channels. This alignment can reflect a combination of rising funding costs, cautious underwriting, and investor risk aversion amid uncertain AI demand trajectories, supply chain normalization, and competitive dynamics within technology markets.

Yet the broader ecosystem also contains supportive undercurrents. Demand for cloud computing, AI-enabled analytics, and digital platforms remains robust in many industries as organizations seek to digitize operations, enhance decision-making, and bolster resilience. The challenge for lenders is to distinguish between prudent risk management and overly restrictive financing that could stifle productive technological advancement.

Industry resilience and adaptation In response to credit pressures, technology firms are implementing several strategic adaptations. These include focusing on profitability over growth, tightening discretionary spend, and accelerating product roadmaps with clearer monetization strategies. Many companies are exploring alternative funding channels, such as strategic partnerships, licensing arrangements, and revenue-based financing arrangements that align funding sources with measurable outcomes.

Additionally, the technology services ecosystem is adapting by offering modular, scalable solutions that reduce upfront capital requirements for customers. This shift can improve cash-flow profiles for vendors and clients alike, potentially mitigating some leverage-related vulnerabilities. As firms embrace these models, lenders may re-evaluate risk profiles to reflect more predictable revenue streams and longer-term customer engagements.

Public sentiment and market psychology Public reaction to rising tech credit stress tends to be a barometer of broader economic confidence.s about debt loads and default risk can influence business sentiment, shaping hiring plans and investment priorities. In periods of heightened concern, decision-makers may exhibit increased prudence, prioritizing core competencies and sustainable growth over experimentation with high-risk, high-reward ventures. Conversely, as stabilization emerges and liquidity returns, market confidence can rebound, encouraging reinvestment in AI programs and digital transformation initiatives.

Conclusion: navigating a cautious yet hopeful horizon The current stretch of rising distress in US tech credit markets reflects a confluence of high expectations for AI-driven value and the practical realities of financing complex digital initiatives in a tightening macro environment. While the metrics signal elevated risk, they also highlight a sector undergoing careful recalibration—prioritizing disciplined capital management, clearer monetization pathways, and resilient strategic planning.

For lenders, borrowers, and policymakers, the path forward lies in a careful balance: sustaining access to essential funding for innovation while enforcing prudent risk controls. The technology sector has repeatedly demonstrated an ability to adapt quickly to shifting conditions, and the current moment is no exception. As AI technologies continue to mature and expand across industries, the push and pull between growth aspirations and financial discipline will shape investment patterns, product development, and regional economic outcomes for months to come.