Rising U.S. Bond Yields Overtake Oil Prices as Top Market Threat Amid Iran War

U.S. Treasury Yields Surge as Global Conflict Escalates

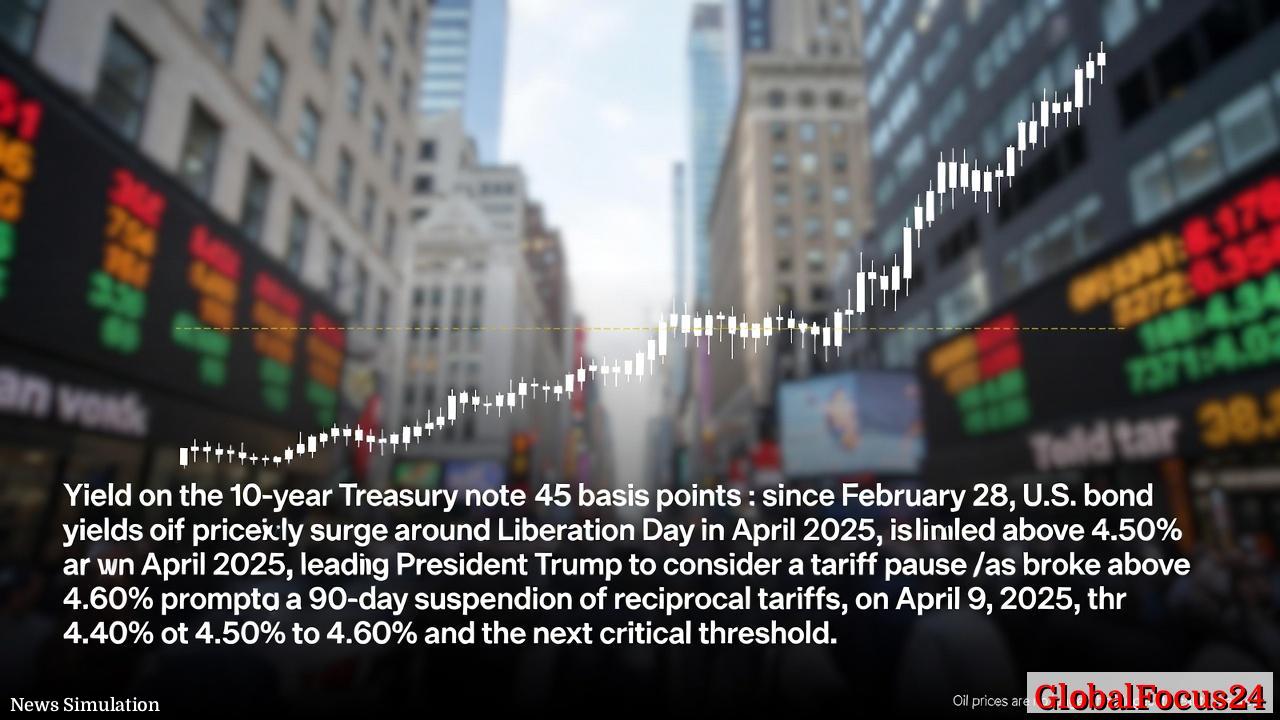

Rising U.S. bond yields have surged to the forefront of global financial concerns, overtaking oil prices as the primary threat to market stability amid the ongoing Iran War. Since hostilities began on February 28, the yield on the benchmark 10-year U.S. Treasury note has climbed roughly 45 basis points, approaching levels not seen since the spring of 2025.

This sharp increase signals growing tension within both domestic and international markets. Investors, traditionally turning to Treasuries as a safe haven in times of conflict, are instead contending with the inverse effect: a sell-off in government debt that reflects anxiety over inflationary pressure, fiscal imbalances, and a fragile geopolitical landscape.

As of late March, the yield stands at 4.40%. Analysts warn that a sustained rise into the 4.50%–4.60% range could reawaken memories of last year’s policy turbulence, when the U.S. government resorted to temporary trade measures to stabilize the economy.

Historical Echoes of Market Volatility

The current surge draws stark parallels to events nearly a year ago, around Liberation Day in April 2025, when yields spiked to similar levels amid global trade uncertainty. At that time, yields climbing above 4.50% compelled Washington to reconsider its tariff strategy, as rising borrowing costs threatened to tighten financial conditions across multiple sectors.

By early April 2025, when yields pierced the 4.60% mark, the administration implemented a 90-day suspension of reciprocal tariffs—a move designed to calm currency markets and ease inflationary pressure stemming from import costs. That temporary measure helped cool yield momentum briefly, but structural issues such as high federal deficits and robust labor costs quickly reignited upward pressure.

Market observers now suggest that, although the details differ, the underlying dynamics remain the same: elevated government spending, persistent supply chain challenges, and geopolitical conflict continue to strain the Treasury market. The pattern underscores a recurring theme in U.S. fiscal history—episodes of global crisis amplifying domestic economic vulnerabilities.

The Shifting Role of Oil in a Time of War

Traditionally, war in the Middle East triggers an immediate surge in oil prices, with investors bracing for disruptions to global energy supply. Yet in the weeks since the Iran War began, oil has remained comparatively steady, confounding expectations. While crude prices did initially spike when airstrikes intensified in early March, they soon retreated as global output adjustments, emergency reserves, and reduced demand in Europe helped stabilize supply dynamics.

This unusual decoupling of oil from geopolitical risk has redirected investor fears toward fixed-income markets. The muted energy response contrasts sharply with the oil shocks of earlier decades, such as the Gulf War in 1990 and the Iran-Iraq War of the 1980s, when crude prices skyrocketed and dominated markets.

Today, however, the broader financial ecosystem is more exposed to fluctuations in interest rates than to oil price volatility. A world built on cheap debt and leveraged assets is far more vulnerable to sharp swings in Treasury yields than to moderate energy price shifts.

Why Rising Yields Matter More Than Ever

The 10-year Treasury yield serves as a benchmark for nearly all forms of borrowing, from corporate bonds to home mortgages. As yields climb, the cost of capital increases, slowing corporate investment and dampening consumer spending. A rise of even 40–50 basis points can ripple through sectors like real estate, auto manufacturing, and technology—each heavily reliant on access to credit.

At 4.40%, yields remain below the critical levels seen last April, but financial strategists warn that breaching the 4.60% threshold could push borrowing costs close to unsustainable levels. Many analysts agree that the U.S. economy cannot comfortably withstand a 5% yield on the 10-year note without triggering financial tightening akin to a recessionary shock.

Historically, such levels have coincided with slower growth, equity market corrections, and reduced lending activity. The correlation is not causal but thematic: high Treasury yields often indicate an economy overheating or absorbing higher fiscal risk, forcing central banks and bond traders alike to reassess long-term inflation expectations.

Fiscal Pressures and the Debt Question

Underlying this market tension lies an uncomfortable arithmetic. The United States continues to finance record-level fiscal deficits, a dynamic intensified by both pandemic-era spending legacy and rearmament programs related to global military commitments. As debt issuance increases, so does the supply of Treasuries on the open market—placing downward pressure on bond prices and upward pressure on yields.

Federal debt servicing costs are now projected to grow faster than defense or healthcare spending by late 2026, according to many economists. A 5% 10-year yield would add tens of billions of dollars to annual interest expenses, crowding out discretionary programs and complicating future budget negotiations.

The Treasury Department faces a delicate balancing act: financing national priorities while preventing an investor backlash that could drive yields even higher. This interplay of policy, market psychology, and global instability forms the backdrop for the current surge, one that may define the trajectory of the American economy through the remainder of the decade.

Investor Sentiment and Market Dynamics

On Wall Street, traders are recalibrating expectations for both inflation and Federal Reserve policy. While the Fed’s official stance remains cautious, the market has increasingly priced out earlier assumptions of rate cuts in 2026. Instead, futures data show a growing belief that elevated rates may persist for much longer—especially as fiscal expansion and defense mobilization add upward pressure to medium-term inflation.

In the equity markets, sectors sensitive to interest rate shifts, such as housing, banking, and technology, have all experienced heightened volatility. Bond funds are recording unusually large redemptions, and municipal issuers are facing higher financing costs, leading some states to postpone or scale back infrastructure projects.

The private sector, particularly small and mid-sized firms, is beginning to feel the squeeze. Rising credit costs make refinancing existing debt more expensive, potentially dampening job creation and investment appetite just as the broader economy faces geopolitical risk premiums. The effects are cumulative, not immediate, but they underscore why financial analysts increasingly rank rising bond yields as a greater threat than oil in the current environment.

Comparing the Current Climate with Global Trends

The United States is not alone in confronting rising yields. Across advanced economies, government bonds have sold off as investors demand higher compensation for long-term uncertainty. The United Kingdom, Japan, and parts of the Eurozone have all seen modest but noteworthy increases in benchmark yields since early March.

However, America’s position as the world’s reserve currency issuer amplifies the global significance of its bond market movements. When U.S. yields rise sharply, they often export financial strain: emerging-market currencies weaken, capital flows shift toward dollar assets, and developing nations face higher borrowing costs. The result is a cascading tightening of financial conditions worldwide.

In Asia, central banks have intervened to stabilize currencies against the dollar, while European policymakers weigh the trade-offs between inflation control and growth amid a slowing industrial sector. The interconnected nature of global bond markets means that a sustained U.S. yield spike could exert pressure far beyond Washington’s borders.

Economic Outlook: A Fragile Equilibrium

Economic forecasts for the remainder of 2026 hinge largely on whether Treasury yields stabilize below critical thresholds. If yields can remain near 4.40% without a renewed acceleration, analysts expect moderate GDP growth to continue, supported by consumer spending and strong labor markets. However, a breach of 4.60% or beyond would likely tighten financial conditions considerably, forcing the Federal Reserve and the White House to coordinate policy responses similar to those undertaken in 2025.

The challenge lies in timing and credibility. Any perception that policymakers are reacting defensively, rather than strategically, could undermine confidence in U.S. fiscal management. Conversely, measured communication coupled with inflation control could reassure markets and curb excessive volatility.

The coming weeks will be pivotal. As the conflict in the Middle East continues and global trade routes face disruption, investors will watch closely for signs of intervention—monetary or fiscal—that could determine the trajectory of yields through the summer.

A Global Market on Edge

For now, the bond market’s message is clear: the cost of security is rising, and financial conditions are tightening. The Iran War has amplified underlying tensions but has not fundamentally altered the mechanics driving yields higher. The forces at work—fiscal strain, investor skepticism, and cautious central bank policy—reflect structural realities rather than short-term panic.

With the 10-year yield hovering near 4.40% and the critical 4.50%–4.60% zone in sight, markets remain poised on a razor’s edge. Every incremental basis point has implications that ripple through housing, industry, and international capital flows. In an era defined by fiscal expansion and geopolitical friction, rising U.S. bond yields have once again become the clearest barometer of global financial risk—and perhaps the defining economic story of 2026.