Federal Reserve Now Expected to Hold Rates Until Late 2027 as Markets Shift Toward Possible Hikes

The Federal Reserve’s long-anticipated pivot to lower interest rates appears to be on an extended delay. According to the latest futures market data, investors now see the first potential cut in the federal funds rate not arriving until December 2027—more than a year later than previously expected. In fact, markets are assigning a growing probability that the central bank could raise rates again before that date, underscoring persistent concerns about inflation, resilient consumer demand, and a still-tight labor market.

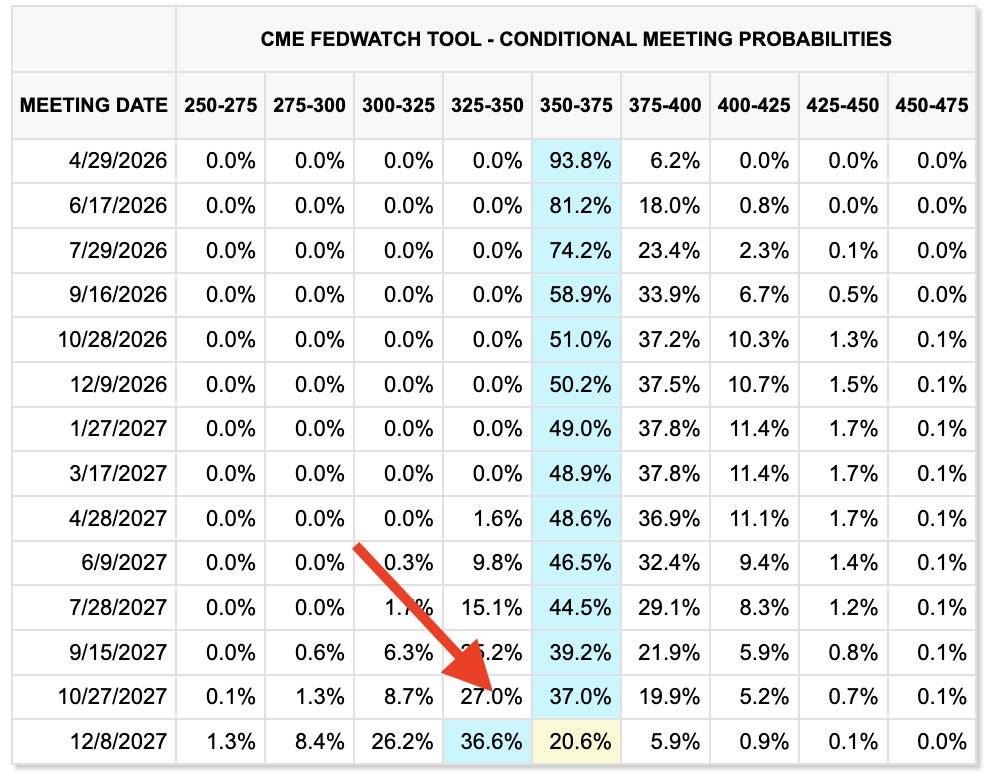

Market Expectations: From Cuts to Possible Hikes

Interest rate futures show an increasing likelihood that the next policy move could be an upward one. Data now indicate a 51% probability of an interest rate hike by March 2027, marking the first time in nearly two years that the prospect of higher borrowing costs has outweighed the expectation for cuts.

These shifts reflect a reappraisal of the economic landscape following a string of stronger-than-expected inflation and employment reports. While core inflation has moderated from its 2022 highs, recent months have seen modest reacceleration across key categories such as housing and services. This sustained price pressure has forced markets to reassess the timeline for when the Federal Reserve might feel confident enough to ease policy.

Federal Reserve Caution Amid Uncertain Disinflation

The Federal Reserve has signaled a cautious stance since mid-2025, emphasizing its commitment to bringing inflation back to the 2% target on a “sustainable basis.” Although consumer-price growth slowed considerably from its pandemic-era peak, it remains above that goal, prompting officials to maintain a restrictive policy stance longer than markets initially anticipated.

Chair Jerome Powell and other Federal Open Market Committee (FOMC) members have reiterated that premature rate cuts could risk undoing progress made on inflation. Their measured communication has contributed to anchoring long-term inflation expectations but has also dampened hopes for near-term relief in lending costs.

“Policy needs to remain steady until inflation’s decline is fully secured,” Powell said in late 2025, highlighting the importance of clear evidence before easing monetary conditions. That sentiment continues to dominate market pricing well into 2026.

Economic Backdrop: Growth Without Cooling Inflation

The strength of the U.S. economy remains a double-edged sword for policymakers. Real GDP growth held steady through 2025, while consumer spending showed little sign of fatigue. The labor market continues to defy expectations, with unemployment below 4% and wage growth keeping pace with prices.

These dynamics have underpinned households’ confidence and corporate investment, but they have also slowed the pace of disinflation. Sectors such as housing, healthcare, and transportation have maintained upward pricing momentum, a pattern inconsistent with the rapid normalization that many economists had hoped to see by now.

The persistence of inflation at these levels makes cutting rates a difficult proposition. For the Fed, moving too quickly could invite a repeat of the 1970s pattern, when premature easing contributed to resurgent price pressures.

Historical Context: Lessons from Past Tightening Cycles

Historically, interest rate cycles have exhibited long lags between the final hike and the first cut. In the early 2000s, for example, the Fed held rates steady for nearly a year before reversing course. During the 1980s inflation fight, it maintained elevated rates for even longer to ensure price stability.

The current cycle, which began with aggressive hikes from near zero in 2022 to over 5% by mid-2024, resembles those earlier eras more than any recent one. The inflation shock triggered by the pandemic and subsequent supply disruptions remains one of the most severe in decades. The Fed’s patient approach, officials argue, is designed to prevent a destabilizing rebound in inflation expectations.

Global Comparisons: Diverging Monetary Paths

The U.S. stance contrasts sharply with monetary policy trends in other major economies. The European Central Bank and the Bank of England have already begun modest rate cuts as inflation recedes more quickly in their regions. The divergence underscores differences in economic resilience and labor market structure.

In Europe, energy price declines and slower wage growth have hastened disinflation, giving policymakers room to ease without fueling inflationary risks. By contrast, the U.S. economy’s robustness—buoyed by high consumer spending and sustained fiscal support—has forced the Fed to keep rates higher for longer.

In Asia, central banks such as the Bank of Japan and the Reserve Bank of Australia are also navigating complex trade-offs. Japan, having only recently exited negative rates, remains cautious about tightening further. Meanwhile, Australia’s experience mirrors that of the U.S., with a stubbornly strong labor market complicating the path to lower rates.

Financial Market Reaction and Corporate Impact

The repricing of interest rate expectations has rippled through financial markets. Treasury yields have risen across the yield curve, particularly in the 5- to 10-year range, reflecting reduced bets on near-term easing. Equities, especially rate-sensitive sectors like real estate and technology, have faced renewed headwinds after a period of optimism earlier this year.

Corporate borrowers are also feeling the effects. High-yield bond spreads have widened modestly, while companies with floating-rate debt face elevated interest expenses. Small businesses, reliant on bank credit lines, are encountering higher costs of capital, potentially limiting expansion plans.

However, investment-grade firms with strong balance sheets continue to find credit markets receptive, suggesting that financial conditions, while tight, remain functional. This balance underscores the Fed’s success in containing inflation without triggering systemic stress—a key objective of its gradualist approach.

Housing and Consumer Finance Adjustments

Nowhere is the impact of sustained high rates more visible than in the housing market. Mortgage rates hovering near multi-decade highs have continued to suppress home sales and construction activity. Although prices have stabilized in several regions, affordability remains a pressing issue for first-time buyers.

Consumer credit conditions have also tightened. Credit card rates remain above 20%, and auto loan delinquencies have risen slightly as households adjust to higher financing costs. Still, robust employment and steady wage growth have prevented widespread distress—a sign of resilience but also of ongoing monetary constraint.

Outlook: Delayed Easing, Persistent Uncertainty

Looking ahead, the question for markets is not only when the Fed will cut rates but whether further hikes might be necessary. If inflation data continue to show stubborn strength through 2026, policymakers may feel compelled to raise rates again to reassert their commitment to price stability.

A 51% probability of a hike by March 2027 implies nearly even odds between tightening and holding steady, while the chance of any cut before December 2027 remains remote. These probabilities could shift quickly, however, should incoming data show meaningful progress toward the 2% inflation goal.

Economic analysts suggest that by 2027, the combined effects of restrictive policy, receding fiscal stimulus, and demographic shifts could naturally slow demand, paving the way for eventual easing. But the timing remains deeply uncertain—an uncertainty that continues to define both policy debates and market expectations.

Broader Economic Implications

For consumers and businesses alike, the prospect of high rates persisting into late 2027 has profound implications. Borrowers may need to adjust to an extended period of elevated financing costs, while savers could benefit from sustained returns on fixed-income products.

Federal debt servicing costs are also rising, adding pressure to the government budget. Higher interest payments could crowd out other fiscal priorities if yields remain elevated for several more years. Meanwhile, investment strategies tied to shorter policy horizons may need to be recalibrated as the timeline for policy normalization extends further into the future.

Conclusion: A New Era of Higher-for-Longer

As of early 2026, the Federal Reserve finds itself at a delicate crossroads. Inflation has eased but not vanished; growth has slowed but remains solid. The balance between restraint and risk continues to define U.S. monetary policy.

The market’s evolving outlook—now projecting the first cut no earlier than December 2027 and even pricing in a chance of further hikes—signals a collective realization that the era of near-zero rates is firmly behind. Whether this high-rate environment marks a temporary plateau or the beginning of a new long-term normal will depend on the delicate interplay of data, expectations, and global economic forces over the next two years.

For now, both Wall Street and Main Street must prepare for an extended period of monetary restraint, as the world’s most influential central bank leans once again on patience, data, and discipline to navigate the next phase of the economic cycle.