Investor Sentiment Turns Deeply Negative as Bearish Views Hit 10-Month High

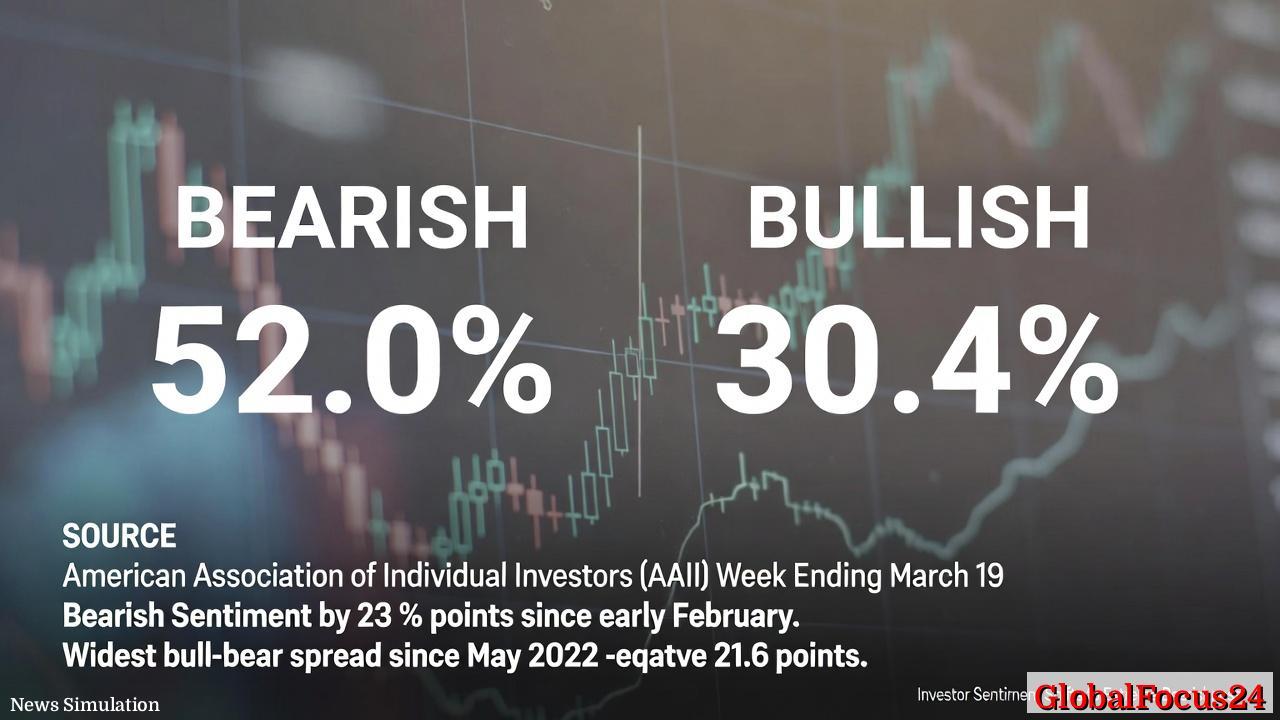

Investor confidence has plunged to its lowest point in nearly a year, with U.S. retail investors signaling sharp pessimism about the stock market’s outlook. According to the latest American Association of Individual Investors (AAII) Sentiment Survey for the week ending March 19, 52.0% of respondents reported a bearish view of the market over the next six months — the highest level since May 2025. The rapid surge in gloomy sentiment underscores growing unease over economic prospects, volatile earnings expectations, and persistent global uncertainty.

Bearish Surge Marks Sharp Sentiment Shift

The shift has been dramatic. Bearish sentiment has risen by more than 23 percentage points since early February, the largest monthly increase since February 2025, when fears of a renewed trade conflict sent markets tumbling. Over the same period, bullish sentiment has slumped to just 30.4%, its third-lowest reading in ten months and a continuation of an eight-week slide that has gradually eroded optimism.

The bull-bear spread—the difference between optimistic and pessimistic outlooks—now stands at negative 21.6 percentage points. Analysts note that this figure often serves as a psychological gauge for market behavior; such a wide gap historically aligns with times of heightened volatility or correction phases. The last time the spread was this wide was in mid-2025, coinciding with a period of sustained market turbulence and bond yield inversion.

Signals from the AAII Survey: A Market Thermometer

For over three decades, the AAII Sentiment Survey has been considered a vital barometer of retail investor psychology. Weekly changes often provide early hints of shifting market dynamics, as overly bullish or bearish extremes can precede market reversals. Historically, periods when bearish sentiment climbs above 50% have correlated with contrarian buying opportunities, as pessimism reaches unsustainable levels.

However, the current mood reflects more than mere emotional reaction. Market strategists suggest that investors are struggling to reconcile mixed economic signals — cooling inflation data alongside uneven consumer spending, slowing job growth, and cautious corporate guidance. While certain sectors such as technology and renewable energy have shown resilience, concerns about valuation pressures and supply chain disruptions remain prevalent.

Global Factors Weigh on Investor Optimism

The renewed wave of pessimism is not occurring in isolation. A cocktail of global economic headwinds has intensified uncertainty in recent months. Renewed trade tensions between major economies, fluctuating oil prices, and delays in interest rate adjustments have amplified fears of a broader slowdown.

Markets in Europe and Asia have echoed these concerns. The Euro Stoxx 50 has faced similar bearish pressure amid weaker-than-expected industrial output, while major Asian indices have posted mixed results as regional investors grapple with export headwinds. In Japan, investor confidence has wavered despite strong corporate earnings, as monetary tightening looms. Meanwhile, China’s ongoing efforts to stabilize property markets have had uneven results, contributing to cautious global risk sentiment.

Historical Context: Lessons from Previous Bearish Waves

The current bearish intensity recalls market psychology from previous downturns. During the 2022 bear market, the AAII bearish reading surged above 58%, coinciding with a steep sell-off in growth stocks and widespread concerns over rising interest rates. In May 2025, similar levels of pessimism followed a bout of trade-related tensions and currency volatility.

In each case, sentiment extremes tended to precede recoveries within months, driven by stabilization in macroeconomic indicators. Historically, a high bearish reading does not guarantee further declines; rather, it represents widespread capitulation that can set the stage for rebound if fundamental conditions improve. Still, analysts caution that context matters — during prolonged tightening cycles or global shocks, negative sentiment can persist longer before markets stabilize.

Investor Psychology and Market Behavior

Investor sentiment remains one of the most closely watched indicators for market timing and behavioral finance analysis. When retail investors overwhelmingly lean bearish, it often reflects emotional responses to recent volatility rather than fundamental deterioration. Behavioral economists note that fear-driven decision-making can amplify short-term swings, as investors de-risk portfolios collectively.

Yet, professional market participants often interpret extreme pessimism as a contrarian signal. High fear levels can coincide with undervaluation across sectors, presenting opportunities for long-term investors willing to weather short-term turbulence. In previous cycles, notably in 2020 and 2022, deeply negative sentiment readings were followed by multi-month rallies once macro data stabilized.

Economic Factors Fueling Market Angst

Several economic undercurrents explain the sentiment shift. Inflation has moderated significantly from 2025 highs but remains uneven across key categories, with energy and housing costs still elevated. The Federal Reserve’s cautious approach to rate cuts, aimed at preventing a resurgence of price pressures, has left investors uncertain about the timing of policy easing.

Corporate earnings have sent mixed signals: while large-cap technology firms have largely met expectations, industrials, small caps, and cyclical sectors have issued profit warnings tied to slowing demand. At the same time, U.S. Treasury yields remain elevated, fostering competition between stocks and bonds for investor capital.

Consumer confidence has also waned, particularly among lower-income households contending with high borrowing costs. These overlapping factors have combined to reinforce defensive positioning across retail portfolios.

Comparing U.S. Sentiment to Global Trends

While U.S. retail sentiment stands out for its steep decline, international markets show parallel caution. In Europe, investor confidence surveys have fallen for three consecutive months amid stubborn inflation and weak manufacturing data. The United Kingdom’s FTSE indices have lagged global peers, reflecting both domestic political uncertainty and global economic exposure.

In Asia, the outlook diverges. Indian equities have remained relatively robust thanks to strong domestic growth, while South Korean and Taiwanese markets have faced selling pressure due to semiconductor sector volatility. Latin American markets, driven by commodity exports, have experienced moderate optimism as global energy prices stabilize, though currency volatility remains a risk.

This contrast highlights that the U.S. sentiment downturn is part of a broader pattern of global caution rather than an isolated collapse of confidence.

Reactions from Analysts and the Broader Market

Market strategists across Wall Street and independent research firms are split on whether the current pessimism is a precursor to further declines or an opportunity for recovery. Some argue that persistent investor fear suggests the market has not yet reached capitulation, implying potential for additional downside if earnings disappoint. Others believe that sentiment has turned excessively negative, setting up conditions for a short-term relief rally if inflation data or corporate results improve.

Institutional investors have reported increased demand for defensive assets such as longer-term Treasuries, gold, and dividend-paying stocks. The VIX volatility index has risen moderately, signaling heightened investor protection strategies but still staying below crisis levels.

On trading floors, activity has tilted toward hedging and cash accumulation rather than panic selling — a sign, according to some analysts, that the sentiment downturn is more psychological than systemic at this stage.

Historical Parallels and Potential Turning Points

If historical patterns hold, extreme bearish sentiment may persist for several weeks before stabilizing. Data from past market cycles indicates that when the AAII bearish reading surpasses 50%, subsequent six-month equity returns often improve compared to periods of neutral sentiment. Investors, however, remain cautious about assuming history will repeat amid today’s more complex global environment.

Several potential catalysts could reverse sentiment: an earlier-than-expected policy shift from the Federal Reserve, stronger-than-forecast first-quarter earnings, or easing geopolitical tensions. Conversely, renewed trade frictions or signs of recession could entrench pessimism further.

Outlook: Uneasy Calm Ahead of Key Data

Looking ahead, investors are bracing for a series of critical economic reports that may shape market direction into spring. The upcoming personal consumption expenditures (PCE) inflation data, corporate earnings season, and fresh labor market updates could clarify whether the bearish surge reflects justified caution or excessive fear.

Even as pessimism sweeps across surveys, the broader market remains within sight of major technical support levels, suggesting resilience beneath the surface. For long-term investors, the disconnect between sentiment and fundamentals could present selective opportunities, particularly in sectors with strong balance sheets and consistent cash flow.

Still, the prevailing mood is one of vigilance. With bearish sentiment at its highest in nearly a year, the next few weeks will test whether America’s investors are reacting to temporary uncertainty — or signaling deeper concern about the durability of the post-pandemic expansion.