US Food Blockages and Fading Price Pressure: A 2026 Look at Inflation, Fertilizer, and Supply Chains

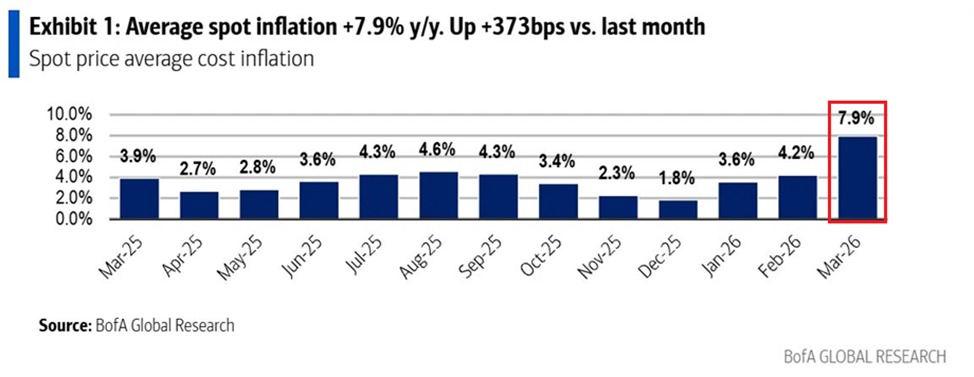

A recent surge in input costs for American food and beverage companies has highlighted how a complex web of energy, fertilizer, and transport pressures can ripple through the economy from farm fields to grocery aisles. In March, the average input inflation for US food and beverage producers rose to 7.9 percent year over year, marking the sharpest gain in at least a year and widening from 4.2 percent in February by 373 basis points. The surge underscores how global commodity dynamics and domestic logistics are colliding to shape price trajectories for households and businesses alike.

Historical context: a long arc from farm to fork To understand the current momentum, it’s helpful to map the sequence from farm input to retail price. Fertilizer costs, particularly nitrogen-based products like urea, are a foundational input for crop yields. When fertilizer becomes costlier, farmers face higher production expenses, which can translate into higher wholesale prices for fruits, vegetables, and other perishables. The fertilizer market has experienced pronounced volatility over the past several years, driven by shifts in natural gas prices, global supply constraints, and geopolitics. In the United States, the recent price dynamics for urea—doubling since February and reaching around $900 per metric ton—signal a renewed stress on farming margins and a potential pass-through to wholesale food costs as farmers adjust planting plans, fertilizer application rates, and crop mixes.

Beyond fertilizer, energy and fuel costs have remained a persistent pressure point. Diesel prices have surged, with a near-88 percent year-over-year increase highlighted in recent wholesale data. The transportation sector, including trucking, shipping, and rail, functions as a critical artery for food distribution. When fuel costs climb, the cost of moving goods from rural production zones to urban markets rises accordingly. This dynamic tends to compress profit margins for producers if pass-through is imperfect or delayed, while accelerating consumer-facing price signals at the grocery store in the absence of sufficient competition or buffering inventory.

Regional context: growth, inflation, and resilience across markets Different regions in the United States have experienced varying intensities of input cost pressures, reflecting local agricultural mixes, climate conditions, and energy infrastructure. In the Midwest, a breadbasket region characterized by large-scale row crops, fertilizer application intensity and fuel consumption are central to production costs. In coastal and urban markets, where fresh produce and perishables dominate purchasing patterns, wholesale price shifts can quickly translate into retail changes that affect household budgets.

Comparative lenses show similar inflationary threads in global markets, though with notable distinctions. Countries with fertilizer subsidies or domestic fertilizer production capacity may experience different transmission speeds from input costs to consumer prices. Supply chain resilience also matters: regions with diversified transport networks and robust warehousing can dampen price volatility, while areas relying on fragmented logistics or limited cold-chain infrastructure may see sharper price swings.

Economic impact: from margins to consumer wallets The March data suggest a two-stage effect on the broader economy. First, producer costs are rising, particularly for essential inputs like fertilizer, fuel, and certain plastics used in packaging. The second stage involves how these increased costs, once embedded in wholesale pricing, affect consumer prices at the grocery level. If wholesale inflation persists or accelerates, grocery bills for everyday staples—such as vegetables, fruit, and processed foods—could rise in tandem with supply chain friction.

Industry analysts are watching several channels for potential dampening or amplification of these price dynamics. Inventory levels at wholesalers and retailers can provide a buffer against quick price changes, but only up to a point. Producer hedging strategies, longer-term contracts for energy and inputs, and shifts in crop planning could moderate the pace of price transmission. Conversely, sustained higher fuel costs, continued fertilizer price volatility, or disruptions in fertilizer supply could prolong inflationary momentum in the food-and-beverage sector.

Important sector-specific signals: tomatoes and vegetables among the largest movers Among the components driving the March input inflation rise, tomatoes and vegetables stood out with double-digit year-over-year increases—tomatoes around 102 percent and vegetables near 90 percent. These sharp moves reflect the sensitivity of certain produce categories to input costs and climate-related supply dynamics, as well as the energy components tied to cold storage and transportation. While some of these price spikes may reflect temporary bottlenecks or seasonal factors, the magnitude underscores the potential for broader price transmission if higher costs persist across the supply chain.

The fertilizer dimension: urea as a bellwether Urea’s price trajectory—doubling to approximately $900 per metric ton—serves as a bellwether for nitrogen-based fertilizer costs globally. As fertilizer represents a substantial expense for growers, sustained elevation in its price can influence planting decisions, soil management practices, and overall agricultural input profitability. Even if farmers optimize fertilizer usage, higher baseline costs can show up in wholesale produce prices as growers seek to preserve margins.

Planned and potential policy responses Policy makers and industry stakeholders are likely to monitor inputs closely and consider supply-side and market-stability measures. Potential avenues include:

- Fertilizer supply chain assurances: assuring steady access to nitrogen inputs through domestic production, diversified sourcing, or strategic reserves could reduce price volatility.

- Energy-market interventions: stabilization of diesel and fuel prices through wholesale energy programs or efficiency incentives for transport and logistics could mitigate downstream cost pressures.

- Agricultural and rural support: programs that improve farm productivity and resilience—such as precision agriculture, better irrigation management, and soil health initiatives—could help manage input intensity and long-run costs.

- Trade and tariff considerations: maintaining open trade in key inputs and avoiding protectionist barriers that raise costs for farmers and food producers.

Regional and global comparisons for context Across major food-producing regions, input inflation follows a familiar logic: higher input costs tend to creep into wholesale food pricing, particularly for perishable goods. Regions with diversified energy sources, efficient logistics, and robust farming infrastructure may fare better in stabilizing prices, while areas susceptible to fuel price spikes or fertilizer supply shocks often experience more pronounced inflation in agricultural products.

The road ahead: forecasting and resilience Forecasts suggest that wholesale food prices will be shaped by a combination of fertilizer availability, energy costs, weather patterns, and global commodity markets. If fertilizer prices stabilize or retreat from the current highs and energy costs ease, wholesale inflation might ease accordingly. However, any sustained disruptions—whether due to supply chain bottlenecks, geopolitical tensions, or climate-related shocks—could maintain upward pressure on prices across the food and beverage sector.

Public reaction and market sentiment Public reaction to rising input and wholesale prices typically centers on two questions: when will grocery prices reflect these higher costs, and how will households adapt to potential budgetary pressures? Retailers may respond with promotions, product assortment adjustments, and inventory strategies designed to balance affordability with margins. Consumers may alter purchasing patterns—prioritizing value, seeking seasonal or local options, and adjusting meal planning to accommodate fluctuating price points.

Sustainability considerations in the equation As producers navigate higher input costs, there is renewed emphasis on sustainability and efficiency. Investments in crop genetics, precision agriculture, and improved supply chain transparency can contribute to reducing waste and optimizing input use. Over the medium term, sustained improvements in productivity and energy efficiency may help offset some of the inflationary pressures seen in fertilizer and fuel.

Conclusion: a cautious but proactive outlook The March uptick in input inflation for US food and beverage producers reflects a convergence of higher energy costs, elevated fertilizer prices, and the ongoing challenges of distributing perishable goods through complex supply chains. While the magnitude of the current rise is notable, the sector has multiple levers to moderate or amplify future price moves, including hedging strategies, operational efficiency, and policy interventions designed to stabilize essential inputs. The broader message for households is clear: watch the sequence from farm input costs to grocery cart prices, as shifts at any link in the chain can influence the cost of everyday meals in the months ahead.

Note on scope and context This article synthesizes March data on input inflation, fertilizer pricing trends, and their implications for wholesale and retail food prices, while providing historical perspective, regional considerations, and discussion of potential policy responses. The aim is to present a balanced, fact-based view suitable for a general audience seeking to understand how upstream costs can shape downstream prices without political commentary.