Oil Prices Show Historic Regional Divergence Amid Middle East Disruptions

A Record-Breaking Split in Global Oil Prices

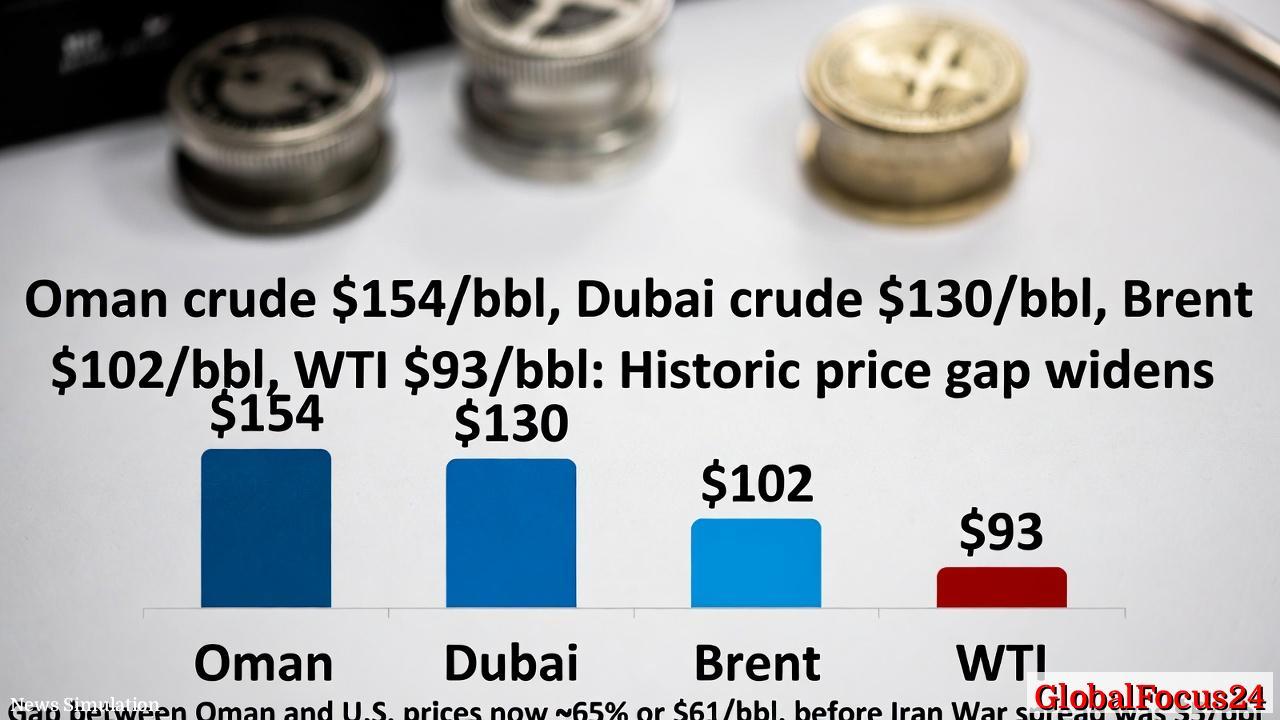

Global oil markets are facing an unprecedented schism as regional price benchmarks diverge to record levels following continued disruptions in the Middle East. Oman crude surged past $150 per barrel for the first time on record this week, reaching approximately $154, while Dubai crude climbed to around $130 per barrel. In stark contrast, Brent crude—the primary international benchmark—hovered near $102 per barrel, and West Texas Intermediate (WTI), the U.S. standard, traded around $93 per barrel.

The gap between Oman and U.S. prices has now widened to a historic $61 per barrel, a roughly 65 percent premium. Analysts note that such a wide spread between regional benchmarks has not occurred in decades, revealing the scale of dislocation in global energy flows since the outbreak of the Iran War earlier this year.

Only two months ago, in January and February, the spread among major benchmarks was just $5 per barrel. Today’s extreme divergence underscores how unevenly the conflict’s supply shock has rippled through global energy markets.

The Impact of Middle East Supply Disruptions

At the center of the crisis lies the continued closure of the Strait of Hormuz, the strategic waterway through which roughly one-fifth of globally traded oil normally flows. Escalating military tensions and attacks on tanker routes have limited crude exports from key Gulf producers, including Oman and the United Arab Emirates. The physical disruption has pushed Middle Eastern crude prices sharply higher, even as Western benchmarks lag behind.

Energy traders describe current conditions as “two-tiered”: a local scarcity of crude in the Gulf region contrasted with still-ample inventories in Europe and North America. Brent and WTI prices, less directly affected by physical constraints, reflect short-term market buffers such as emergency reserves and strategic stockpiles. However, those cushions may prove temporary.

If the Strait of Hormuz does not reopen soon, market participants expect the gap between benchmarks to narrow—but not through falling Middle East prices. Instead, Brent and WTI are expected to reprice sharply higher as Western inventories are drawn down.

Historical Context: Echoes of Past Oil Crises

The current pricing dynamic recalls earlier energy shocks that reshaped global markets, though none matched the regional imbalance seen today. During the 1973 oil embargo, all major benchmarks surged nearly in unison, driven by coordinated OPEC supply cuts. The 1990 Gulf War likewise caused a broad rally across crude types, with prices rising together as fears of sustained disruption spread worldwide.

In contrast, today’s divergence is rooted in geography and logistics more than political coordination. Middle Eastern producers face logistical bottlenecks at export terminals, while Western refiners remain temporarily insulated by previously shipped cargoes. The divergence also highlights changes in the global oil landscape: shorter supply chains, more regionally concentrated production, and a proliferation of distinct benchmark crudes that reflect localized market fundamentals.

Market historians agree that no previous oil shock has generated such a prolonged and wide differential among key crude grades. The scale of the current gap suggests deep fragmentation in global energy pricing—a sign, some analysts say, of a return to a more localized world energy system.

Economic Repercussions Across Regions

The ripple effects of this divergence are already visible across global economies. In the Middle East and parts of Asia reliant on Gulf crude, the surge in local oil prices is straining import costs, raising inflation, and pressuring government budgets. Countries like India, which import large volumes of Oman and Dubai blends, face steeply rising energy bills and potential fiscal deterioration if prices remain near current levels.

In contrast, U.S. and European consumers have so far been partially shielded. Retail fuel prices in North America, for example, have risen modestly but remain well below peaks seen during past crises. This temporary cushion stems from abundant domestic production, especially in the U.S. shale sector, and strategic petroleum reserves that continue to offset import disruptions.

However, experts caution that this relative stability may not last. Should Middle Eastern exports remain curtailed beyond the next few weeks, Brent and WTI prices will likely rise as Western inventories deplete. In that scenario, global energy inflation would accelerate rapidly, affecting not only fuel prices but also shipping, manufacturing, and food costs worldwide.

The Role of the Strait of Hormuz

The Strait of Hormuz remains the linchpin of the global oil system. Roughly 21 million barrels per day pass through the narrow passage connecting the Persian Gulf to the Arabian Sea. Its closure has immediate and severe repercussions for oil exporters in the Gulf Cooperation Council (GCC) and for import-dependent economies across Asia.

Efforts to restore safe passage have been hampered by continued naval skirmishes and diplomatic deadlock. Several regional navies have increased patrols, but commercial traffic remains limited as insurers withdraw coverage for vessels traversing the area. Industry experts compare the current situation to “a global pipeline suddenly switched off.”

If the strait remains closed, tankers may be rerouted around the Arabian Peninsula, adding weeks to delivery times and escalating freight costs. Some Gulf exporters, notably Saudi Arabia, have limited alternative routes via pipelines to the Red Sea, but their capacity falls far short of normal export volumes. This constraint further amplifies upward pressure on Oman and Dubai crude prices, as buyers compete for limited spot shipments.

Short-Term Market Reactions

Financial markets have responded with heightened volatility. Futures trading volumes in Oman crude have surged, reflecting intense demand for hedging and speculation. Traders report wide bid-ask spreads and extreme daily swings, with intraday price movements exceeding 10 percent in some sessions.

Brent and WTI futures remain more liquid but are beginning to show signs of contagion. Forward price curves have shifted into steep backwardation—a pattern indicating immediate demand far outstripping future supply expectations. Refiners are reportedly scrambling to secure physical cargoes, fearing that replacement deliveries could become unavailable within weeks.

Energy equities have rallied alongside crude prices, while airline and shipping stocks have fallen sharply. Global bond yields edged up as investors priced in inflationary risks. Currency markets also reacted, with oil exporters’ currencies strengthening and major importers’ currencies, including the Indian rupee and Japanese yen, coming under renewed pressure.

Potential Scenarios for Market Evolution

Analysts outline two primary scenarios for how this divergence may evolve in the coming months:

- Resolution and Rebalancing: If diplomatic negotiations succeed in reopening the Strait of Hormuz, physical oil flows could normalize rapidly. Under this scenario, Oman and Dubai prices would likely decline from record levels, narrowing the spread with Brent and WTI back toward historical norms of $3–$6 per barrel.

- Prolonged Disruption and Global Repricing: If the closure persists, global inventories would steadily drain, pushing Western benchmarks sharply higher. Brent could climb above $120 per barrel within weeks, while WTI might approach parity with Asian crude as the shortage becomes global.

Both paths carry significant economic implications. A swift resolution would stabilize inflation expectations and restore confidence in global trade routes. A prolonged crisis, however, could trigger a broad commodity shock reminiscent of the 2008 price surge, when oil briefly exceeded $140 per barrel and contributed to a global economic slowdown.

Broader Implications for Energy Security

Beyond immediate market mechanics, the current crisis raises deeper questions about energy security and supply diversification. The extreme premium on Oman crude reflects how concentrated the world’s oil supply chain remains in a few vulnerable chokepoints. Despite decades of investment in alternative pipelines and maritime routes, global dependencies on the Strait of Hormuz remain largely unchanged.

Several governments are accelerating contingency planning. Asian importers are exploring increased purchases from West Africa and Latin America, while the United States has signaled readiness to release additional barrels from its Strategic Petroleum Reserve if global supply tightens further. Meanwhile, major oil companies are reassessing their shipping and insurance arrangements, anticipating prolonged volatility in Gulf trade.

Energy analysts say the episode may also accelerate investment in renewable energy and liquefied natural gas infrastructure, as nations seek to reduce exposure to geopolitical flashpoints. Yet such transitions take years to bear fruit, leaving the world economy highly sensitive to events in the Middle East in the short term.

A Market at a Crossroads

The unprecedented divergence in regional oil benchmarks signals a global energy system under acute stress. While Brent and WTI prices remain relatively subdued for now, the underlying tensions suggest that this calm may be temporary. Oman and Dubai crudes are broadcasting what the rest of the market is likely to feel soon: that the world’s buffer of spare capacity and supply flexibility has eroded.

As traders, refinery managers, and policymakers watch developments in the Strait of Hormuz, the stakes could hardly be higher. Whether the global oil system rebalances or fractures further will depend not only on geopolitics but also on how quickly economies can adapt to a new era of regionalized energy prices and fragile trade routes. For now, the widening gulf between Middle East and Western oil prices stands as a stark reminder of how interconnected—and precariously balanced—the global energy network remains.