Global Demand for US Dollar Reaches Record Highs with Offshore Deposits at $14.5 Trillion

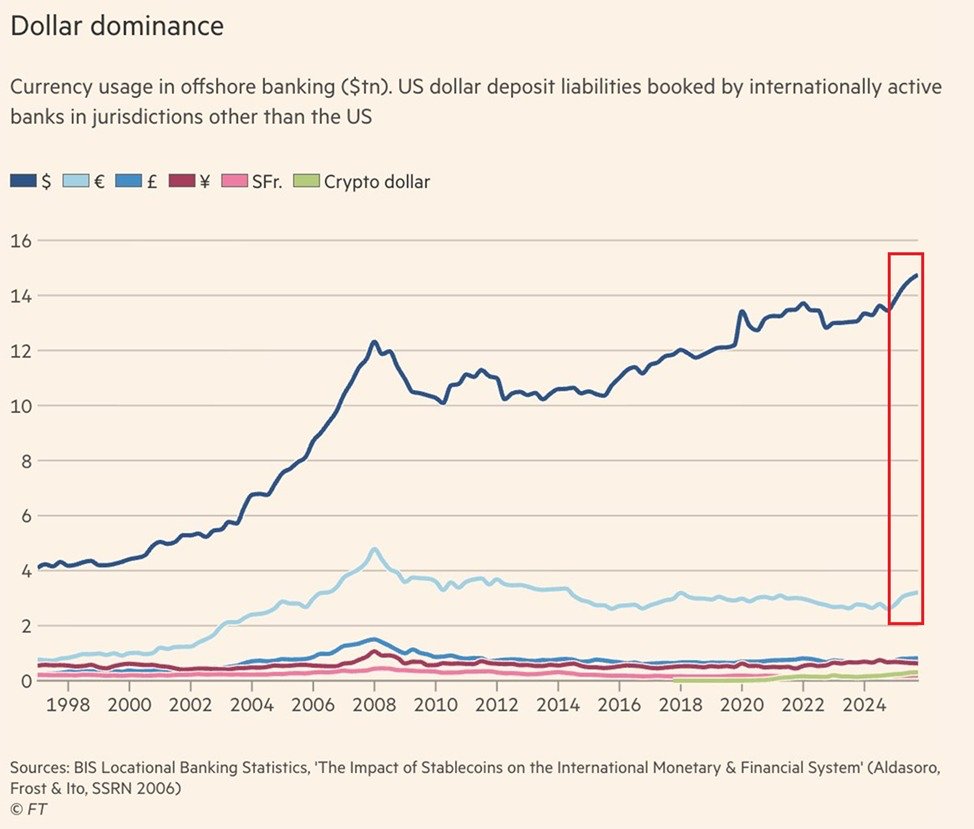

Offshore US dollar deposits held in banks outside the United States have climbed to a record approximately $14.5 trillion, marking a 220% increase from around $4.5 trillion at the start of the century. By comparison, offshore euro deposits held outside the Eurozone stand at roughly $3.5 trillion. Meanwhile, the Federal Reserve and domestic US commercial banks hold over $19.0 trillion in US dollars. This positions offshore US dollar deposits at about 43% of US domestic bank deposits, a level unmatched by any other currency. The figures underscore sustained and growing international demand for the US dollar as a primary medium for global transactions, reserves, and financial holdings.

Historical context and framework The trajectory of offshore US dollar deposits mirrors the broader evolution of the international monetary system since the early 2000s. After the 2008 financial crisis, policymakers across the globe sought safe, liquid assets to anchor balance sheets and manage exchange-rate risk. The dollar’s status as the world’s residual liquidity, reinforced by deep and diversified financial markets, contributed to a steady flow of dollars into international banking centers. In parallel, emerging economies accelerated import and trade invoicing in dollars, even as domestic currencies expanded their own roles in regional markets. The data, though transforming over time, consistently point to a singular theme: the dollar remains the preeminent reserve and settlement currency for international finance.

Economic implications for global markets

- Global liquidity and settlement efficiency: The abundance of offshore dollar deposits supports smoother cross-border payments, lowers settlement risk, and enhances the ability of banks to manage short-term funding needs. In times of market stress, the depth of dollar funding channels often proves a stabilizing factor for global liquidity.

- Interest rate transmission and funding costs: Large pools of offshore dollar deposits influence the availability and cost of dollar funding for banks outside the United States. Banks with substantial offshore dollar liabilities may experience heightened sensitivity to shifts in US monetary policy, which can ripple through funding costs for global borrowers and impact lending standards in multiple regions.

- Reserve diversification and macro risk management: Central banks and sovereign wealth funds often accumulate dollar-denominated assets to diversify reserve holdings, balance risk, and maintain credibility in exchange-rate anchors. The scale of offshore deposits reinforces the dollar’s role as a central pillar of international reserve portfolios, shaping investment allocations and currency hedging strategies worldwide.

Regional comparisons and regional dynamics

- Europe and the United Kingdom: Offshore dollar activity has long linked to financial hubs such as London and, more recently, Dublin, Luxembourg, and other centers that provide liquidity, custody services, and dollar-denominated instruments. While euro-denominated offshore deposits remain substantial, the relative dominance of the dollar in trade invoicing and financing supports the sustained growth of offshore dollar liabilities.

- Asia-Pacific: In Asia, the dollar’s influence is pronounced through trade finance, cross-border settlements, and wholesale funding markets. Singapore, Hong Kong, and Tokyo function as key offshore centers where banks manage dollar liquidity, currency hedging, and correspondent banking relationships. The region’s growing imports and investment flows keep dollar liquidity at elevated levels, even as regional currencies pursue greater internationalization.

- the Middle East and Africa: Offshore dollar deposits there reflect a mix of sovereign wealth fund activity, commodity pricing dynamics, and the strategic use of dollar-denominated instruments to stabilize budgets and financing. These regions often exhibit a high sensitivity to US policy signals given their trade ties and commodity pricing practices.

- Latin America: Cross-border trade, remittance flows, and dollar-denominated funding in Caribbean and South American markets illustrate how offshore dollar deposits support regional financing needs, particularly in economies with volatile local currencies.

Policy considerations and risk factors

- Monetary policy spillovers: Large offshore dollar deposits amplify the transmission channels of US monetary policy. Changes in the Federal Reserve’s policy stance can influence global liquidity conditions, funding costs, and the availability of USD-denominated credit in foreign banking systems.

- Currency stability and hedging costs: For countries with significant offshore dollar activity, currency reserves and hedging strategies must adapt to fluctuations in dollar valuation. This dynamic can affect inflation, import prices, and balance-of-payments pressures in economies that rely heavily on US-dollar financing.

- Regulatory evolution: International standards and cooperation in banking supervision, capital adequacy, and anti-money-laundering controls shape how offshore centers manage dollar deposits. Ongoing regulatory alignment aims to preserve financial integrity while sustaining liquidity access for global markets.

What the numbers reveal about global finance

- A persistent preference for the dollar: The size of offshore dollar deposits signals a broad trust in the dollar’s reliability and depth. Market participants continue to view dollars as a readily usable asset for settlement, risk management, and reserve adequacy.

- The safety and flexibility of dollar funding: Banks operating outside the United States benefit from the dollar’s liquidity profile, especially during market stress when access to other currencies may tighten. This has historically made dollar-denominated funding a preferred option for cross-border activities.

- The interconnectedness of financial systems: The offshore dollar footprint underscores how deeply integrated global financial networks are. Movements in US monetary conditions, geopolitical developments, or shifts in global trade can quickly propagate through offshore centers, influencing lending, capital flows, and investment decisions worldwide.

Public sentiment and market behavior Investors and corporate treasurers monitor offshore dollar deposits as an indicator of global liquidity appetite. In periods of heightened uncertainty, demand for safe-haven assets and USD liquidity tends to rise, reinforcing offshore pools of dollars. Conversely, when global growth accelerates and diversification widens, some entities may shift toward alternative currencies or diversify funding bases, though the dollar’s dominance remains resilient.

Historical milestones and comparable contexts

- 20th-century anchors: The post-World War II era established the dollar as a central reserve asset, with the Bretton Woods system shaping early global finance. Even after the transition to floating exchange rates, the dollar’s liquidity and depth remained unmatched.

- Post-2000s shifts: The rise of globalization and technologically advanced financial markets expanded the reach of dollar transactions. Offshore centers leveraged these developments to offer services that attract dollar deposits from a broad spectrum of clients, including multinational corporations, sovereigns, and financial institutions.

- 2020s resilience: Despite regional policy experiments and currency diversification debates, the dollar’s position in international finance persisted. The record offshore deposits reflect both ongoing reliance on dollar-denominated instruments and strategic considerations by foreign institutions managing exchange-rate risk and funding needs.

Implications for domestic institutions

- US monetary policy posture: Domestic banks and the Federal Reserve monitor global dollar flows as part of a broader understanding of liquidity conditions. Offshore deposits influence the global availability of dollar liquidity, which can interact with US funding markets and policy transmission.

- Banking sector health: A robust ecosystem of offshore dollar deposits supports the liquidity of international banks, potentially affecting cross-border lending and the stability of global financial networks. U.S. banks, as the core issuers of dollar liquidity, continue to benefit from deep, diversified access to funding channels.

Future outlook and scenarios

- Scenario A: Sustained dollar dominance with gradual diversification: Offshore dollar deposits consolidate at elevated levels while regional centers expand non-dollar offerings. This balances the dollar’s global role with broader diversification in international finance.

- Scenario B: Dollar liquidity under pressure: If US policy shifts lead to tighter global dollar funding conditions, offshore deposits could respond with tighter liquidity or re-pricing of dollar-denominated liabilities. Markets would likely recalibrate funding strategies accordingly.

- Scenario C: Fragmentation and regionalization: Some regions accelerate inward-looking financial strategies, increasing currency diversification and local settlement infrastructures. The dollar would remain prominent but encounter intensified competition from alternative currencies in specific niches.

Bottom line The record-high offshore US dollar deposits highlight the ongoing centrality of the greenback in global finance. As banks and sovereigns manage liquidity, funding, and reserves across borders, the dollar’s reach extends beyond domestic shores, shaping cost structures, investment decisions, and policy debates around the world. In a landscape of evolving monetary policy, geopolitical shifts, and rapid technological change in financial services, the dollar’s role as a global medium of exchange and store of value remains a defining pillar of modern finance.