Global Investors Flock to Cash Amid Rising Tensions and Market Volatility

Surge in Cash Holdings Marks Sharp Shift in Sentiment

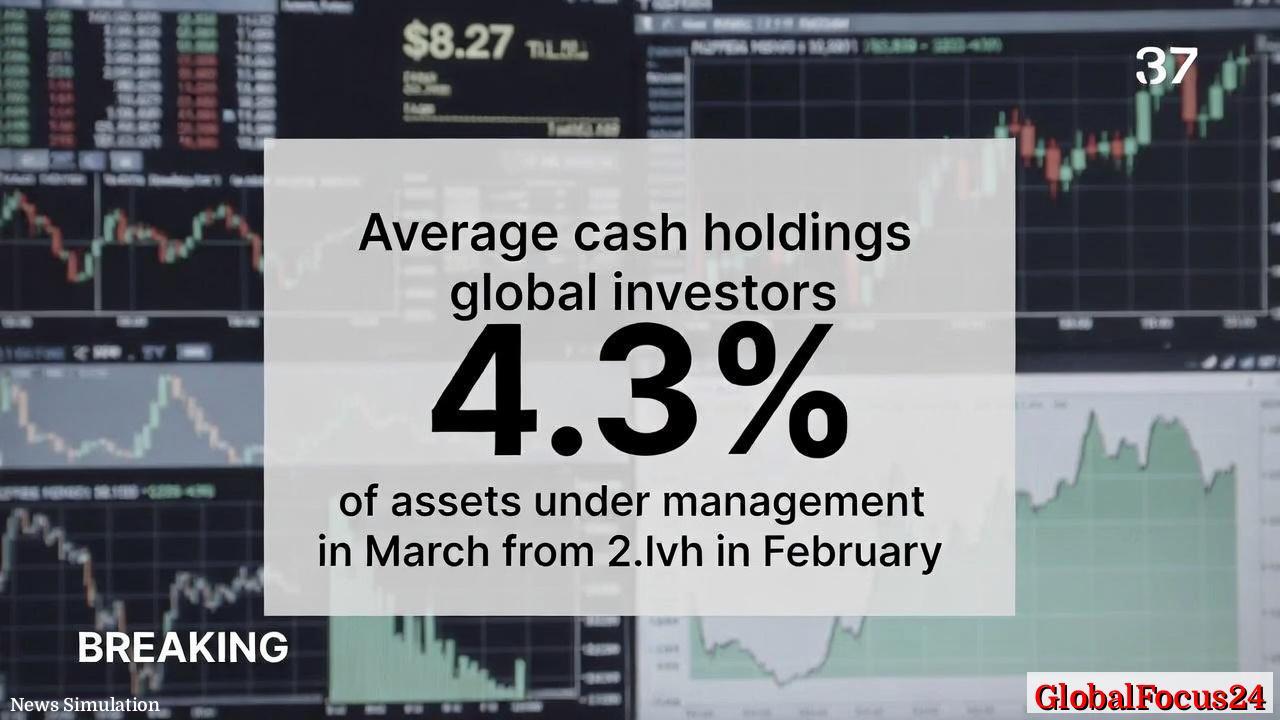

Global investors are retreating from risk and moving into cash at the fastest pace since the onset of the COVID-19 pandemic, signaling growing alarm over escalating conflict involving Iran and its potential to disrupt global markets. Average cash holdings in portfolios surged to 4.3 percent of total assets under management in March, up from 3.4 percent the previous month — the largest monthly increase since March 2020, when pandemic uncertainty gripped the world economy.

The defensive repositioning underscores a sharp reversal from the risk-on sentiment that dominated markets through late 2025. With geopolitical tensions flaring and crude oil prices climbing toward $100 per barrel, fund managers have responded by seeking the safety and liquidity of cash and money market instruments, reflecting deep concern about both inflation and the stability of global trade.

Escalating Conflict and Fear of Economic Disruption

The immediate catalyst for the shift has been the escalating military conflict involving Iran, which has intensified investor fears of a wider regional war spreading through the Middle East. Analysts warn that any disruption to the Strait of Hormuz — through which about 20 percent of global oil supply passes — could send energy prices soaring, triggering a new wave of inflation and economic volatility.

Brent crude futures have already surged amid speculation that further sanctions and military escalation could choke supply from the Gulf. Energy analysts note that if Brent prices consistently exceed $100 per barrel, the resulting cost pressures could force central banks to delay interest rate cuts, unsettling markets that had been anticipating a gradual easing of monetary policy in 2026.

A Retreat to Liquidity as Volatility Builds

Money market funds have emerged as a primary refuge. U.S. money market assets reached record highs this month, approaching $8.27 trillion as investors poured capital into short-term, low-risk instruments. Portfolio managers have trimmed equity exposure and scaled back allocations to corporate bonds, citing heightened uncertainty and the lack of traditional safe havens.

Cash-rich positioning is not new in times of geopolitical instability, but the scale and speed of the recent shift are striking. Historically, similar rotations occurred during the oil shock of 1973, the Gulf War in 1990, and the early weeks of the pandemic in 2020. Each episode reflected a sudden tightening of investor risk tolerance as global supply chains and commodity flows came under threat.

Fund managers now describe the current climate as "a holding pattern," characterized by minimal new equity commitments and a focus on preserving liquidity. The sentiment index tracking global investor optimism has fallen to its lowest reading in several years, underscoring the growing skepticism about near-term market stability.

Regional Comparisons Reflect Diverging Risk Views

The trend toward cash holdings has played out unevenly across regions. In the United States, domestic-focused fund managers have adopted a more measured approach, maintaining limited exposure to technology and defensive sectors while parking excess liquidity in money market instruments. The Federal Reserve’s cautious tone on rates has added to the appeal of cash, as yields remain relatively attractive compared to dividend returns from equities.

In Europe, investors have turned notably defensive. The continent’s heavy dependence on imported energy makes it especially sensitive to oil price shocks, prompting institutional investors to pivot toward safe government bonds and higher cash balances. Meanwhile, Asian markets have shown mixed reactions. Japanese institutions, buoyed by the yen’s status as a traditional haven, have actually seen inflows into domestic assets. However, emerging market portfolios have experienced accelerated outflows as investors reassess geopolitical exposures tied to global shipping routes.

Oil Prices and Inflation Fears Reignite

The specter of surging oil prices has intensified fears of renewed inflationary pressures, particularly just as many economies had begun to stabilize from elevated price levels in recent years. Analysts caution that sustained high energy prices could ripple through sectors including manufacturing, transportation, and consumer goods. Rising fuel costs often lead companies to pass expenses onto consumers, potentially eroding purchasing power and slowing economic growth.

Central banks face a delicate balancing act. In the United States, the Federal Reserve has signaled a willingness to adjust its policy stance if inflationary pressures reemerge, though officials insist they will not respond hastily to short-term commodity shocks. Similarly, the European Central Bank has maintained a neutral tone, but markets are already pricing in potential delays to interest rate cuts. This policy uncertainty has further reinforced the appeal of holding cash, a flexible buffer in volatile times.

The Psychological Dimension of Market Caution

Beyond economic fundamentals, psychology plays a critical role in shaping market behavior. The abrupt spike in cash allocation reflects a broader crisis of confidence — not only in equity valuations but in the reliability of global systems that support trade and investment. In uncertain geopolitical climates, investors often prioritize flexibility, preferring liquid holdings that allow rapid repositioning as conditions evolve.

Risk models have also been recalibrated to reflect higher geopolitical volatility, amplifying the reflexive shift toward cash. Many asset managers note that while some sectors could benefit from instability, such as defense and energy producers, most institutional portfolios are structured for stability, not speculation during wartime scenarios.

Comparisons to Previous Flight-to-Safety Episodes

The current rotation echoes past market reactions to global crises. During the early days of the pandemic, investors also swarmed to cash and money market funds as equities tumbled. Similarly, in the aftermath of the 9/11 attacks and the 2008 financial crisis, liquidity became paramount, driving massive inflows into short-term U.S. Treasuries and cash equivalents.

However, there are key differences today. In those prior episodes, central banks intervened aggressively, cutting rates and injecting liquidity to calm markets. In 2026, many central banks have less room to maneuver, constrained by elevated debt levels and lingering inflation risks. That limitation partly explains why this wave of risk aversion may persist longer than past cycles.

Broader Economic Impact of Investor Caution

The reallocation toward cash carries broader economic consequences. Rising demand for money market instruments tends to compress short-term yields, while reducing liquidity in equity and corporate bond markets. Companies seeking to raise capital may find conditions tighter, particularly smaller firms reliant on public issuance. A prolonged period of defensive positioning could dampen overall investment, slowing economic recovery and curbing corporate expansion.

On the consumer side, persistent volatility and high energy prices could weaken confidence, affecting spending patterns and slowing demand growth. Economists warn that if geopolitical tensions escalate further, the resultant slowdown could test the durability of the current global recovery.

Emerging Outlook and Risk Scenarios

For the near term, financial strategists outline two potential paths. The first assumes that diplomatic channels stabilize the conflict, easing oil prices and restoring a measure of predictability. Under that scenario, pent-up liquidity could quickly reenter risk assets, fueling a rebound in equity markets. The alternative — a protracted standoff and enduring price pressures — risks entrenching caution and drawing out the global shift toward ultra-defensive postures.

Some investors are positioning for both outcomes, maintaining higher cash reserves while selectively buying into sectors seen as resilient under stress: defense, energy infrastructure, and commodities. Others are holding cash outright, preferring to wait until market volatility subsides.

A Cautious Wait-and-See Phase

Ultimately, this sharp move into cash highlights a transition to caution not seen since the height of the 2020 pandemic. The escalation in Iran has crystallized broader anxieties about global stability, supply chain dependencies, and the fragility of post-pandemic recovery. For now, liquidity reigns supreme — not as a long-term investment strategy, but as a temporary safe harbor in a world once again tilting toward uncertainty.