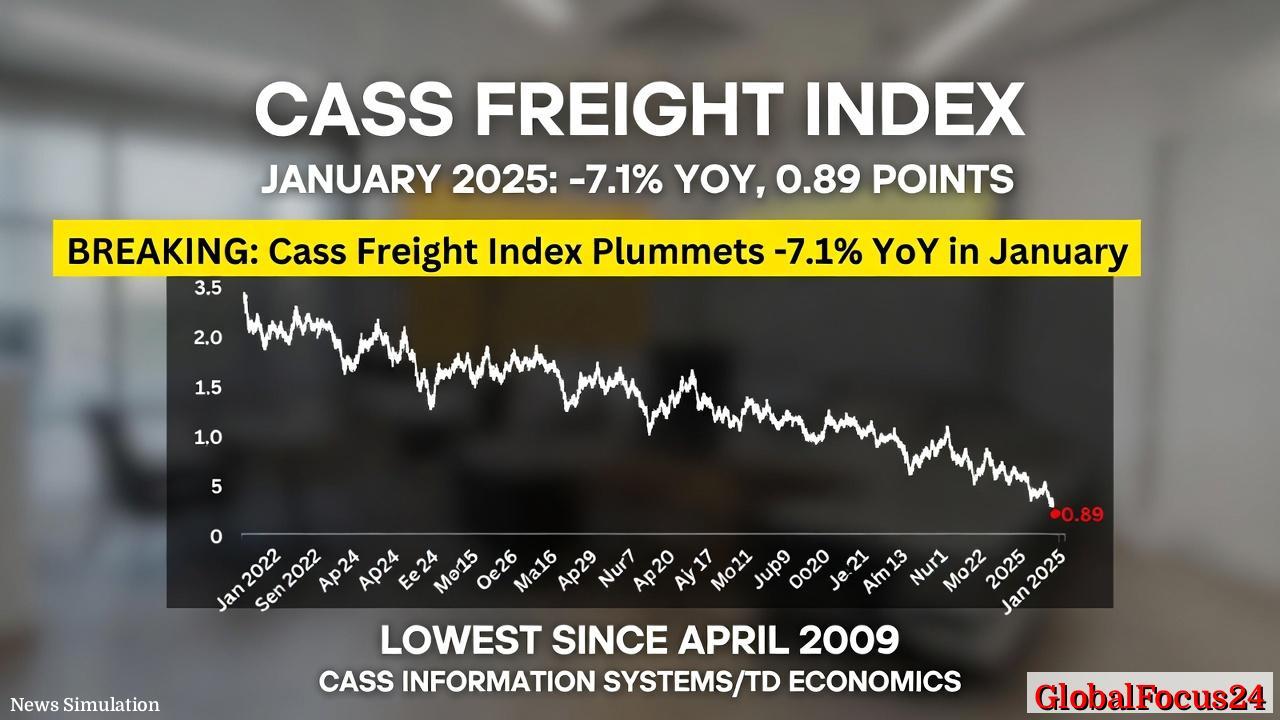

GLOBAL CARGO TRENDS: JANUARY SHIPMENTS FALL TO NEW CYCLE LOWS WITH ROUGH ECONOMIC RATTLE

In January, the Cass Freight Index recorded a year-over-year drop in shipments of 7.1%, marking a new cycle low and signaling sustained softness in the freight landscape. The index closed at 0.886 (with January 1990 equal to 1.00), underscoring a continued downward trajectory that began in 2022 and has persisted into 2026. On a monthly basis, shipments fell 4.9%, or 2.0% when seasonally adjusted, reflecting a moderation in activity after an earlier surge in shipments during the pandemic era. These numbers collectively paint a picture of subdued demand across freight networks, with implications for manufacturers, retailers, and logistics providers.

Historical context: a long arc of decelerating freight demand

- Since 2022, the Cass Freight Index has traced a downward path as macroeconomic cooling, inventory adjustments, and evolving supply chains affected shipping volumes. The January 2026 low point reinforces a structural shift that many shippers have been preparing for, even as some sectors intermittently show pockets of resilience. Historical patterns suggest that freight volumes often respond to shifts in consumer demand, industrial activity, and global trade dynamics, making this cycle particularly sensitive to indicators of inventory restocking and business investment. The January 2026 data point aligns with a broader trend toward tighter freight activity seen in prior years, highlighting a transition from post-pandemic normalization to a more balanced or cautious operating environment for freight carriers.

Economic impact: costs, capacity, and pricing signals

- Expenditures rose modestly on a year-over-year basis by 0.6%, yet fell 3.6% month-over-month, signaling that shippers are moderating spending and seeking efficiency as volumes retreat. Truckload linehaul rates, meanwhile, increased by 3.2% year-over-year and 1.7% month-over-month, suggesting ongoing pressure on transportation costs even as overall freight activity cools. Together, these figures imply a freight market navigating higher per-shipment costs amid softer demand, potentially compressing carrier margins and influencing contract negotiations across industries. For regional economies with heavy logistics footprints, such as the West Coast and intermodal hubs, this mix could translate into slower throughput at ports, greater emphasis on return-to-ship planning, and investment in capacity management to align with demand cycles.

Regional comparisons: where the pressures are felt most

- On the West Coast, global supply chain realignments and inventory recalibrations have historically weighed on freight volumes, with shipments sensitive to retail restocking and manufacturing cycles. The Midwest, a core manufacturing belt, often experiences more pronounced sensitivity to freight pricing and capacity because industrial activity drives both inbound components and outbound finished goods. The Southeast, closely tied to e-commerce and consumer goods distribution, may view steadier demand in some periods but remains susceptible to tightening macroeconomic conditions that curb freight spend. The Northeast, with its dense distribution networks and cross-border trade dynamics, can experience sharper swings in volumes during early-year cycles as businesses adjust inbound materials and outbound shipments. Overall, the January data underscore a nationwide trend rather than a regional outlier, but the degree of impact will continue to vary by sector, port activity, and the strength of consumer demand in each region.

Industry implications: carriers, shippers, and policy considerations

- Carriers face the reality of leaner volumes and tighter capacity discipline, which can lead to selective rate adjustments and more competition for higher-margin lanes. Shippers are likely to prioritize freight spend optimization, mode mix optimization, and longer-term contracts that stabilize costs in a volatile environment. Policy considerations around infrastructure investment, border efficiency, and multimodal connectivity could influence freight dynamics by reducing transit times and improving reliability, thereby supporting a more predictable cost structure for businesses. In markets with concentrated logistics activity, small shifts in demand can magnify pricing signals, underscoring the importance of data-driven capacity planning and visibility across the supply chain.

Comparative outlook: how this cycle compares to peers

- Compared with the pre-pandemic era, today’s freight cycle exhibits a more deliberate pace of recovery, with inventory normalization and demand calibration playing larger roles in shaping volumes. Unlike periods of rapid growth, where capacity could quickly tighten and rates surge, the current environment reflects a cautious expansion, with shipments retreating and expenditures showing mixed signals from month to month. In major trading regions, the degree of price resilience varies, but the overarching pattern is one of careful cost management and strategic capacity deployment by logistics providers. As the market absorbs this January data, many stakeholders anticipate a gradual stabilization rather than a swift rebound, with improvements likely tied to consumer demand resilience, inventory discipline, and a measured recovery in industrial activity.

Public reaction and market sentiment: a sense of urgency tempered by realism

- Shippers and logistics managers are responding with heightened focus on end-to-end visibility, better demand forecasting, and more flexible contracting. Traders and carriers watch for catalysts that might spur a quick uptick in volumes, such as expedited restocking by retailers, easing supply chain bottlenecks, or policy signals supporting trade and infrastructure improvements. Public reaction in regions heavily invested in logistics centers often centers on pressure to maintain employment and sustain economic activity amid slower freight flows, while industry analysts emphasize the importance of strategic investments in digital freight solutions, automation, and network optimization to navigate the current cycle.

Looking ahead: potential triggers for a rebound

- A rebound in shipments could emerge from renewed consumer spending, a reacceleration in manufacturing orders, or renewed inventory restocking cycles across key sectors such as consumer electronics, automotive, and consumer packaged goods. Improvements in fuel efficiency, regulatory clarity, and cost-per-mile containment could also contribute to more favorable economics for carriers, encouraging capacity to align with demand. Regional port performance and cross-border trade dynamics will remain critical barometers, as smoother supply chains and faster transit times can translate into healthier volumes and more stable pricing for freight services.

Conclusion: navigating a cautious freight landscape

- The January 2026 Cass Freight Index reading reinforces a challenging but navigable freight environment, characterized by a downward shipments trajectory and mixed but consequential cost signals. For businesses reliant on timely delivery and efficient logistics, the current moment demands disciplined planning, robust data analytics, and adaptive mode strategies to weather ongoing volatility. As the market continues to absorb these levels, stakeholders across manufacturing, retail, and transportation will be watching for early signs of stabilization that might herald a more predictable trajectory for freight volumes and prices in the months ahead.