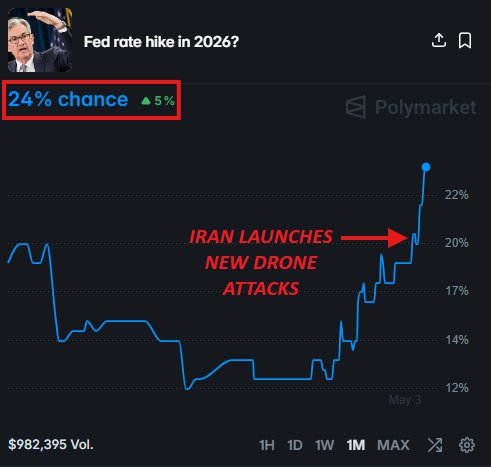

Fed Rate Hike Odds for 2026 Surge to 24% Amid Iran Drone Attacks on UAE

Introduction Market pricing has shifted decisively in response to recent geopolitical developments in the Middle East, with traders elevating the odds of a Federal Reserve rate increase in 2026 to about 24%. The beat of this revision comes as investors weigh the potential for oil price volatility, supply disruptions, and renewed inflation pressures stemming from Iran’s drone attacks on the United Arab Emirates. While policy remains uncertain, the new pricing reflects a broader reassessment of the inflation-growth trade-off and the risks that global energy markets could pose to U.S. economic momentum in the second half of the decade.

Historical context: a longer arc of policy and prices To understand the present shift, it helps to review the macro backdrop over the past decade. Following the global financial crisis, the Federal Reserve pursued a low-rate regime designed to support recovery and reassure markets. As growth strengthened, the central bank began tapering asset purchases and signaling gradual path normalization. Inflation, which had remained stubbornly subdued for years, accelerated in 2021–2022 amid supply-chain bottlenecks and resilient demand. The ensuing policy tightening cycle ran its course through 2023 and 2024, with the Fed navigating a delicate balance: restraining inflation without tipping the economy into a deep slowdown.

The 2020s have been characterized by a more complex inflation dynamic than in earlier cycles. Supply shocks, energy costs, currency fluctuations, and global demand shifts have all fed into a higher level of price volatility. In this context, market participants have increasingly priced rate paths that depend not only on domestic inflation readings but also on the outlook for energy markets, geopolitical risk, and the pace at which labor markets cool. The current pricing around a potential 2026 rate hike sits within a broader spectrum of scenarios that investors continuously reevaluate as new information arrives.

Economic impact: energy prices, inflation expectations, and growth Oil and gas prices play a pivotal role in any central bank’s calculus. The UAE, a key regional energy hub, sits at the intersection of global supply chains and geopolitical risk. When drone, missile, or other disruptive actions threaten energy flow or supply security, markets weigh the potential for price spikes and the knock-on effects for consumer energy bills, transportation costs, and broader inflation measures.

- Inflation dynamics: Higher energy costs tend to feed intoinflation through energy-sensitive components such as transportation, manufacturing, and services that rely on fuel for operations. If higher oil prices persist, monetary authorities may face heightened difficulty in damping inflation without dampening demand. The 2026 pricing implies that markets anticipate a scenario in which inflation pressures remain more persistent than previously expected, prompting cautious stance from policymakers.

- Growth considerations: Higher energy costs can dampen consumer spending power and raise production costs for businesses, especially those with energy-intensive operations. The result can be a slower pace of economic expansion, potentially elongating the adjustment period before a new cycle of rate cuts would be warranted.

- Financial conditions: Energy price movements influence broader financial conditions, including credit spreads, equity valuations, and currency fluctuations. When investors reassess risk, all these channels can tighten financial conditions, which in turn can influence the trajectory of monetary policy.

Regional comparisons: what this means for other economies The repercussions of Iran’s drone actions and the ensuing energy-market volatility extend beyond the United States. In Europe and parts of Asia, where energy imports and manufacturing exposures differ, the policy responses may diverge.

- Europe: The European Union remains sensitive to energy price shifts because of its reliance on energy imports and regional production structures. A sustained pull in oil prices could pressure inflation, complicating the European Central Bank’s battle against price pressures while balancing economic resilience for member states.

- Asia-Pacific: Countries in Asia with large energy import needs and open economies watch the developments with heightened attention. Central banks in the region may respond with calibrated policy moves to shield growth while managing inflation expectations. Supply chains and trade flows in East Asia could experience ripple effects from shifts in global energy pricing.

- Emerging markets: For commodity exporters and economies with flexible exchange rates, the energy-price environment can influence capital flows and financing conditions. Accurate risk assessment and hedging strategies become essential for corporate and sovereign borrowers alike.

Market psychology and public reaction Geopolitical tensions and energy-market uncertainty tend to spark a broad recalibration in investor sentiment. In many households and businesses, this translates into a more conservative stance on expenditures, longer planning horizons for investments, and increased attention to energy pricing forecasts. Public reaction often centers on the affordability of fuel and electricity, as well as the potential implications for employment and wage growth if higher energy costs persist.

Policy implications: what the market is signaling The price-based outlook for potential rate hikes in 2026 underscores several key policy considerations for the Federal Reserve and the broader economic architecture:

- Inflation sensitivity: If energy-driven price pressures continue to linger, the Fed may face a scenario where gradual policy tightening remains a tool to keep inflation anchored near the target without derailing growth. The 24% probability reflects a scenario in which policy normalization is cautiously extended into the latter part of the decade.

- Data dependence: The central bank’s approach would continue to hinge on incoming data, including employment metrics, wage dynamics, consumer prices, and broader inflation gauges. The trajectory would be subject to revisions as new information about energy markets and geopolitical developments emerges.

- Credit and liquidity conditions: Market expectations influence the shape of the yield curve and the availability of capital. A path that includes higher-for-longer expectations could affect borrowing costs for households and businesses, potentially influencing investment decisions and housing markets.

Technical considerations: interpreting the 24% probability Financial markets use a range of instruments to price policy expectations, including futures markets, options, and swaps. A 24% probability for a rate increase in 2026 signals that investors allocate a non-trivial chance to a policy adjustment, even if the baseline view remains for stability in the near term. This pricing often evolves with the data; a series of stronger inflation prints or unexpected energy price movements could push probabilities higher, while cooling inflation or a stabilizing energy market could pull them back.

Historical analogs and risk management Historically, rate-hike expectations have swung in response to energy shocks, geopolitical events, and shifts in inflation momentum. Investors who monitor these dynamics typically diversify across asset classes, employ hedges against energy-price exposure, and maintain liquidity to adapt to rapid policy shifts. For corporate treasurers and asset managers, the key is to balance short-term risk with long-term planning, recognizing that geopolitical risk can reconfigure the price landscape quickly.

What to watch next: indicators and catalysts Several indicators will be critical in the weeks and months ahead as markets digest the evolving situation:

- Crude oil benchmarks: Movements in Brent and West Texas Intermediate (WTI) prices will be a primary signal of energy-price risk pricing into policy expectations.

- Inflation readings: The trajectory of core andinflation will influence the Fed’s communications and the market’s anticipation of policy adjustments.

- Labor market data: Employment growth, wage inflation, and labor force participation will help determine the economy’s underlying resilience.

- Geopolitical developments: New information on risk to energy supply, regional stability, and potential escalations will inform risk pricing and policy interpretation.

Regional economic resilience: a look at supply chains and employment The interplay between energy markets and regional economies hinges on resilience built through diversified energy sources, strategic reserves, and efficient logistics networks. Areas with robust manufacturing bases or energy-intensive industries may experience more pronounced sensitivity to energy-price fluctuations, while regions with diverse energy portfolios and strong labor markets might better weather volatility. Workforce adaptability, investment in energy infrastructure, and policy support for energy efficiency can shape outcomes in the face of heightened risk.

Conclusion: navigating uncertainty with measured calm The surge in rate-hike odds for 2026 reflects a world where geopolitics and energy markets intersect with monetary policy in real time. While the immediate path for the Fed remains data-dependent, the market’s attention to Iran’s drone actions and their potential impact on oil prices underscores a broader truth: energy security and macroeconomics are deeply entwined. As investors monitor evolving developments, policymakers will balance the goals of price stability, sustainable growth, and financial market stability, aiming to navigate a landscape marked by volatility but guided by fundamentals. In this environment, prudent planning, transparent communication, and rigorous risk assessment will be essential for households, businesses, and institutions alike as they adapt to a dynamic economic horizon.