U.S. Dollar Bearish Sentiment Hits Fourteen-Year Low as Investors Shift Outlook

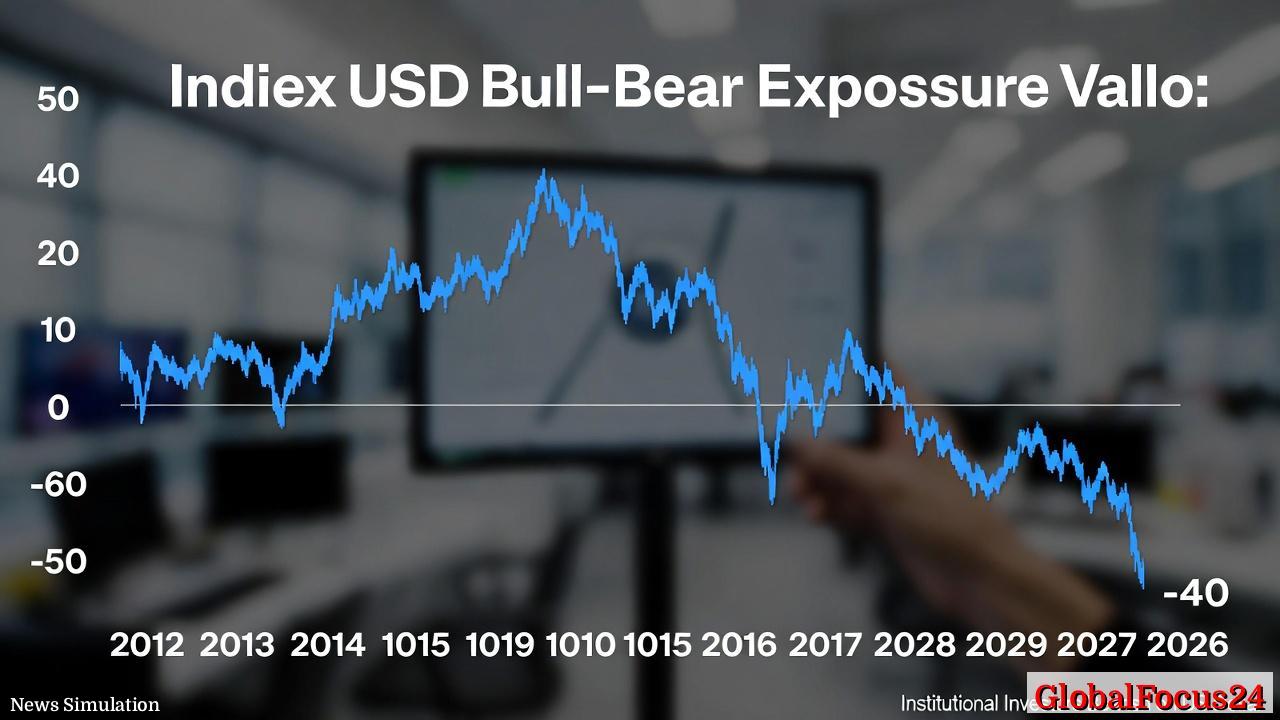

The U.S. dollar, long seen as the world’s most resilient currency, is facing a sharp downturn in investor sentiment. According to recent positioning data, exposure to the dollar has reached its most bearish level since January 2012. A key metric tracking investor outlook — the USD Bull-Bear Index — has fallen to roughly -40, signaling an intense pullback in confidence. The retreat marks a striking shift from the robust outlook that defined currency markets through much of 2024, as global investors recalibrate expectations for interest rates, inflation, and overall growth in the United States.

A Historical Slide in Dollar Sentiment

The USD Bull-Bear Index, which measures positioning on a scale from -100 to +100, offers a window into the global mood toward the dollar. A neutral value of zero represents balanced sentiment; values below zero indicate bearishness. The recent plunge to around -40 represents the most significant negative reading in over a decade, underscoring a widespread belief that the dollar may have peaked after multiple years of strength.

Historically, similar drops in sentiment have coincided with shifts in U.S. monetary policy or moments when global risk appetite favored higher-yielding or emerging-market currencies. The previous major low, recorded in early 2012, came as the Federal Reserve maintained near-zero rates during a fragile economic recovery, prompting investors to seek returns elsewhere. The parallels between that period and the early months of 2026 are striking: both reflect markets recalibrating after extended periods of dollar dominance.

Changing Expectations Around Fed Policy

One of the primary drivers behind the recent downturn in dollar sentiment is the evolving outlook for Federal Reserve policy. After several years of aggressive rate hikes aimed at controlling post-pandemic inflation, investors now anticipate a more accommodative stance. Inflation has slowed considerably from its 2022–2023 peaks, wage pressures are easing, and global growth concerns have resurfaced.

Markets are increasingly pricing in the possibility that the Federal Reserve could begin cutting rates later in 2026, reducing yields on dollar-denominated assets. Lower yields typically weaken a currency’s appeal to foreign investors, and speculative traders have been quick to adjust positions. This shift suggests a deep reassessment of the U.S. monetary path — from one of tight control to cautious support for economic stability.

Global Factors Amplifying the Dollar’s Retreat

The softening of the dollar is also part of a broader rebalancing across global markets. Europe and Asia have seen relative economic improvement, while several major emerging markets, notably India, Mexico, and Brazil, are reporting resilient growth and stronger capital inflows. These dynamics have encouraged a pivot away from the greenback toward regional currencies with more attractive short-term prospects.

China’s gradual economic stabilization following a difficult 2024 has also contributed to the dollar’s decline. The yuan has held relatively stable, reflecting efforts by Beijing to reassure investors and bolster domestic confidence. Furthermore, strong commodity prices have buoyed currencies such as the Australian and Canadian dollars, which benefit from renewed demand for natural resources tied to infrastructure and clean energy development worldwide.

A Look Back: When Dollar Sentiment Last Hit Bottom

The last major period of dollar pessimism in 2012 emerged in a context that, while different in detail, shared notable similarities. At that time, investors reacted to prolonged low interest rates, fiscal uncertainty, and a recovering but uneven global economy. The eurozone remained in crisis, yet the U.S. currency struggled to gain due to a perception that structural imbalances would weigh on long-term performance.

From that point forward, however, the dollar began a multiyear ascent, fueled by higher U.S. growth, relative strength in financial markets, and comparative weakness overseas. The current question for investors is whether history might repeat itself — with bearish positioning today laying the groundwork for a future rally if the U.S. economy proves more durable than expected.

Contrasting Regional Trends in 2026

Across the Atlantic, the euro has benefited modestly from the dollar’s weakness, gaining ground as investors bet on narrowing rate differentials between the U.S. and the eurozone. The European Central Bank, while maintaining a cautious tone, has indicated that further tightening may not be necessary, reassuring markets that Europe’s inflation trajectory is under control.

In Asia, the yen’s recovery from multi-decade lows has attracted attention, particularly as Japanese authorities maintain vigilance against excessive volatility. Meanwhile, commodity-linked currencies — such as the Canadian, Australian, and New Zealand dollars — have rallied on the back of high export demand and stable policy environments. These crosscurrents suggest investors are re-diversifying away from the dollar after a long period of one-sided positioning.

Economic and Market Impact in the United States

For the United States, a softer dollar presents both challenges and opportunities. On one hand, a weaker currency enhances the competitiveness of American exports, providing a potential boost to manufacturers and agricultural producers. U.S. companies with substantial overseas revenue could benefit from favorable exchange rates, improving earnings translated back into dollars.

On the other hand, dollar weakness increases import costs, potentially exerting mild upward pressure on prices at a time when policymakers aim to keep inflation contained. For consumers, imported goods — from electronics to energy — could become more expensive if the trend persists. Nevertheless, the overall effect is expected to remain moderate, especially if global supply chains continue to stabilize in 2026.

Investor Strategies and Market Positioning

The sharp downturn in the Bull-Bear Index reflects not only changing macroeconomic expectations but also evolving investor strategies. Hedge funds and asset managers have been rotating into non-U.S. exposures, seeking diversification and tactical opportunities in markets that had previously lagged. Meanwhile, U.S. bond and equity inflows have cooled as global funds rebalance portfolios toward Asia and Europe.

Currency strategists note that such extreme bearish sentiment often precedes periods of stabilization or reversal. When the market becomes too heavily weighted in one direction, even modest positive surprises — such as stronger U.S. economic data or a less dovish Fed outlook — can trigger sharp counter-moves as investors rush to cover short positions.

Broader Context: The Dollar’s Enduring Role

Despite the current bearish turn, the U.S. dollar remains central to the international financial system. It still serves as the primary reserve currency for central banks, the dominant medium for global trade settlements, and the benchmark for commodities pricing. Roughly 88 percent of all foreign exchange transactions involve the dollar, underscoring its enduring influence.

Periods of Weakness in the dollar’s history — from the late 1980s through the early 2000s — have been cyclical rather than structural. Each downturn eventually gave way to recovery, driven by the U.S. economy’s scale, depth, and institutional stability. In this sense, the current decline may reflect the market’s natural rhythm rather than a lasting shift in global financial architecture.

Comparing 2012 and 2026: Lessons From the Past

A comparison between 2012 and 2026 highlights how investor psychology interacts with macroeconomic cycles. In both periods, falling sentiment followed a phase of strong dollar performance and tightening financial conditions. In 2012, ultra-low rates and slow global expansion driven by post-crisis recovery paved the way for renewed risk-taking. The eventual dollar rebound came when U.S. growth accelerated and the Fed began normalizing rates.

Today’s situation may follow a different script but similar logic. If global demand strengthens and U.S. economic fundamentals remain solid, bearish bets could unwind quickly. However, if the Federal Reserve moves aggressively toward easing while other regions maintain stability, investors may continue favoring diversified currency exposure for much of 2026.

Outlook for the Months Ahead

Looking forward, analysts expect volatility in currency markets to remain elevated as traders digest shifting economic data and policy signals. The Federal Reserve’s guidance at upcoming meetings will be pivotal in determining whether the dollar’s decline deepens or finds a floor. A clearer picture of inflation trends, employment strength, and fiscal policy direction will shape the path ahead.

While the current drop in sentiment is steep, the market’s underlying conviction about the dollar’s global importance remains intact. The coming months will test whether this bearish wave marks the beginning of a longer-term transition or merely another oscillation in the currency’s extended cycle of strength and retreat.

As of early 2026, the U.S. dollar stands at a delicate crossroads. The combination of shifting monetary expectations, global diversification, and historical echoes from past downturns underscores the complexity of this moment. Whether the latest bearish readings signal a turning point or a temporary adjustment, one fact remains clear: the evolution of dollar sentiment continues to serve as a vital barometer for the health of the global financial system.