DRAM and NAND Prices Surge: Global Chip Supply Recalibration in Early 2026

The sharp rise in DRAM and NAND spot prices seen in late 2025 through January 2026 marks a critical inflection point for the semiconductor supply chain, with implications spanning consumer electronics, data centers, and manufacturing ecosystems around the world. After a multi-year period of volatility, the newest price movement underscores how memory markets respond to a complex mix of demand resurgence, supply constraints, and investment cycles in memory fabrication capacity.

Historical context: memory markets through the years

- A cyclical industry by design, DRAM and NAND prices have historically moved in waves tied to capex cycles,fab utilization, and end-market demand. In the early 2020s, prices bottomed during technology transitions and oversupply conditions, before a gradual reacceleration as demand recovered from pandemic-era inventory adjustments. The latest run-up continues this pattern, highlighting how macroeconomic recovery, cloud expansion, and consumer device refresh cycles can drive rapid price shifts once supply tightens.

- The memory market’s historical price dynamics are closely linked to fab creation and line utilization. When memory makers expand capacity ahead of demand, prices tend to soften; when production cannot keep pace with demand, prices rise quickly as buyers bid for limited supply. This pattern has repeated across several cycles, shaping investment decisions for equipment suppliers, foundries, and memory manufacturers.

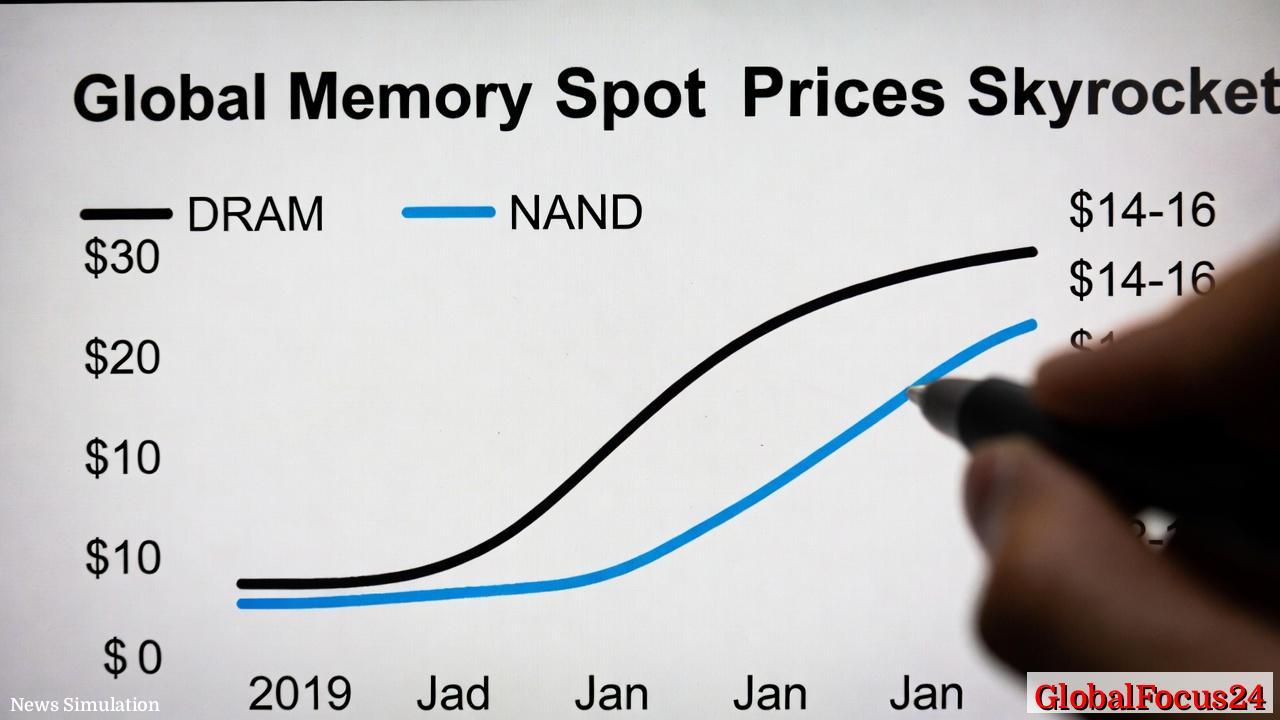

What is driving the current surge

- Demand normalization in data centers and cloud services has accelerated the need for higher-capacity DRAM and NAND in servers, storage arrays, and AI-driven workloads. As hyperscale operators expand memory footprints to support large-scale inference and real-time analytics, demand has outpaced earlier expectations, contributing to price pressure on spot markets.

- Supply-side constraints at memory suppliers, including unique polytechnic and process challenges, have constrained the pace at which new capacity can be brought online. While capacity additions are ongoing, the ramp has not kept pace with the post-pandemic demand rebound, helping to push spot prices higher in late 2025 and early 2026.

- Market psychology and inventory adjustments among buyers—ranging from consumer electronics manufacturers to enterprise IT providers—have also amplified price movements. In periods of rising prices, buyers may accelerate purchases to hedge against further increases, which in turn tightens spot markets further and sustains the upward price trajectory.

Regional and sectoral implications

- Silicon Valley and California’s tech corridor, already a focal point for memory-intensive industries, faces a mixed outlook. Local data centers, AI startups, and hardware developers could experience wider cost considerations for memory components, influencing capex planning and product pricing for AI accelerators, servers, and storage products. The region’s high concentration of high-tech manufacturing and R&D intensifies exposure to memory price swings, underscoring the need for strategic supplier partnerships and diversified sourcing.

- Asia remains a central hub for memory production and distribution, with price dynamics echoing regional supply chain realignments. Taiwan, Korea, and China-based fabs contribute significantly to DRAM and NAND output, making regional market conditions particularly influential on global prices. Fluctuations in this regional balance can ripple through global supply chains, affecting not only device manufacturers but also downstream equipment makers and service providers.

- Europe and the Americas are increasingly sensitive to memory costs in enterprise IT and telecommunications infrastructure. As 5G, edge computing, and data-center modernization continue, European and North American customers may experience tighter supply and higher total cost of ownership for memory-intensive deployments, reinforcing the importance of long-term supplier relationships and strategic stock planning.

Economic impact across devices and industries

- Consumer electronics: Smartphones, laptops, and EVs with advanced infotainment systems increasingly rely on high-density memory. Higher DRAM and NAND costs can propagate into device pricing, potentially slowing refresh cycles or prompting more aggressive feature trade-offs in price-sensitive segments. Device manufacturers may respond by optimizing software and memory usage to mitigate cost pressures while preserving performance.

- Data centers and cloud services: Memory is a core driver of data center performance and energy efficiency. Rising memory prices raise capital expenditure and operating costs for hyperscale operators, potentially slowing expansion plans or prompting a shift toward memory-efficient architectures and increased memory tiering strategies. As memory becomes a larger portion of total compute cost, procurement strategies emphasizing long-term supplier commitments and multi-sourcing become more common.

- Enterprise storage and AI workloads: Price volatility in DRAM and NAND affects SSD pricing, storage density, and AI model training infrastructure. Systems integrators and enterprise buyers may prioritize solutions that balance performance with total cost of ownership, including memory recycling, memory compression techniques, and platform-level optimizations to maximize usable capacity within budget constraints.

Historical context and how today compares

- The current price trajectory resembles prior memory cycles, where a rebound in demand coincided with restrained supply, leading to rapid price increases after a period of underutilization. Analysts often monitor line utilization rates, fab ramp timing, and capex cycles to gauge how long elevated prices may persist. The latest surge aligns with a broader pattern of post-peak demand realignment and capacity buildouts in the memory sector.

- Unlike some earlier episodes, the integration of AI workloads and edge computing has reinforced memory inelasticity in certain segments, intensifying price sensitivity for high-performance memory applications. This dynamic may prolong elevated price levels relative to consumer-focused memory applications, where demand elasticity tends to be higher.

Comparisons with adjacent tech components

- NAND versus DRAM: While both memory types have tracked upward in late 2025 and into 2026, NAND market movements are often more sensitive to capacity additions in flash memory ecosystems and enterprise SSD demand. DRAM prices can respond more quickly to memory bandwidth requirements in servers and client devices, leading to nuanced price trajectories across the two segments. The concurrent rise in both indicates synchronized demand pressures across primary memory categories.

- Semiconductors more broadly: The memory segment, while subject to its own supply-demand dynamics, also interacts with broader chip cycles, including logic and foundry capacity. A tightening memory market can influence overall chip pricing and inventory strategies for device makers, especially when coupled with supply constraints in other critical components such as GPUs and CPUs. This interconnectedness underscores the importance of diversified supplier relationships and strategic inventory planning within the tech ecosystem.

Policy and strategic considerations for buyers

- Long-term procurement and inventory management: Organisations may increasingly adopt longer-term memory supply agreements, advance purchase commitments, and secure contractual pricing to hedge against continued volatility. These strategies can stabilize budgets and ensure access to essential memory components during demand surges.

- Risk management and supplier diversification: Given regional supply concentration, buyers are likely to diversify suppliers across multiple geographies to reduce single-source risk. This approach helps mitigate potential disruptions from geopolitical tensions, natural disasters, or localized outages impacting memory production and distribution networks.

- Innovation and architectural resilience: Enterprises may invest in architectural strategies that reduce memory dependency, such as memory-compression techniques, improved data locality, and software optimizations that lower bandwidth and energy consumption. These investments can offset some memory cost pressures while preserving performance growth in AI and data-intensive workloads.

Public reaction and market sentiment

- Industry analysts, investors, and technology executives are closely watching memory price indices as bellwethers for capex cycles and product roadmap decisions. The heightened attention reflects memory’s central role in data-driven applications, from cloud data centers to consumer devices, and the broader implications for competitiveness in tech-intensive markets.

- In regional tech hubs, startup ecosystems and hardware accelerators are expressing cautious optimism about steady demand for memory-intensive platforms, paired with a pragmatic focus on supply chain resilience and cost control. This sentiment often translates into strategic partnerships and collaboration across suppliers, service providers, and research institutions to navigate ongoing market volatility.

Conclusion The early-2026 surge in DRAM and NAND spot prices marks a pivotal moment for the global memory market, reflecting a confluence of rebounding demand, constrained supply, and strategic shifts across industries. As memory remains a critical bottleneck for data centers, AI workloads, and consumer electronics, buyers and manufacturers alike will likely prioritize diversification, long-term planning, and architectural efficiency to navigate a pricing environment that has grown more dynamic and interconnected than in recent years. The memory cycle is once again reshaping investment decisions, pricing strategies, and product design across the technology spectrum, signaling a period of careful navigation rather than rapid acceleration.