Venture Capital Funding in Crypto and Blockchain Surges to $8.5 Billion in Q4 2025, Marking Strongest Quarter Since 2022

Historic Rebound Signals Renewed Confidence in Digital Assets Sector

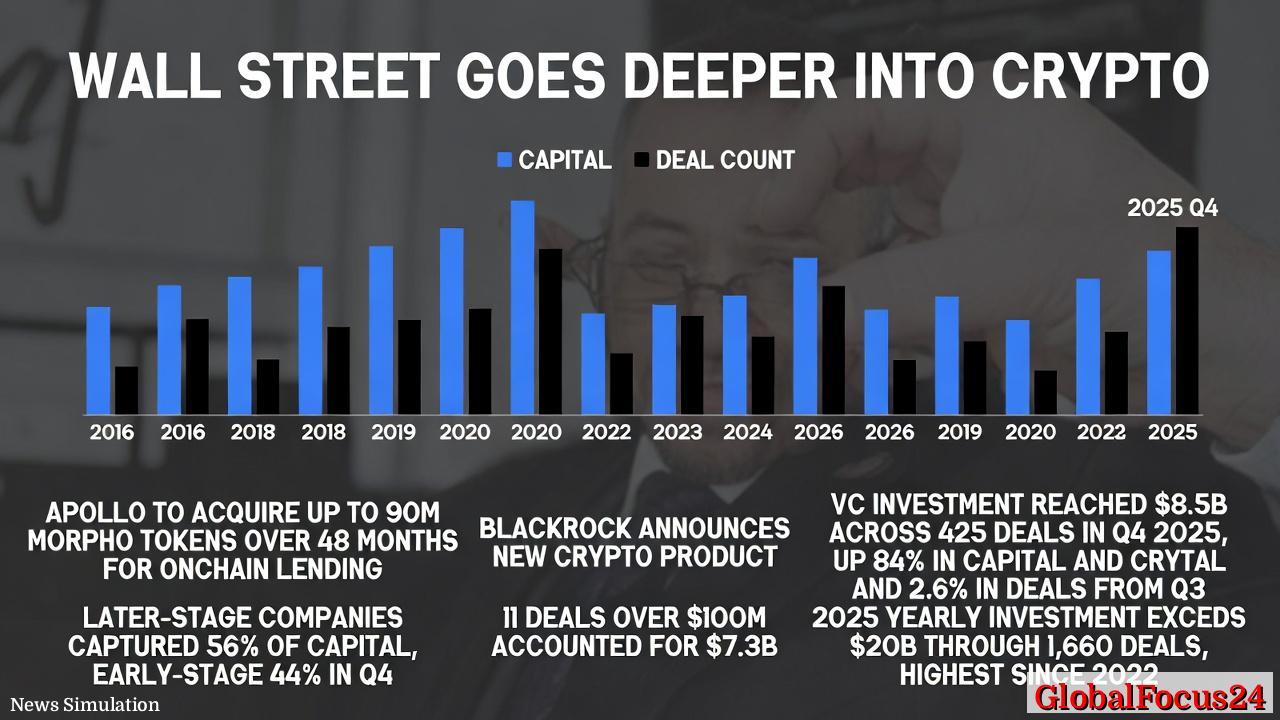

Venture capital investment in cryptocurrency and blockchain startups soared to approximately $8.5 billion across 425 deals in the fourth quarter of 2025, according to newly compiled industry data. The surge represents an 84% increase in capital deployed compared with the previous quarter, accompanied by a modest 2.6% rise in deal volume. This resurgence marks the largest quarterly total since mid-2022, signaling a potential turning point for the digital assets industry after two years of subdued activity.

The renewed pace of investment underscores a shift in investor sentiment, driven by technological maturity, improved market stability, and the growing institutional acceptance of blockchain applications beyond speculative trading. It follows a cautious period in 2023 when venture funding across the crypto sector reached multi-year lows amid global macroeconomic tightening and regulatory uncertainty.

Late-Stage Deals Capture Majority of Capital

Later-stage companies dominated the deal landscape in Q4 2025, capturing 56% of total capital raised, as investors sought established ventures with proven business models and traction in areas such as blockchain infrastructure, custody solutions, and enterprise integrations. Early-stage startups, including seed and Series A rounds, accounted for 44% of the quarter’s investment, reflecting ongoing interest in innovation at the frontier of decentralized finance, digital identity, and tokenized real-world assets.

A handful of large transactions defined the quarter’s momentum. Eleven late-stage deals, each surpassing $100 million in funding, collectively accounted for approximately $7.3 billion, or 85% of total quarterly investment. These “mega-rounds” included financing for blockchain infrastructure platforms, layer-two scaling technologies, and Web3 gaming ecosystems, highlighting investors’ focus on scalability and utility-driven adoption.

2025 Closes as Strongest Year for Crypto VC Since 2022

For the full year 2025, venture capitalists committed over $20 billion across approximately 1,660 deals—the largest annual total since 2022 and more than double the total recorded in 2023. The rebound follows a tough 2023 marked by liquidity contractions, rising interest rates, and fallout from regulatory actions against major digital asset platforms.

By comparison, 2022 had previously set the record with an unprecedented influx of venture capital exceeding $30 billion into blockchain startups. That wave was followed by a significant downturn in 2023 as crypto markets reeled from bankruptcies, compliance crackdowns, and investor retrenchment. The resurgence in 2025 suggests a broader recovery cycle gaining traction, with the investor community pivoting from speculative projects toward infrastructure, compliance technology, and interoperability solutions.

Institutional Momentum and Regulatory Clarity Drive Renewed Activity

Institutional participation has been a defining feature of this latest wave of investment. Several major asset managers, fintech firms, and sovereign funds expanded their exposure to blockchain startups during the second half of 2025. Their focus largely centered on tokenization of real-world assets, digital payments infrastructure, and decentralized data verification systems aimed at improving efficiency across finance, logistics, and energy sectors.

Regulatory clarity also played a crucial role in restoring investor confidence. North America, Europe, and select jurisdictions in Asia implemented or advanced comprehensive digital asset frameworks in late 2025, providing more predictable compliance pathways for both startups and investors. Jurisdictions such as the European Union—through the Markets in Crypto-Assets (MiCA) framework—and the United Kingdom’s emerging tokenization guidelines have made it easier for capital allocators to assess risk.

In the United States, while federal regulation remained fragmented, state-level initiatives and pilot programs around blockchain-enabled payments and smart contract validation added to a sense of optimism among venture backers seeking long-term stability.

Global and Regional Investment Patterns

Geographically, North America remained the leading hub for crypto venture financing in Q4 2025, accounting for nearly half of all capital raised. Silicon Valley and New York continued to dominate in late-stage deal flow, driven by maturing startups focused on institutional-grade crypto infrastructure and AI-powered transaction analytics.

Europe captured approximately 30% of global crypto VC funding, buoyed by strong interest in regulatory-compliant projects and payments platforms aligned with MiCA standards. Notable hotspots included London, Berlin, and Zurich—each benefitting from access to both fintech talent and forward-leaning regulatory regimes.

Asia-Pacific saw a steady but measured recovery, led by Singapore, Hong Kong, and South Korea. These markets drew investors to blockchain gaming, decentralized social applications, and cross-border payment solutions. Meanwhile, venture interest in emerging regions such as Latin America and Africa expanded modestly, reflecting growing adoption of blockchain for remittances and supply chain tracking.

Comparing to Broader Venture Market Trends

The cryptocurrency sector’s rebound stands out against a more uneven backdrop in the broader venture capital landscape. While global VC investment in technology remained below 2021 levels, crypto and blockchain startups gained relative momentum thanks to sector-specific catalysts—including Bitcoin’s price stabilization and the resurgence of decentralized finance protocols.

In contrast, sectors such as cloud software, mobility, and consumer applications saw flat or declining deal activity as investors prioritized profitability over growth. The re-entry of corporate venture arms from financial institutions and technology conglomerates into blockchain funding marked another key shift, suggesting long-term strategic interest in distributed ledger applications.

Thematic Investment Trends: Beyond Speculation

The focus of crypto venture investment in 2025 diverged significantly from the speculative narratives of earlier cycles. Investors increasingly prioritized “picks and shovels” opportunities—foundational infrastructure that supports scalability, interoperability, and regulatory compliance. Top themes included:

- Layer-2 and modular blockchain architecture enabling faster and cheaper transactions.

- Tokenization of real-world assets (RWAs) such as bonds, real estate, and commodities, which gained traction among institutional investors.

- DeFi protocols integrating compliance features, bridging traditional finance and decentralized ecosystems.

- Blockchain-driven data provenance and identity verification tools supporting enterprise use cases.

- Web3 gaming and entertainment ecosystems, emphasizing player ownership and digital asset portability.

This shift toward practical and enterprise-oriented applications reflects a maturing market aligning innovation with sustainable business fundamentals. Venture partners cited measurable revenue growth, rather than speculative token valuation, as the primary driver for late-stage allocations.

Lessons from the Previous Cycle

The last major crypto VC surge in 2021–2022 was marked by an explosion of projects built around non-fungible tokens (NFTs), decentralized exchanges, and experimental governance tokens. Many of these ventures struggled to retain users or revenue when market liquidity faded in subsequent years. As a result, investors in 2025 adopted more cautious diligence standards and emphasized transparent tokenomics, audited smart contracts, and compliance readiness.

The lessons of the 2022 crash led to increased professionalism across the crypto startup ecosystem. Founders emerging in this cycle often have backgrounds in traditional finance, enterprise software, or regulatory technology, enhancing investor confidence. Accelerators and incubators have likewise shifted focus from speculative assets toward business models capable of integrating with mainstream financial infrastructure.

Economic Implications and Outlook for 2026

The renewed flow of capital into crypto ventures carries broader economic implications. Blockchain investment increasingly intersects with traditional sectors, allowing for more efficient capital markets, supply chain resilience, and data integrity solutions. Analysts suggest that the sector’s rebound could lift related industries—including cybersecurity, cloud computing, and digital asset custody—creating a multiplier effect across the tech economy.

For 2026, experts forecast continued momentum in institutional blockchain adoption but expect a slower pace of funding growth as markets consolidate. With venture investors maintaining disciplined valuations and closer oversight, the next phase is likely to favor commercially proven businesses. Strategic mergers, token equity hybrids, and differentiated infrastructure bets could define the competitive landscape.

The interplay between macroeconomic stability, regulatory evolution, and technological breakthroughs will remain central to sustaining growth. If digital asset adoption progresses alongside clearer legal frameworks and increasing enterprise utility, the crypto venture market could establish a more enduring foundation than in prior speculative cycles.

A Defining Quarter for the Digital Asset Industry

The fourth quarter of 2025 stands as a landmark period of rejuvenation for the crypto and blockchain ecosystem. Following two years of retrenchment and recalibration, the surge to $8.5 billion in venture funding underscores renewed conviction in the transformative potential of distributed technologies. While risks remain—from regulatory adjustments to liquidity constraints—the trajectory of late 2025 suggests a sector once again stepping into the mainstream of technological innovation and financial investment.