Global Crypto Funds Face Sharp $1.7 Billion Weekly Outflow Amid Investor Pullback

Digital Asset Markets Reverse Course After Strong 2025

Digital asset investment products saw one of their steepest weekly declines in months, with net outflows totaling $1.7 billion in the week ending early February 2026, according to new data from market trackers. The figure represents a marked reversal from the strong inflows of late 2025, shifting the year-to-date flows into negative territory and dragging down total assets under management (AUM) across major cryptocurrency funds.

The downturn reflects renewed investor caution as global markets adjust to tighter liquidity, fluctuating sentiment, and a shifting macroeconomic environment. After hitting record highs in October 2025, the crypto asset management industry now faces a retrenchment that underscores the persistent volatility and sensitivity of the sector to risk appetite and regulatory shifts.

United States Leads Capital Withdrawals

The majority of last week’s outflows originated in the United States, which has long dominated digital asset fund activity. Analysts report that American institutional investors, who had driven much of the late 2025 recovery, are now scaling back exposure, citing the continued lack of clarity in digital asset regulation, as well as uncertainty around central bank policy.

While Europe and Asia also registered modest redemptions, the U.S. accounted for the bulk of the $1.7 billion in withdrawals. This concentration reflects the region’s higher participation in spot bitcoin exchange-traded products (ETPs) and futures-linked funds, which saw the steepest declines.

Bitcoin and Ethereum Lead Redemptions

The largest outflows were concentrated in Bitcoin and Ethereum funds, historically the cornerstones of digital asset portfolios. Bitcoin products alone saw several hundred million dollars in redemptions, signaling waning enthusiasm after a strong rally that began in mid-2025. Ethereum followed a similar pattern, reflecting broader weakness in the large-cap segment of the crypto market.

Other major altcoins, including Solana and Cardano, experienced smaller but still notable corrections. Market analysts describe the moves as “defensive profit-taking” rather than panic selling, with investors looking to lock in gains accumulated over the previous quarter.

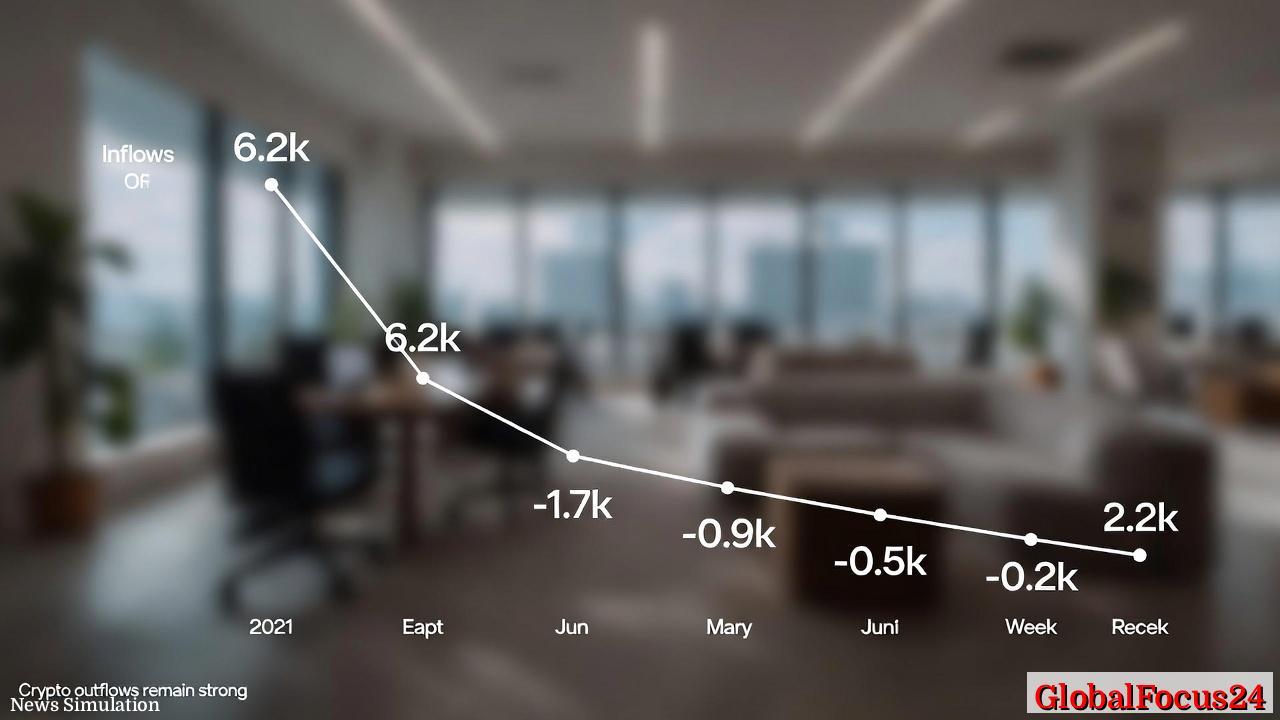

The pattern of flows in recent months tells a story of mounting investor indecision. As the weekly data show, strong inflows reaching as high as $6.2 billion during peak periods in earlier cycles have given way to a streak of negative values, including -0.9 billion, -0.5 billion, and -1.7 billion dollars in recent weeks. A brief surge to positive 2.2 billion late last month proved short-lived before returning to small outflows of around -0.2 billion, suggesting instability in momentum and confidence.

A Broader Context of Volatility

Cryptocurrency markets entered 2026 after one of the most turbulent years in recent memory. Following a robust recovery in the second half of 2025—when Bitcoin prices reclaimed levels above $60,000 and investor optimism surged—headwinds began to mount. Rising interest rates across major economies, slower institutional adoption, and concerns over regulation collectively dampened enthusiasm.

Historically, digital assets have shown cyclical patterns tied closely to macro-financial conditions. During the 2020–2021 bull cycle, for example, digital asset funds recorded consistent inflows driven by record-low global interest rates and stimulus spending. In contrast, periods of quantitative tightening, such as those seen in 2022 and again starting in late 2025, have tended to correspond with significant drawdowns.

Economic Impact Across the Sector

The latest data carry significant implications for both retail investors and institutional asset managers. The fall in managed assets not only reduces fee revenue for fund providers but also dampens liquidity in secondary markets for digital asset products. This, in turn, can contribute to wider bid-ask spreads and diminished market depth—conditions that historically exacerbate volatility.

Some analysts note that the decline in AUM could prompt fund consolidations or operational restructuring in smaller firms that depend heavily on management fees. Large-scale providers with diversified exposure, however, are better equipped to absorb short-term fluctuations.

Moreover, the shift in flows may influence regional capital markets. In countries where crypto-linked funds have become a notable component of alternative investment portfolios—such as the U.S., Canada, and parts of Western Europe—the reversal could marginally reduce overall cross-asset liquidity. Still, the impact on traditional equity or bond markets remains limited, underscoring the relatively small footprint of digital assets in global finance.

Comparing Global Trends

The regional divergence in recent weeks mirrors broader differences in regulation and investor sentiment.

- United States: Outflows here were amplified by ongoing uncertainty around tax treatment and upcoming Securities and Exchange Commission decisions on new crypto fund applications.

- Europe: Activity in Europe was steadier, although sentiment weakened due to recent amendments to the EU’s Markets in Crypto-Assets (MiCA) framework, which introduced new compliance costs for issuers.

- Asia-Pacific: Japan and South Korea continued to see net inflows into domestic exchange-traded vehicles, supported by clearer regulatory regimes. Meanwhile, Hong Kong-based funds experienced slight outflows following profit-taking in Chinese-linked crypto assets.

These variations highlight how policy stability and operational transparency remain key determinants of investor engagement in digital assets.

Institutional Behavior and Investor Psychology

The scale and speed of this outflow also underscore the role of investor psychology in the cryptocurrency market. Unlike traditional asset classes, where institutional flows are often gradual, crypto fund positions can shift abruptly with changes in sentiment ors. Analysts describe this dynamic as a “behavioral amplification effect,” where both inflows and outflows tend to overshoot underlying value movement.

Institutional investors, who now represent a significant share of total crypto fund volume, often rely on algorithmic signals or momentum models that can exacerbate volatility. This mechanized repositioning explains why the $1.7 billion outflow, though large, aligns with prior episodes of correction in earlier cycles such as mid-2022 and early 2023.

Resilience and Long-Term Outlook

Despite the current downturn, digital assets remain embedded within global financial infrastructure more deeply than ever before. Long-term managers continue to view Bitcoin as a potential inflation hedge and Ethereum as the technological backbone of decentralized finance. Recent industry reports suggest that venture capital funding into blockchain startups, while below 2021 peaks, remains significant—another indicator that structural interest in the sector endures even in risk-off periods.

Market historians draw parallels between the present correction and earlier shakeouts that preceded renewed growth. For example, after the late-2018 crypto winter, digital asset funds rebounded sharply as institutional frameworks matured. If macroeconomic conditions stabilize later in 2026—particularly if inflation moderation allows for interest rate cuts—analysts expect inflows to return, though possibly with greater emphasis on regulated and exchange-listed instruments.

What Comes Next

Short-term momentum remains fragile. Traders are watching whether the next few reporting cycles will confirm a stabilization in flows or extend the current trend of redemptions. Total assets under management have already fallen significantly from the highs of late 2025, illustrating just how quickly sentiment can shift in digital markets.

Still, volatility is a defining feature rather than an anomaly of the digital asset sector. While the $1.7 billion weekly outflow marks a setback, it also fits within the cyclical rhythm that has characterized the industry since its inception. Each contraction phase has historically been followed by renewed innovation, tighter risk controls, and ultimately broader adoption.

As February progresses, the focus will turn to whether institutional confidence can recover in time to prevent further erosion in managed capital. For now, the data paint a picture of an industry in recalibration—one that continues to test the boundaries of both financial technology and investor endurance.