Title: White-Collar Jobs in the S&P 500 Fall for First Time Since 2016 as AI Push Reshapes Corporate Staffing

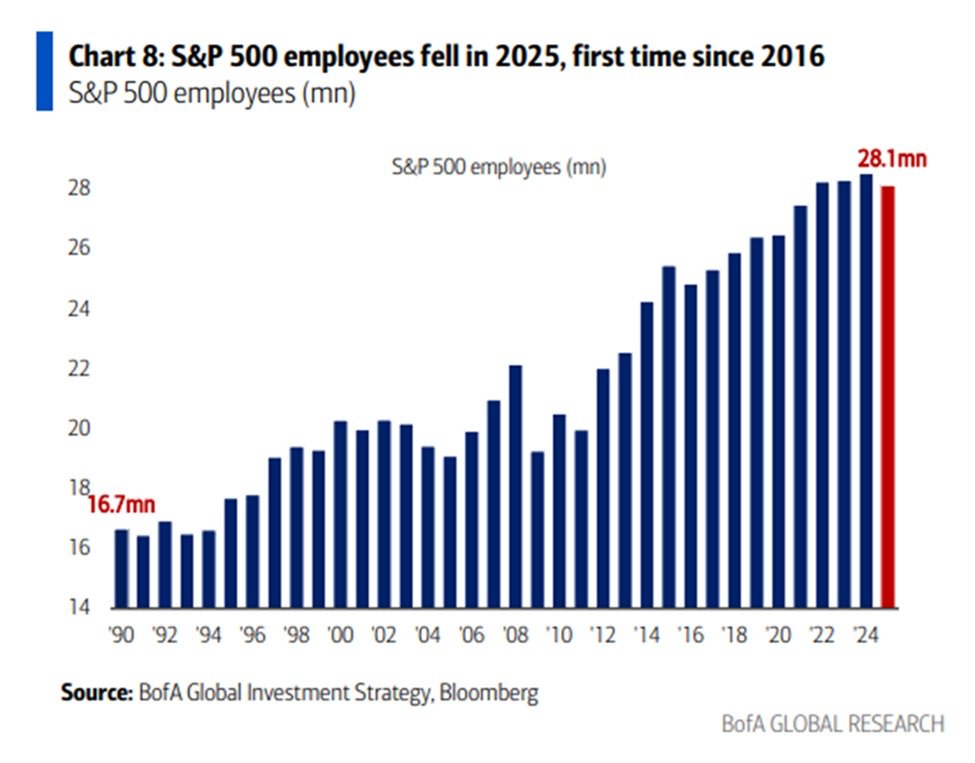

A broad shift in corporate strategy across the S&P 500 has produced a rare contraction in white-collar employment, signaling a turning point in the labor market and corporate balance sheets. In 2025, the number of white-collar workers employed by S&P 500 companies declined by about 400,000, bringing the total to 28.1 million. This marks the first annual drop in this segment in nearly a decade, ending a sustained period of growth that added more than 3 million white-collar jobs over eight consecutive years. The change underscores how cost discipline, efficiency drives, and the rapid deployment of artificial intelligence are reshaping the composition of the modern corporate workforce.

Historical context: a century-long trend toward tech-enabled productivity To understand the significance of the 2025 decline, it helps to place it in a longer arc. Since the late 20th century, white-collar employment in large U.S. corporations has been highly sensitive to productivity gains, capital investment cycles, and the pace of technology adoption. The late 1990s and early 2000s brought thousands of back-office jobs offshore or automated, followed by a rebound during the tech boom of the 2010s. The 2016 to 2024 period was characterized by steady hiring across many sectors—finance, software, manufacturing, and professional services—as firms expanded teams to support growth in cloud computing, data analytics, and global supply chain management.

What changed in 2025 was not solely a reaction to a single event, but a convergence of strategic priorities. The most notable driver has been the accelerated integration of artificial intelligence and automation into core business processes. Advanced AI tools promise to streamline decision-making, enhance customer service, and optimize operations—from procurement and compliance to finance and human resources. As companies test and scale these capabilities, they often reallocate resources away from routine, non-core tasks toward higher-value activities, while also creating a path for restructuring entrenched processes. The result is a leaner, more automated wage bill that maintains competitiveness in a challenging macroeconomic environment.

Industry players at the center of the shift Several leading corporations figured prominently in the 2025s about white-collar reductions:

- Amazon announced plans to eliminate roughly 16,000 corporate positions as part of an ongoing effort to recalibrate the mix of roles supporting e-commerce, logistics, and cloud computing platforms. The move aligns with a broader strategy to temper operating expenses while investing aggressively in AI-enabled services and automation across fulfillment networks and back-office operations.

- Meta Platforms initiated a workforce reduction of about 8,000 roles, reflecting a broader reexamination of organizational structure as the company pivots toward short-form video monetization, artificial intelligence-driven products, and the monetization of the metaverse ecosystem.

- Microsoft signaled significant voluntary buyouts affecting approximately 8,750 employees, signaling a disciplined approach to headcount management in areas where automation and AI tools can substitute or augment human labor, while preserving critical software development and enterprise services capabilities.

- Other tech and consumer platforms, including Oracle, Intel, and UPS, joined the broader trend of aligning headcount with strategic priorities, emphasizing efficiency improvements and AI-enhanced operations.

Economic impact: the ripple effects beyond balance sheets The 2025 decline in white-collar employment carries implications that extend beyond corporate payrolls. Analysts highlight several key channels through which the hiring slowdown and layoffs may influence the broader economy:

- Consumer spending: layoffs and wage adjustments affect household purchasing power, particularly in metropolitan regions with high concentrations of S&P 500 headquarters and corporate campuses. Slower job growth in white-collar sectors can cushion wage inflation expectations but may damp consumer demand in metropolitan service sectors.

- Investment and risk sentiment: the shift toward automation and AI-driven processes can influence capital expenditure patterns. Companies may accelerate investments in AI software, cloud infrastructure, and cybersecurity to support new workflows, potentially boosting growth in the tech sector even as headcount declines in administrative layers.

- Real estate and urban dynamics: changes in corporate staffing can affect demand for office space, commercial real estate rents, and urban infrastructure. Regions with a high density of corporate offices could see a recalibration of demand for urban amenities, transit, and ancillary services.

- Productivity and supply chains: AI-infused workflows can raise productivity, potentially offsetting some wage pressures and supporting margins. This productivity gain may translate into more competitive pricing and healthier corporate earnings over time, even as employment levels in traditional administrative roles decline.

Regional comparisons: pockets of resilience and exposure Different regions in the United States experience the 2025 headcount shift in distinct ways, shaped by industry mix and the concentration of corporate headquarters:

- West Coast hubs: California and Washington remain centers for technology, software, and cloud services. While some white-collar roles shrink, these regions often see continued demand for high-skill AI development, product management, and data science roles, partially offsetting losses in administrative and middle-management layers.

- Northeast financial corridors: Metropolitan areas with dense financial services ecosystems may experience upside from AI-enabled risk analytics, regulatory technology, and compliance operations. The shift toward automation can support more complex, high-value functions that require specialized expertise, sustaining demand for senior-level professionals.

- Southeast growth markets: Regions with a mix of manufacturing, logistics, and technology services may witness a more gradual impact. AI adoption in operations, supply chain optimization, and customer service automation can drive efficiency gains without triggering as large a withdrawal from traditional white-collar roles.

- Mountain and central regions: States with diversified economies and strong manufacturing bases could experience mixed effects. The rebound or decline in jobs depends on the pace of AI deployment, investment in skilled labor, and the ability of local workers to retrain for higher-value roles.

Corporate strategies in a changing labor landscape What explains the 2025 turnover beyond thenumbers? Many companies are pursuing a multi-pronged strategy that blends cost discipline with investment in AI-driven capabilities:

- Workforce optimization: firms are scrutinizing non-core roles and administrative functions. The goal is to streamline operations, reduce duplication, and improve cross-functional collaboration through technology-enabled workflows.

- Re-skilling and upskilling: as automation deploys in more processes, companies invest in training programs to help employees transition into data analytics, machine learning, AI ethics, and advanced software engineering roles. This shift aims to preserve institutional knowledge while unlocking higher-value work.

- Strategic outsourcing and consolidation: some tasks migrate to specialized service providers or centralized platforms, enabling in-house teams to focus on core capabilities and product development. This trend can influence job geography, with more roles shifting to regions with competitive talent pools.

- AI governance and risk management: the adoption of AI tools comes with oversight requirements. Companies are strengthening governance structures, ethics guidelines, and compliance frameworks, which often creates demand for roles in risk analysis, regulatory technology, and internal controls.

Public reaction and market signals Public sentiment around corporate layoffs is nuanced. On one hand, investors often interpret headcount reductions as a signal of disciplined management and a clear path to improving margins. On the other hand, lingering concerns about job security and wage growth can influence consumer confidence and spending patterns. The broader market response to these shifts is shaped by the quality of the AI deployments, the transparency of the cost-cutting measures, and the speed at which new product capabilities translate into revenue growth.

Industry economists emphasize that the 2025 decline does not necessarily imply a secular drop in productivity or a long-term trend away from employment in professional sectors. Rather, it reflects a structural reallocation of human capital—prioritizing roles that complement AI systems, and shifting routine, repetitive, or lower-value tasks toward automation or outsourcing. Over time, this can yield a more resilient corporate economy, provided workers are offered credible pathways to transition into higher-skill roles.

Technological acceleration: AI at the core of corporate evolution The role of artificial intelligence in this reshaping cannot be overstated. AI tools now assist with complex data analysis, forecasting, and decision support across finance, operations, and customer relations. In areas such as procurement, compliance, and human resources, AI accelerates cycle times and reduces human error, enabling teams to tackle more strategic initiatives. This acceleration fosters a cycle where AI enables better human productivity, which in turn drives renewed investment in platform-scale solutions and skilled labor that can design, supervise, and optimize these systems.

Societal and regional policy implications policymaking and workforce development play a crucial role in how communities adapt to these changes. Local governments and educational institutions can support transitions through reskilling programs, apprenticeships, and partnerships with industry to align curricula with in-demand skills. Moreover, regional economic plans that emphasize digital infrastructure, data centers, and cybersecurity can help attract firms pursuing AI-driven efficiency while creating opportunities for workers to move into higher-value roles.

Outlook for 2026 and beyond While 2025 marked a decline in white-collar employment within the S&P 500, analysts expect a nuanced path forward. Several factors will shape the trajectory:

- AI maturity: as AI tools mature and are embedded more deeply into core business processes, productivity gains are likely to accelerate. This can support higher profits and, potentially, selective hiring in specialized areas such as data science, AI ethics, and product innovation.

- Macro conditions: interest rates, inflation, and consumer spending dynamics will influence corporate investment decisions. A stable or improving macro backdrop could encourage cautious hiring in strategic areas while maintaining efficiency gains from automation.

- Sector-specific differences: software, semiconductors, e-commerce logistics, and professional services may experience divergent hiring patterns. Companies with a strong AI-enabled product roadmap and scalable platforms could see more targeted growth in specialized roles even as broader administrative positions shrink.

Conclusion: a nuanced turning point in corporate employment The 2025 decline in white-collar employment across the S&P 500 underscores a period of significant recalibration in corporate staffing. It reflects not just cost-cutting but a strategic pivot toward AI-enabled efficiency and higher-value work. The shift challenges workers and communities to adapt, offering opportunities for retraining and progression into roles that leverage data-driven decision-making, automated workflows, and technology-enabled service delivery.

As firms continue to balance the benefits of automation with the need to maintain innovation and customer focus, the labor market will likely enter a phase of selective growth, with hiring concentrated in areas that require advanced technical expertise, strategic thinking, and complex problem solving. For regions and industries that invest in workforce development and digital infrastructure, the transition may yield a more resilient economic fabric capable of sustaining competitiveness in a rapidly changing global market.