AI Infrastructure Stocks Lead Market Gains Amid Structural Shifts in Tech Spending

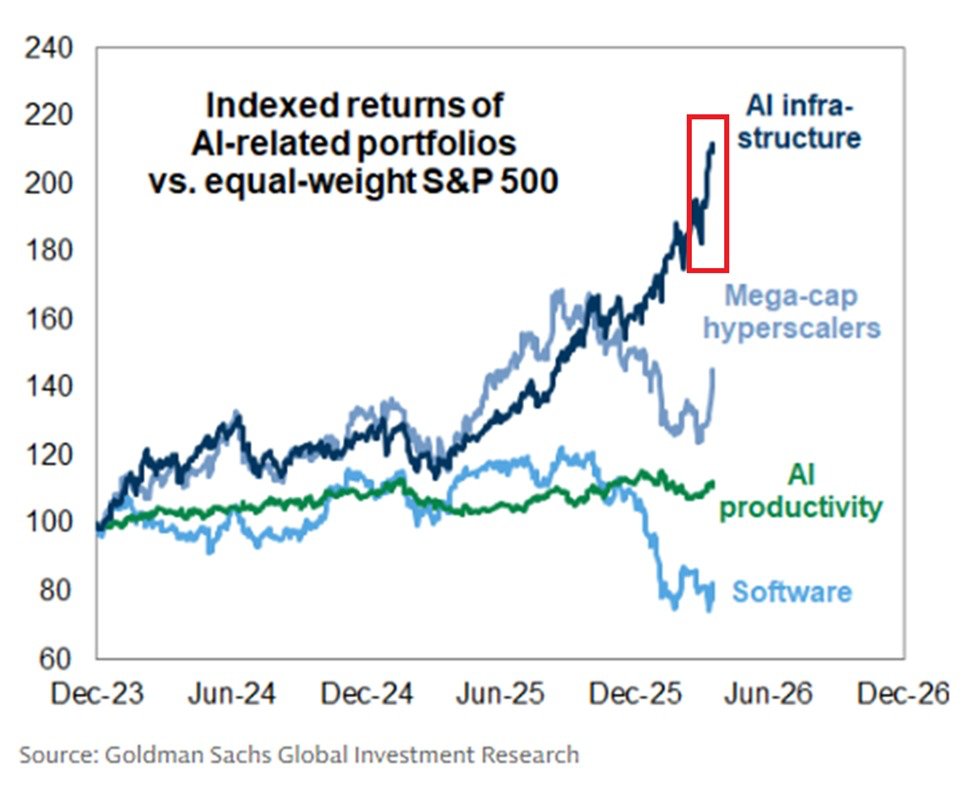

AI infrastructure stocks have outperformed the broader market since December 2023, underscoring a structural shift in how firms invest in technology to power next-generation intelligence. Weighing in across semiconductors, data center operators, cloud providers, networking equipment firms, and power utilities, this cohort has surged roughly 115% relative to the equal-weighted S&P 500 over the period. By contrast, mega-cap hyperscalers — including Microsoft, Alphabet, Amazon, and Meta — have delivered a solid but more modest outperformance of about 45% in the same window. AI productivity stocks, which emphasize companies aimed at reducing costs and boosting efficiency through artificial intelligence, have posted a 10% gain, while software equities have lagged by about 20%. These dynamics illuminate how investors perceive the backbone of AI adoption and where the benefits of scale, bandwidth, and energy efficiency accrue.

Historical context: the dawn of scalable AI infrastructure

The current cycle traces back to foundational investments in compute, memory, and networking that began accelerating in the early 2020s. As organizations sought to train larger models and deploy AI services at scale, demand for specialized chips, high-performance data centers, and robust cloud ecosystems intensified. The result was a bifurcation in the tech landscape: companies that build and operate the physical and cloud layers needed to support AI workloads, and those that deliver end-user AI-powered applications. The former group has benefited from higher capital expenditure cycles and longer-duration investments, while the latter has enjoyed expanding TAM (total addressable market) driven by AI-enabled features and new business models.

Economic impact: capital allocation, margins, and regional spillovers

- Capital expenditure cycle: The AI infrastructure cohort has benefited from sustained capex in semiconductors, data center buildouts, and networking upgrades. These investments support higher utilization of AI accelerators, faster interconnects, and more energy-efficient operations, contributing to improved total cost of ownership for AI deployments.

- Margins and pricing power: Firms embedded in the AI backbone have, in many cases, capitalized on favorable supply-demand dynamics for premier chips, edge devices, and hyperscale cloud capacity. While chipmakers and data center operators face cyclicality, the trajectory toward larger-scale deployments has supported disciplined pricing and efficiency gains.

- Regional spillovers: The United States and other major tech hubs have seen job creation, supplier diversification, and knowledge spillovers as AI infrastructure spending accelerates. Regions with dense ecosystems of chip fabrication, cloud services, and network hardware manufacturing tend to exhibit faster productivity growth, higher investment inflows, and more resilient supply chains.

- Energy considerations: As AI workloads scale, power consumption remains a salient concern. Advances in chip efficiency, cooling technologies, and power management contribute to the long-term sustainability of AI infrastructure investments. Power utilities serving data center campuses and colocation facilities are increasingly linked to growth in AI-capable infrastructure, highlighting the intertwined nature of technology and energy markets.

Regional comparisons: North America, Europe, and Asia-Pacific

- North America: The largest concentration of AI infrastructure activity remains in North America, where leading cloud providers, hyperscalers, and semiconductor manufacturers sustain a robust investment cycle. The region benefits from mature capital markets, favorable regulatory environments, and deep talent pools, reinforcing its central role in AI deployment.

- Europe: European markets have emphasized data sovereignty, cybersecurity, and energy efficiency. AI infrastructure investments in Europe are increasingly tied to green data centers and modular compute, aligning with broader sustainability goals and digital sovereignty initiatives. While growth may be slower than North America’s, steady progress reflects a mature, risk-managed approach.

- Asia-Pacific: APAC, led by China, Japan, South Korea, and Singapore, represents a rapidly expanding frontier for AI infrastructure. Investments in hyperscale campuses, advanced manufacturing of semiconductors, and 5G-enabled networking hardware support a high-growth trajectory, even as geopolitical and regulatory dynamics influence project pacing.

Industry dynamics: what sets AI infrastructure apart from software and pure AI productivity plays

- Underlying assets: AI infrastructure stocks center on tangible assets — servers, accelerators, network fabrics, and cold energy systems. These assets require ongoing maintenance, capacity upgrades, and risk management but offer tangible durability and collateral value.

- Revenue visibility: Cloud providers and data center operators often enjoy recurring revenue streams, long-term contracts, and scale efficiencies that can translate into resilient cash flows, even amid macro headwinds.

- Innovation cycle: The AI backbone benefits from ongoing breakthroughs in chip architectures (such as specialized AI accelerators), memory technologies, and interconnectivity. This acceleration cycle sustains demand for newer equipment and upgrades, supporting longer investment horizons for infrastructure players.

- Compared to software and AI productivity: Software names can experience higher gross margins but may face greater risk from competition and customer consolidation. AI productivity companies are exposed to corporate budgeting cycles and user adoption rates, which can be more volatile. In contrast, the AI infrastructure cohort rides the trend of rising AI adoption at the enterprise level, anchored by hardware and cloud-scale services.

Market drivers: demand catalysts shaping the trajectory

- AI model scale and training: The race to train larger and more capable models continues to require powerful compute and optimized data pipelines. This drives demand for high-performance GPUs, CPUs, and tensor processing units, as well as efficient datacenter operations.

- Cloud migration and edge compute: Enterprises increasingly rely on cloud-native AI services, hybrid architectures, and edge deployments. This broadens the footprint of AI infrastructure, expanding opportunity across both core data centers and distributed facilities.

- Networking and data movement: As AI workloads proliferate, high-speed interconnects, software-defined networking, and robust security layers become more critical. Networking equipment firms that can deliver low-latency, high-throughput solutions stand to gain from this trend.

- Energy efficiency: Sustainable data center design and advanced cooling technologies help reduce operating costs and environmental impact. Power utilities and equipment manufacturers that innovate in energy management approach are well-positioned for long-term growth.

Public reaction and market sentiment: a sense of urgency without political overtones

Investors and tech professionals alike express a clear sense of urgency around AI infrastructure readiness. The inclination is toward strategic pacing aligned with capacity, reliability, and cost controls. Stakeholders emphasize the importance of resilient supply chains, diversified sourcing, and transparent governance as AI infrastructure becomes more central to corporate competitiveness. At the same time, regional policy developments around data safety, electricity pricing, and tax incentives can shape project timelines and capital allocations in meaningful ways.

Key takeaways for the investment landscape

- Leadership in AI infrastructure has translated into meaningful outperformance versus the broader market and other AI-related categories, indicating a durable competitive edge for businesses anchored in compute, data centers, and cloud platforms.

- The diversification within the AI infrastructure group helps mitigate idiosyncratic risk. Semiconductors, data center operators, cloud providers, networking equipment firms, and power utilities each contribute unique strengths to a shared growth story centered on AI adoption.

- While mega-cap hyperscalers have delivered strong performance, the AI infrastructure cohort’s leadership suggests investors are rewarding the underlying assets and the scalable nature of AI deployment infrastructure.

- For investors seeking exposure to AI without relying on a single name, a balanced approach across hardware, cloud capacity, and energy efficiency plays can offer compelling risk-adjusted opportunities as the AI economy matures.

What this means for businesses and regions moving forward

Businesses evaluating AI investments should consider the total cost of ownership, including energy use, cooling efficiency, and equipment refresh cycles. A prudent strategy emphasizes not only a robust compute stack but also a resilient network backbone and scalable cloud arrangements that can adapt to evolving AI workloads. Regions aiming to attract AI infrastructure activity can create favorable environments through digital infrastructure incentives, clear data governance frameworks, and reliable energy supply, coupled with skilled talent pipelines and robust manufacturing ecosystems.

In the broader context of technology cycles, the current emphasis on AI infrastructure represents a pragmatic phase of converting theoretical capabilities into practical, enterprise-grade solutions. As organizations continue to push the boundaries of what AI can accomplish, the backbone that supports these innovations will likely remain vibrant, with continued capital expenditure and incremental productivity gains shaping both corporate performance and regional economic health.