Crude Oil Prices Surge to Six-Month High Amid Escalating Middle East Tensions

WTI Crude Jumps More Than 11% in One Month

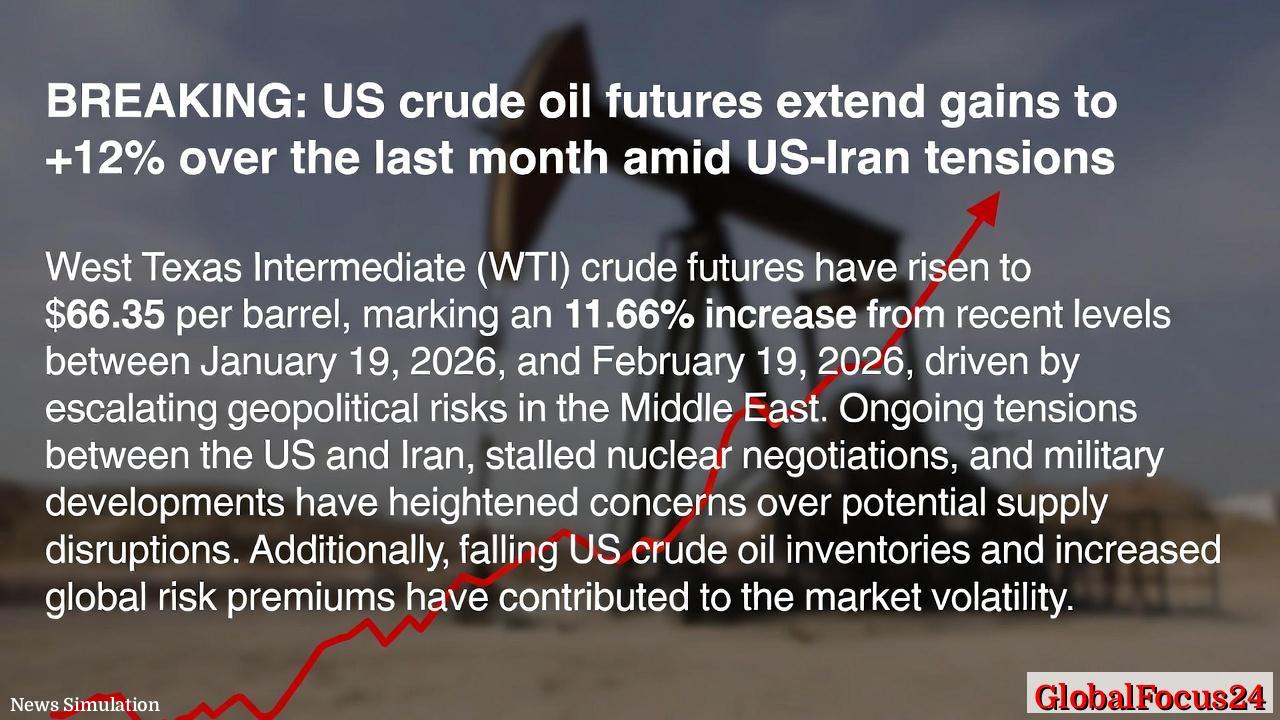

Crude oil markets have experienced a sharp rally over the past month, with West Texas Intermediate (WTI) crude oil climbing to $66.35 per barrel, marking an increase of $6.93 or 11.66% since mid-January. This surge represents the commodity’s highest level in six months, signaling a renewed period of volatility for global energy traders and renewed concerns over geopolitical stability in the Middle East.

From January 19 to February 19, 2026, investors have witnessed an intense rebound driven largely by escalating regional tensions, fears of potential conflict involving the United States and Iran, and uncertainty surrounding stalled nuclear negotiations. Energy markets, long regarded as sensitive to diplomatic rifts and military activity in the Persian Gulf, reacted swiftly to reports of missile testing, restricted shipping operations, and troop movements in the region.

Geopolitical Tensions Drive Momentum

The latest price surge is rooted in a climate of heightened geopolitical risk. The Middle East, home to major oil producers such as Iran, Iraq, and Saudi Arabia, remains central to the world’s energy supply. Any disruption—real or perceived—tends to ripple through futures markets. Reports of renewed hostilities and delays in diplomatic talks between Washington and Tehran have reignited fears of supply interruptions from one of OPEC’s most strategically significant regions.

Analysts note that the upward momentum is not solely speculative. With nuclear talks again at an impasse, and the U.S. reaffirming its commitment to enforcing sanctions on Iranian crude exports, investors are pricing in a tighter global supply outlook for the months ahead. Further complicating the situation, intelligence assessments suggest potential threats to maritime routes through the Strait of Hormuz, through which roughly a fifth of the world’s oil trade passes.

The situation echoes several past episodes of tension-driven price rallies, including the 2019 tanker incidents and the 2020 U.S.-Iran confrontation that briefly pushed WTI prices above $65. Then, as now, heightened military activity in oil-producing zones amplified perceived risk premiums and sent prices climbing despite relatively stable baseline demand.

Tightening U.S. Inventories Add Upward Pressure

The surge in crude prices has been reinforced by declining U.S. inventories, a factor reflecting both seasonal consumption patterns and ongoing supply adjustments. The Energy Information Administration (EIA) reported several consecutive weeks of stockpile draws through February, pointing to strong refining margins and robust exports.

Traders interpret falling inventories as confirmation that supply balances are tightening in North America, complementing geopolitical drivers from abroad. Refinery runs have increased as production remains steady but not excessive, allowing prices to climb without triggering a breakthrough in domestic output.

Moreover, the rebound in export demand—fueled by a weaker U.S. dollar and winter heating needs in Europe—has helped lift WTI contracts relative to Brent, narrowing a long-standing price gap. This dynamic highlights the degree to which the U.S. has reasserted itself as a crucial swing supplier in global energy markets, exporting crude and petroleum products at record volumes despite recent output moderation.

Historical Context: Lessons From Past Oil Shocks

The current scenario bears resemblance to past oil market disruptions, blending both supply-side constraints and political risk. Historically, crude rallies tied to Middle Eastern instability have produced significant economic ripple effects, particularly when sustained above key psychological thresholds.

In the late 1970s, the Iranian Revolution sent crude oil soaring by more than 130% within a year, triggering global inflationary pressures and redefining energy policy in Western economies. The Gulf War in 1990 prompted a comparable, though shorter-lived, spike amid production halts and regional uncertainty. In 2008, tensions coincided with speculative demand and a broader commodity boom, propelling prices above $140 per barrel.

While today’s $66 level is far from those extremes, analysts warn that oil markets remain acutely sensitive to geopolitical cues. Modern supply chains depend on real-time coordination—making even minor transport disruptions, cyber incidents, or strategic blockades capable of moving prices abruptly. The current environment, marked by both structural underinvestment and increased political unpredictability, mirrors these historic flashpoints in several ways.

Regional Comparisons: Diverging Energy Market Trends

The U.S. is not alone in confronting oil price pressures. European and Asian markets are also feeling the effects. Brent crude, the international benchmark, recently traded near $70 per barrel, reflecting a similar 10–12% surge over the same period. East Asian importers, particularly Japan and South Korea, have reported a rise in spot liquefied natural gas prices as buyers hedge against potential oil-linked energy shocks.

In contrast, some emerging economies—especially those with state-subsidized fuel systems—face a direct budgetary challenge from elevated import costs. India, one of the world's largest crude consumers, is already grappling with higher retail fuel prices and depreciating currency effects. The nation’s fiscal planners are closely watching global trends, concerned that a protracted rally could strain government finances and consumer sentiment alike.

Oil-producing nations, meanwhile, stand to benefit from the rally in the near term. OPEC members, particularly Saudi Arabia and Kuwait, view higher prices as a means to support national budgets and fund diversification agendas. However, these same states are wary of triggering demand destruction or stimulating renewed growth in U.S. shale output—a dynamic that has previously undercut sustained rallies.

Market Reaction and Economic Impact

The financial markets have responded swiftly to oil’s upward trajectory. Shares of major integrated energy firms—especially in the U.S. and Europe—have recorded moderate gains, buoyed by stronger margins and improved forward guidance expectations. Conversely, airlines, logistics companies, and fuel-intensive manufacturers face renewed cost pressures.

In inflation terms, analysts anticipate a modest but noticeable impact onconsumer price indices. Energy-related inflation can filter through supply chains, particularly as transportation and production costs rise. Economists estimate that if WTI stabilizes above $65 for several weeks, the U.S. inflation rate could increase by 0.2 to 0.3 percentage points in the second quarter of 2026.

The Federal Reserve and other central banks are watching closely, mindful that sustained commodity inflation can complicate monetary policy decisions. While energy price spikes often prove temporary, they carry strong psychological weight in consumer expectations and market sentiment. Businesses with exposure to energy-intensive operations may pass additional costs along to customers, contributing to entrenched inflation dynamics.

Energy Security and Policy Implications

Beyond immediate market effects, the latest oil rally underscores broader questions about global energy security and supply diversification. Policy analysts argue that repeated crises in the Middle East have revealed the fragility of the world’s oil supply structure. Despite advances in renewable energy and electrification, petroleum continues to account for roughly one-third of total global energy demand, leaving markets exposed to external shocks.

For the United States, energy independence through increased domestic production has mitigated, but not eliminated, vulnerability to global market turbulence. Although the U.S. has become a net exporter of petroleum products, its energy pricing remains linked to international dynamics. This linkage means geopolitical flare-ups abroad still directly influence gasoline prices at home.

Europe, still adjusting to post-Ukraine energy realignments, faces a similar challenge. The continent’s reduced reliance on Russian hydrocarbons has increased dependence on Middle Eastern and American supplies, highlighting the interconnected nature of the modern energy ecosystem. Asian economies, meanwhile, are accelerating renewable and nuclear initiatives to buffer against future oil market volatility.

Outlook for the Months Ahead

Market observers are divided on whether crude oil’s current rally will sustain through the second quarter. Some anticipate that tensions may de-escalate once diplomatic channels reopen, easing price pressures. Others believe that risk premiums will remain elevated, as regional fault lines and constrained investment in new supply create a structurally tighter market.

Analysts at major trading houses note that if WTI maintains levels above $65, U.S. shale producers could gradually ramp up drilling activity by spring, tempering the rally later in the year. However, that response may be slower than in previous cycles due to investor demands for capital discipline and debt reduction.

For now, oil traders remain focused on near-term developments in the Middle East and fresh inventory data from the U.S. Energy Information Administration. Each geopoliticalor production report is capable of triggering swift reactions across futures screens, underscoring how sentiment now drives movement as much as supply fundamentals.

Conclusion: A Renewed Era of Energy Volatility

The recent surge in WTI crude prices to $66.35 per barrel captures a moment of economic tension that extends far beyond the oil patch. With a combination of geopolitical uncertainty, tightening inventories, and fragile supply chains, the global energy market once again finds itself navigating a period of heightened volatility.

For producers, the rally offers an opportunity to recoup margins and reinforce national budgets. For consumers and policymakers, it is a reminder of how sensitive the modern economy remains to events half a world away. Whether this latest price shock proves temporary or the beginning of a sustained trend will depend on diplomacy, demand resilience, and the pace at which the world transitions to more stable energy alternatives.