U.S. Homebuilding Permits Drop in 2025 to Lowest Level Since 2019

Sharp Decline Reflects Slowing Housing Momentum

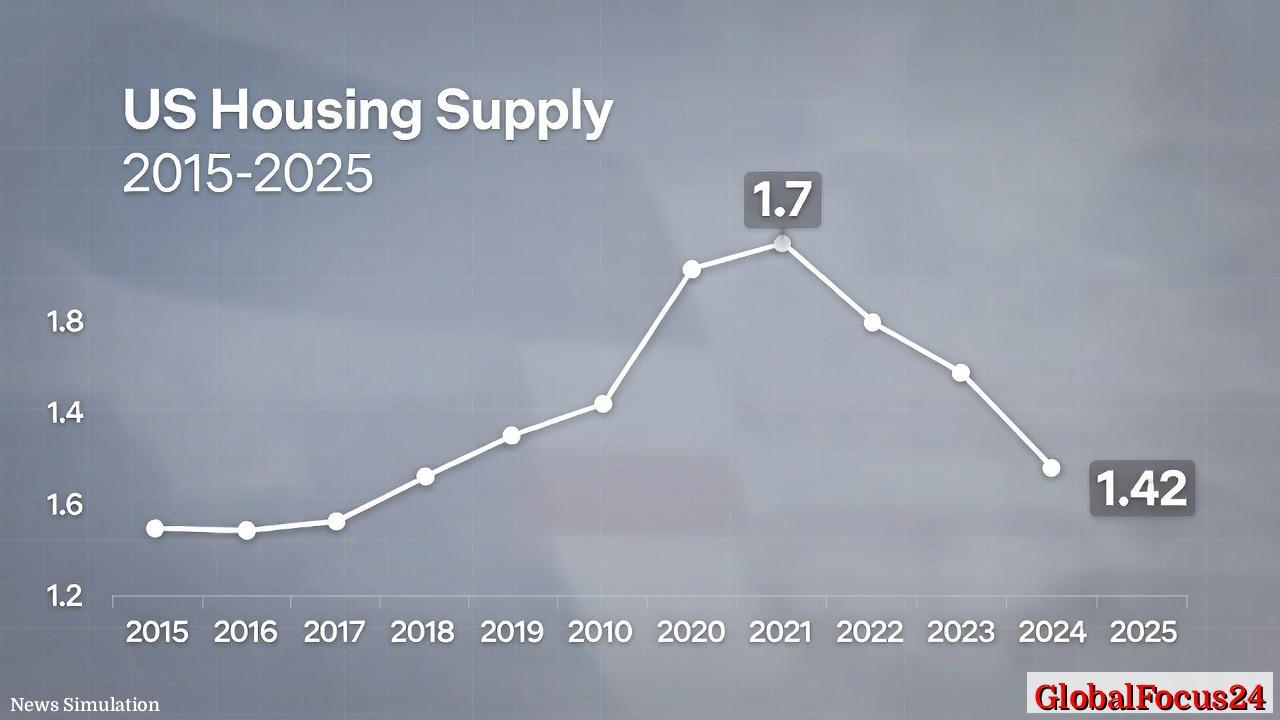

The pace of new home construction in the United States slowed sharply in 2025, with building permits for privately-owned housing units falling to their lowest level since 2019. According to newly released data, a total of 1.42 million housing units were authorized by building permits last year, marking a 3.6 percent decline from the 1.48 million total in 2024.

The trend extended a multi-year cooling in residential construction activity that began in 2022 after a pandemic-era boom. At its peak around 2021, permit authorizations reached an estimated 1.7 million units nationwide—the highest since before the 2008 housing market crash. The subsequent pullback underscores mounting pressures on the homebuilding industry, from high borrowing costs and tighter credit to persistent labor shortages and rising material prices.

Housing Permits Slide Below Pre-Pandemic Levels

The 2025 figure brought authorizations below the 2019 level of roughly 1.39 million, effectively erasing much of the post-pandemic surge that reshaped housing markets across the country. While residential construction remained resilient through much of 2023 and early 2024, the cumulative weight of economic headwinds began to show by mid-2025.

Permits, a leading indicator of future construction, serve as an advance gauge for housing supply. With the latest numbers, analysts warn that new housing starts could remain subdued well into 2026, tightening supply in markets already struggling with affordability constraints.

“Many builders are stepping back from new projects because of the uncertainty surrounding rates and costs,” said one industry economist. “Even though demand for homes remains strong, especially from younger buyers, financing new developments has become significantly more challenging.”

Economic and Financial Pressures on Builders

The construction slowdown reflects a combination of economic pressures that converged over the past two years. Following a rapid series of Federal Reserve rate hikes that began in 2022, mortgage rates have hovered near multi-decade highs, reducing both buyer affordability and builder confidence.

Material and labor costs also remain elevated, with some regional builders reporting double-digit cost increases compared with pre-pandemic baselines. Lumber and concrete prices, though off their pandemic peaks, continue to fluctuate due to supply chain constraints and high energy costs. Moreover, shortages in skilled labor—particularly framing carpenters, electricians, and plumbers—have added to development delays and budget overruns.

For smaller builders, access to credit tightened notably in 2025 as regional banks reined in exposure to real estate. Construction loans became harder to secure, and some projects stalled mid-development due to financing gaps. This combination of higher costs and lower demand for new units led many developers to postpone or scale back planned communities, especially in suburban and exurban markets.

Regional Divergences Highlight Broader Strains

While the national drop in permits was widespread, regional patterns reveal important differences. The South, which historically accounts for the largest share of U.S. housing construction, saw the steepest decline in 2025, driven by cooling markets in Texas and Florida. Both states had led the nation in new home starts throughout the early 2020s but began to experience rising inventories and slowing migration inflows by midyear.

In the West, particularly California and Arizona, higher construction costs and stricter permitting regulations continued to constrain new supply. Builders in those markets faced additional barriers such as land-use restrictions and extended review timelines, which further dampened permit issuance.

The Midwest showed comparatively moderate declines, supported by relatively stable demand in metro areas like Minneapolis, Chicago, and Kansas City. The Northeast remained the smallest regional contributor to new housing, constrained by limited land availability and aging urban infrastructure.

The Enduring Impact of High Interest Rates

The rise in borrowing costs has been one of the most decisive factors behind the recent decline. The average 30-year fixed mortgage rate held above 6.5 percent for most of 2025—roughly double the average rate recorded in 2021. That shift dramatically reduced affordability for first-time buyers and investors alike.

Higher mortgage rates not only discourage potential buyers but also cut into builders’ projected returns on new developments. As profitability margins shrink, developers often defer large-scale projects until financing conditions improve. This cyclical dynamic—where fewer permits lead to fewer starts—can prolong housing shortages over time.

Economists expect that if interest rates begin to stabilize or decline in 2026, homebuilding activity could gradually rebound, particularly in regions with strong population growth and employment opportunities. Until then, industry analysts anticipate continued caution among developers.

Comparing Cycles: Then and Now

The 2025 slowdown invites comparisons to previous housing market downturns, though the underlying fundamentals differ markedly from the 2008 crisis. Unlike the speculative bubble that preceded the Great Recession, today’s contraction stems largely from supply-side challenges rather than a collapse in demand or financing quality.

Homeownership rates remain historically stable, and delinquency rates are low. The issue, experts emphasize, is not excess inventory but insufficient new supply to meet demographic trends. Millennials entering their prime homebuying years, along with continued household formation, are keeping underlying demand firm—even as affordability deteriorates.

During the 2010s, building permit levels rarely surpassed 1.35 million annually, reflecting slow recovery from the last crash. The surge during 2020–2021 represented a rare exception, fueled by pandemic-era migration, record-low interest rates, and shifting work patterns that expanded suburban housing demand. The subsequent cooling, then, marks a reversion to more sustainable volumes—but one that comes with renewed scarcity concerns.

Implications for Homebuyers and Rental Markets

For homebuyers, the continued slowdown in construction could exacerbate the existing housing shortage that many cities already face. In fast-growing regions like Austin, Nashville, and Raleigh, inventory levels remain below long-term norms despite a reduction in transaction volumes.

A diminished pipeline of new homes also places upward pressure on rental rates, as more households delay homeownership. Multifamily construction has moderated less than the single-family sector but still faced headwinds in 2025, particularly amid rising insurance premiums and local zoning restrictions.

Rent growth began accelerating again in several metro areas where new supply tapered off, suggesting that affordability challenges may persist into 2026 even as home price appreciation cools.

Historical Context and Long-Term Outlook

Looking back over the past decade, the trajectory of building permits reflects a broader narrative about the U.S. housing market’s structural imbalances. From 2015 through 2019, permits grew steadily from about 1.2 million to 1.39 million units, tracking strong job and population growth.

The period from 2020 to 2021 brought an unprecedented surge as pandemic-era stimulus and low interest rates unleashed pent-up housing demand. By late 2021, authorizations had reached roughly 1.7 million—levels not seen since before 2006.

Since that peak, the market’s adjustment has been steady but significant. The 2025 total of 1.42 million units represents not only a retreat from that high point but a signal that post-pandemic construction tailwinds have largely dissipated. Builders and policymakers are now grappling with how to stabilize supply without reigniting inflationary pressures in construction costs.

Long-term projections suggest that to meet projected population growth and replace aging housing stock, the United States would need to sustain at least 1.5 million new housing completions annually through the 2030s. The current pace falls short of that mark, raising questions about future affordability and urban development patterns.

Outlook for 2026 and Beyond

As 2026 begins, most forecasts anticipate modest improvement, contingent on broader economic trends. If inflation continues to ease and the Federal Reserve moves toward rate reductions later in the year, improved financing conditions could spark a rebound in housing starts.

However, the persistence of supply chain bottlenecks and the high cost of land in key markets mean recovery is likely to be uneven. Builders remain cautiously optimistic, focusing on smaller, phased projects rather than large-scale developments.

In regions with ongoing population growth—particularly parts of the Southeast and Mountain West—even a modest pickup in permitting could have outsized effects. But nationwide, the legacy of high costs and restrictive zoning continues to constrain the pace at which the U.S. housing stock can expand.

A Market Searching for Balance

The 2025 drop in building permits underscores a housing market caught between strong underlying demand and mounting financial constraints. While the decline points to reduced construction activity, it also reinforces the structural tension defining today’s real estate landscape: too few homes for too many would-be buyers.

Whether the slow pace of new permits signals a temporary pause or a deeper recalibration will depend on the interplay of monetary policy, labor availability, and consumer confidence in the months ahead. What remains clear is that the housing market’s path forward will hinge on restoring balance—between affordability and supply, risk and reward, growth and sustainability—in an economy still adjusting to post-pandemic realities.