Data Center Construction Surpasses Office Development for First Time in U.S. History

A Structural Shift in Commercial Real Estate

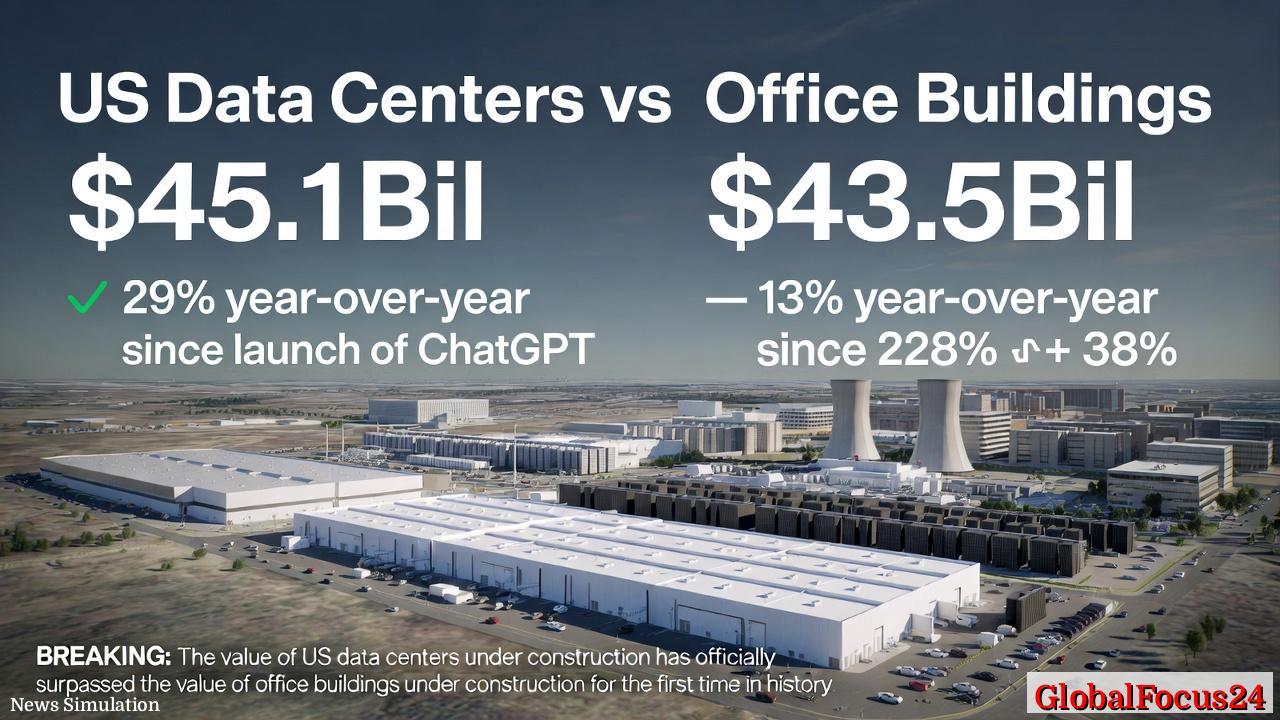

For the first time on record, the total value of data centers under construction in the United States has exceeded that of office buildings, marking a pivotal moment in the evolution of commercial real estate. New figures show that data center projects currently under development have reached $45.1 billion, a 29% increase year-over-year. In contrast, office construction has declined to $43.5 billion, down 13% over the same period and at its lowest level since October 2015.

The crossover reflects a deeper transformation driven by technological demand, changing workplace dynamics, and shifting investment priorities. As digital infrastructure becomes increasingly central to economic growth, the built environment is adapting accordingly.

The Rise of Data Centers in the Digital Economy

Data centers, once considered a niche segment of real estate, have rapidly become one of the most sought-after asset classes. The surge is closely tied to the expansion of cloud computing, artificial intelligence, and data-intensive applications. Since the launch of ChatGPT in November 2022, data center construction activity has increased by 228%, underscoring the scale and speed of this transition.

These facilities serve as the backbone of the modern internet, housing servers that power everything from streaming platforms and financial systems to enterprise software and AI models. As demand for processing power and storage grows, companies are racing to secure capacity, driving unprecedented levels of construction.

Major technology firms, cloud providers, and colocation companies are leading this wave of investment. Regions with access to reliable power, favorable tax policies, and robust fiber networks have emerged as hotspots for development. Northern Virginia, Dallas-Fort Worth, Phoenix, and parts of the Midwest have seen particularly strong activity, transforming into critical hubs of digital infrastructure.

Office Construction Faces Persistent Headwinds

While data centers surge ahead, the office sector continues to grapple with structural challenges. Office construction has declined by 38% since late 2022, reflecting a combination of reduced demand, evolving workplace patterns, and tighter financing conditions.

Remote and hybrid work models, accelerated during the pandemic, have fundamentally altered how companies use office space. Many organizations are downsizing footprints, delaying new projects, or repurposing existing buildings. Vacancy rates in several major cities remain elevated, discouraging new construction and dampening investor enthusiasm.

Developers are also contending with higher borrowing costs and stricter lending standards, which have disproportionately affected traditional office projects. In contrast, data centers often benefit from long-term leases with creditworthy tenants, making them more attractive in uncertain economic conditions.

Historical Context: From Skylines to Server Farms

The shift from office towers to data centers represents a broader evolution in how economic value is created and supported. For decades, commercial real estate was defined by central business districts, where high-rise office buildings symbolized corporate power and urban growth.

In the early 2000s, the expansion of the internet began to reshape this landscape, but data centers remained largely out of public view. It was not until the proliferation of cloud services in the 2010s that demand began to accelerate significantly. Even then, office construction continued to dominate, supported by steady employment growth and urbanization trends.

The turning point came in the early 2020s, when a convergence of factors—including the pandemic, digital transformation, and breakthroughs in artificial intelligence—dramatically increased reliance on data infrastructure. The result is a rebalancing of investment priorities that is now visible in construction data.

Economic Impact and Investment Trends

The growth of data center construction is having wide-ranging economic effects. These projects require substantial capital investment, specialized labor, and long-term planning, contributing to job creation in engineering, construction, and operations.

In addition to direct employment, data centers generate demand for related industries such as energy production, cooling technologies, and network connectivity. Utilities are playing a critical role, as data centers are among the most energy-intensive types of infrastructure. This has prompted increased investment in renewable energy and grid modernization in regions hosting large clusters of facilities.

From an investment perspective, data centers offer relatively stable returns compared to other real estate sectors. Long-term contracts, high occupancy rates, and strong tenant demand make them appealing to institutional investors, including pension funds and private equity firms. As a result, capital is increasingly flowing away from traditional office projects and into digital infrastructure.

Regional Dynamics and Emerging Hubs

The geographic distribution of data center construction highlights shifting regional dynamics within the United States. Northern Virginia remains the largest market globally, benefiting from its proximity to major internet exchange points and government infrastructure. Texas markets, particularly Dallas and Austin, have attracted significant investment due to favorable business conditions and abundant land.

Phoenix and other parts of Arizona have emerged as key locations, offering a combination of lower costs and strategic positioning in the western United States. Meanwhile, secondary markets in the Midwest are gaining traction, driven by access to affordable energy and central connectivity.

In contrast, traditional office-centric cities such as New York and San Francisco are experiencing slower construction activity. While these markets remain important economic centers, their development pipelines are increasingly focused on residential, mixed-use, or adaptive reuse projects rather than new office towers.

Infrastructure Challenges and Sustainability Concerns

The rapid expansion of data centers is not without challenges. One of the most pressing issues is energy consumption. Data centers require continuous power to operate servers and cooling systems, placing significant strain on local grids.

This has led to increased scrutiny from regulators and communities, particularly in regions where energy resources are constrained. Developers are responding by incorporating more energy-efficient designs, investing in renewable power sources, and exploring innovative cooling methods such as liquid cooling and heat reuse.

Water usage is another concern, especially in arid regions where data center growth is accelerating. Balancing the need for digital infrastructure with environmental sustainability is becoming a central consideration for both developers and policymakers.

Comparing Global Trends

The shift toward data center dominance is not unique to the United States, but the scale of activity sets it apart. In Europe, data center development is also expanding rapidly, particularly in markets such as Dublin, Frankfurt, and Amsterdam. However, stricter regulations and energy constraints have limited the pace of growth compared to the U.S.

In Asia, countries like Singapore and Japan have seen strong demand, though land scarcity and regulatory measures have influenced project pipelines. China continues to invest heavily in data infrastructure, supported by government initiatives and domestic technology firms.

Despite these global trends, the U.S. remains the largest and most dynamic market for data center construction, driven by its technology ecosystem, capital availability, and relatively flexible regulatory environment.

The Future of Commercial Development

The crossing point between data center and office construction values signals a broader redefinition of what constitutes essential infrastructure in the modern economy. While offices will continue to play a role, their dominance as the primary driver of commercial development is no longer assured.

Looking ahead, the trajectory of data center growth will depend on several factors, including technological advancements, energy availability, and regulatory frameworks. The continued expansion of artificial intelligence, in particular, is expected to sustain high levels of demand for computing power, further reinforcing the importance of data centers.

At the same time, the office sector may undergo a period of reinvention, with a focus on flexibility, collaboration, and mixed-use integration. Developers and investors are likely to adapt by diversifying portfolios and exploring new asset classes that align with changing economic realities.

A Turning Point in the Built Environment

The surpassing of office construction by data centers marks more than a statistical milestone; it reflects a fundamental shift in how physical space supports digital activity. As the economy becomes increasingly driven by data and connectivity, the infrastructure that enables these functions is taking center stage.

From sprawling server campuses to reimagined office spaces, the landscape of American development is evolving. The cranes on the horizon now tell a different story—one shaped not just by where people work, but by how information moves, processes, and powers the world around them.