U.S. Economy Marks One Year Under Trump’s Second Term with Mixed Indicators

The first anniversary of President Donald Trump’s second term unfolds amid a complex picture of economic performance, market dynamics, and public sentiment. After twelve months of policy shifts, global headwinds, and evolving fiscal strategies, the data reflect steady growth tempered by a slowdown in job creation and rising pressures on households and businesses. Analysts describe a landscape where resilience coexists with new vulnerabilities, underscored by evolving monetary policy tensions and shifting fiscal commitments.

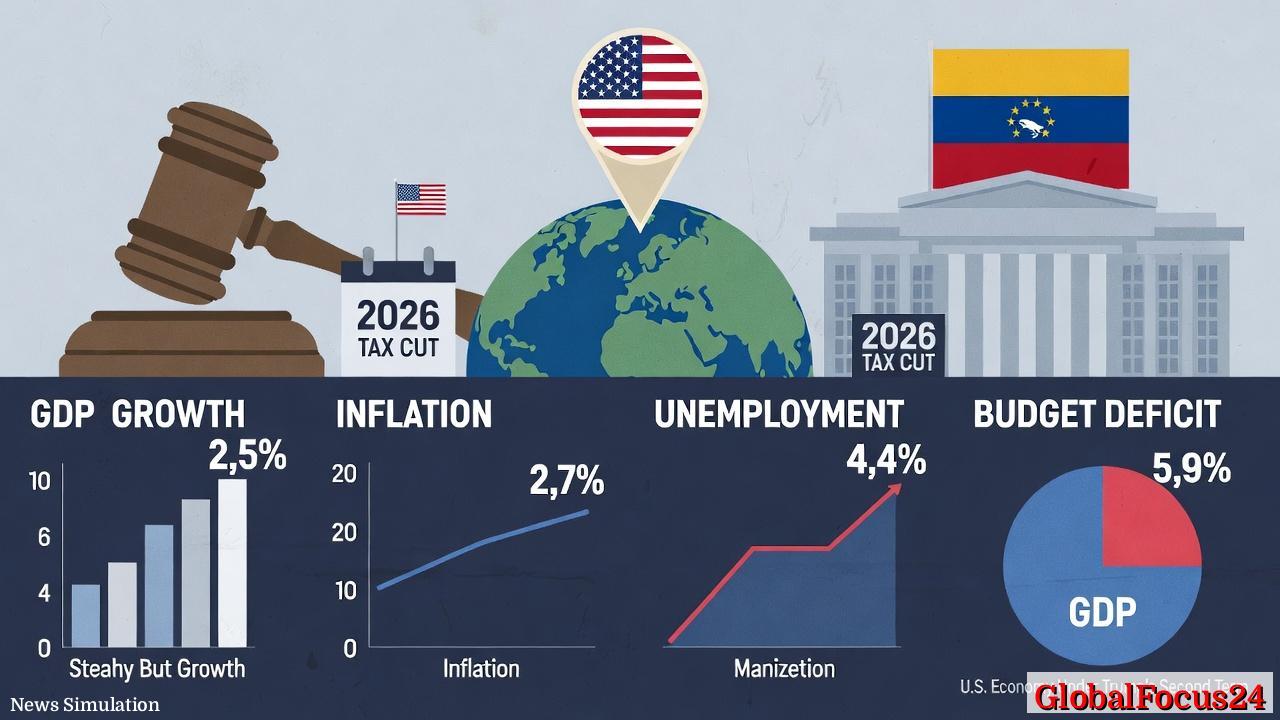

Historical context: growth patterns and policy inflection points Since the transition into the current presidential term, the macroeconomic environment has been shaped by a series of policy decisions, global trade developments, and domestic regulatory changes. The United States has experienced a continuation of moderate GDP growth, with 2025 projections hovering around 2.5 percent. This pace mirrors the prior year’s trajectory, suggesting a stabilization after a period of more rapid expansion. The growth pattern reflects a careful balancing act: supportive fiscal measures in some sectors, coupled with policy caution in others, including the central bank’s stance on inflation and employment.

Inflation dynamics and consumer prices Inflation trends remained relatively contained in 2025, with the consumer price index showing a 12-month variation of about 2.7 percent through December. This marks a slight easing from the prior year’s pace and aligns with the targeted range of many central banks seeking price stability. For households, the moderation in inflation translates into more predictable costs for essentials such as housing, groceries, and transportation, even as some price pressures—particularly in healthcare and energy—continued to pose challenges. In this environment, monetary policy has faced questions about how to calibrate rates to sustain growth while guarding against overheating or renewed price pressures.

Labor markets: momentum slowdown and employment shifting Labor market indicators paint a nuanced picture. The unemployment rate edged up from 4.1 percent at the end of 2024 to 4.4 percent by year-end 2025, a signal of softer momentum in employee demand as the economy matured. Job creation slowed markedly in 2025, with roughly 584,000 net new jobs added over the year, a sharp contrast to the approximately two million positions created in 2024. This deceleration is often interpreted as a transition phase: a full-employment environment gives way to a period of recalibration as hiring focuses on core efficiencies, automation, and sector-specific dynamics. Regions with robust export activity and technology sectors generally continued to show healthier hiring trends, while other areas faced more persistent wage and productivity pressures.

Fiscal developments: deficits, debt, and revenue streams The fiscal landscape in 2025 featured a modest improvement in the budget deficit as a share of GDP, estimated at around 5.9 percent, down from 6.4 percent the previous year. This improvement was aided in part by tariff revenues and revenue-raising measures tied to broader trade and tax policy changes. Yet the policy horizon suggests that future deficits could be influenced by upcoming tax reforms and the ongoing cost of servicing debt. The balance between short-term fiscal consolidation and long-run investment will remain a central topic for policymakers, particularly as demands for infrastructure modernization, education, and healthcare funding persist across diverse constituencies.

Healthcare costs and consumer impact Healthcare expenditures emerged as a critical concern for households and policymakers alike. Projections indicate that healthcare costs are set to rise substantially in 2026, driven by factors including prescription drug pricing dynamics, health insurance market transitions, and the ongoing demand for chronic disease management. For businesses, employer-sponsored health plans continue to absorb a meaningful share of compensation costs, influencing wage negotiations and hiring incentives. For individuals, rising out-of-pocket costs and insurance premiums can affect disposable income and consumer spending patterns, contributing to the broader tone of cautious optimism around the economy.

Monetary policy tensions and regulatory scrutiny A defining theme of the year has been heightened scrutiny of monetary policy and governance. Public discourse surrounding the Federal Reserve has intensified, with critics challenging policy directions and leadership approaches. Legal developments, including challenges related to mortgage documentation processes and related governance questions, have foregrounded the intersection of policy and legal accountability. The intersection of judicial oversight, policy credibility, and financial markets has added a layer of uncertainty to interest rate expectations and lending conditions. In this climate, the Fed’s credibility and the effectiveness of its communications have become central to market sentiment and business planning.

Regional snapshots: comparisons and contrasts Within the broader national narrative, regional performance has exhibited notable variation. Technology hubs and coastal metro areas with diversified economies have generally maintained steadier growth and more robust hiring than some interior regions, where industries such as manufacturing and energy face secular adjustments. States with strong export bases and highly skilled labor pools tended to experience more resilient employment momentum, while regions reliant on commodities or traditional manufacturing faced more pronounced slowdowns in job creation and wage growth.

Global context and regional spillovers International developments continue to shape domestic outcomes. Global supply chains, energy markets, and commodity prices have a continued impact on inflation, trade balances, and corporate investment decisions. The domestic policy stance toward trade, immigration, and regulatory modernization has outsized influence on multinational corporations and small businesses alike, affecting investment risk assessments and long-range planning. As economies around the world navigate similar cycles of growth and restraint, the United States remains a central node in a connected global economy where shifts in one region reverberate across others.

Public reaction and sentiment Public opinion on the economy reflects a mixed but pragmatic stance. Polling indicates that roughly half of voters perceive a deterioration in economic conditions over the past year, while a substantial minority reports improvement. This bifurcation underscores a common theme in modern economies: tangible gains in macro indicators can coexist with personal experiences of cost pressures and job-market flux. The discourse around fiscal and monetary policy, tax changes, and healthcare costs continues to shape consumer confidence and expectations for the year ahead.

Industry outlook: sectors aligning with the new economics

- Technology and innovation: Companies investing in automation, data analytics, and cloud-native capabilities continue to drive productivity enhancements, even as hiring scales adjust to evolving efficiency targets.

- Infrastructure and construction: Ongoing infrastructure modernization programs create near-term opportunities in materials, logistics, and skilled trades, with longer-term benefits for regional connectivity and resilience.

- Healthcare and life sciences: The healthcare sector remains a focal point for policy discussion, with demand patterns rooted in aging demographics, chronic disease management, and advancements in biotechnology.

- Energy and manufacturing: Regions with a competitive energy mix and export-oriented manufacturing activities are positioned to capitalize on global demand, though they face competing pressures from global price cycles and regulatory considerations.

What the data imply for the year ahead On balance, the economy appears poised for continued expansion at a moderate pace, tempered by several headwinds. The deceleration in job creation will require close attention from policymakers, particularly as inflation remains near target but risks outside the core mandate—such as healthcare cost inflation and potential fiscal shifts—could influence consumer behavior and business investment. The upcoming tax policy framework and any adjustments to the regulatory environment will likely shape the trajectory of capital formation, wage growth, and productivity gains.

Public infrastructure, workforce development, and innovation investments will be critical levers for sustaining momentum. Regions that invest in skills training, affordable housing, and transportation networks may better absorb shocks from global demand shifts and supply-chain disruptions. In the corporate sector, prudent risk management and flexible financing strategies will help firms navigate the uncertainties inherent in a recovering but imperfect economy.

Market signals and investor sentiment Financial markets have reflected a cautious optimism, balancing expectations of continued growth with the recognition of potential policy and regulatory risks. Debt markets, equity valuations, and commodity prices have responded to evolving policy statements and macroeconomic data, with investors seeking clarity on the pace of rate adjustments, the trajectory of fiscal deficits, and the framework for long-run growth.

Conclusion: a year of measured progress and unresolved questions A year into the second term, the U.S. economy exhibits a composite picture of resilience and complexity. Growth remains positive, price levels stable, and labor markets gradually adjusting to new dynamics. Yet the slowdown in job creation, rising healthcare costs, and ongoing policy tensions pose questions about the durability of momentum and the policy toolkit needed to sustain it.

As policymakers balance fiscal responsibility with investments in competitiveness, the broader economy will depend on continued innovation, effective governance, and targeted support for workers and communities navigating structural change. The coming months will test whether the constructive elements—productivity gains, selective fiscal support, and prudent monetary policy—can align with a sustained improvement in living standards and long-term economic health.