US New Home Median Price Sees Sharpest Drop in Over a Year as Market Pressures Mount

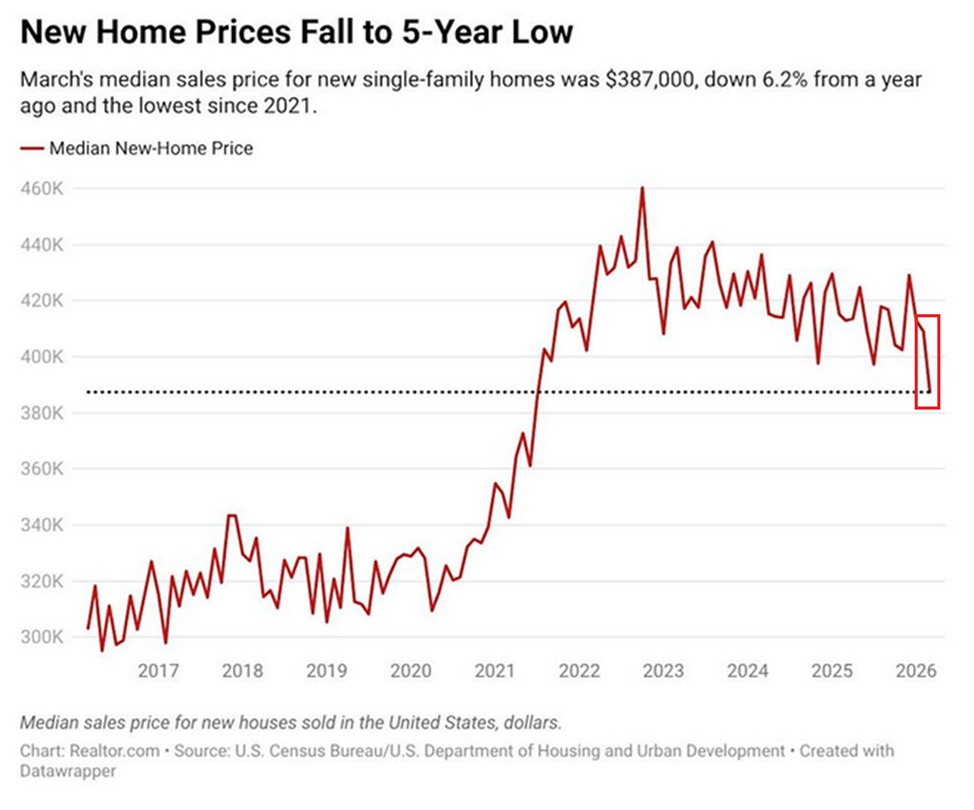

The median sales price for new single-family homes in the United States dropped significantly in March, signaling a notable shift in housing market dynamics and raising questions about affordability, demand, and broader economic conditions. The latest data shows a month-over-month decline of $21,600, or 5.3%, bringing the median price down to $387,400—the lowest level recorded since July 2021. When adjusted for inflation, the decline becomes even more pronounced, with real prices falling 6.3% to levels not seen since 2014.

The sharp decline marks the largest monthly drop since late 2024 and reflects mounting pressures across the housing sector, including higher borrowing costs, shifting buyer preferences, and uneven demand across price tiers.

Median and Average Prices Diverge Sharply

While both median and average home prices declined in March, the gap between the two widened to an unprecedented level. The average sales price fell 3.4% month-over-month to $503,100, its lowest point since mid-2025. At the same time, the spread between the average and median price expanded to $115,700, the largest on record.

This divergence reveals an important structural imbalance within the housing market. A relatively small number of high-end home sales continue to prop up the average price, while the majority of transactions are occurring at significantly lower price points. In practical terms, it suggests that luxury housing remains somewhat resilient, even as broader demand softens.

The widening gap also indicates that builders and sellers may be adjusting pricing strategies to attract more cost-sensitive buyers, particularly first-time purchasers who have been priced out in recent years.

Affordability Pressures Reshape Buyer Behavior

Affordability remains a central issue shaping the housing market. Mortgage rates, although stabilizing compared to earlier peaks, remain elevated relative to the ultra-low levels seen during the pandemic-era housing boom. Higher borrowing costs have reduced purchasing power for many households, forcing buyers to either delay purchases or shift toward lower-priced homes.

For example, a buyer who could afford a $450,000 home at a 3% mortgage rate in 2021 may now only qualify for a home closer to $375,000 at current rates. This recalibration has contributed to downward pressure on median prices as demand shifts toward more affordable segments.

Builders have responded by offering incentives such as rate buydowns, price reductions, and smaller home designs. These adjustments have helped maintain transaction volumes but have also contributed to declining median prices.

Historical Context: From Boom to Correction

The recent decline follows a period of extraordinary growth in home prices during 2020–2022, when a combination of low interest rates, remote work trends, and limited housing supply drove prices to record highs. During that period, annual price increases frequently exceeded 15% in many regions.

By mid-2022, however, rising inflation prompted the Federal Reserve to increase interest rates aggressively. Mortgage rates climbed rapidly, cooling demand and slowing price growth. While prices did not collapse nationwide, the pace of appreciation slowed significantly, and in some markets, outright declines began to emerge.

The March data suggests that the housing market may be entering a more pronounced correction phase, particularly in the new construction segment, where builders have greater flexibility to adjust pricing compared to the resale market.

Regional Variations Highlight Uneven Impact

The price decline is not uniform across the country. Regional trends reveal varying degrees of adjustment based on local economic conditions, supply levels, and migration patterns.

- In the Sun Belt, including states like Texas and Florida, increased housing supply has contributed to more noticeable price corrections. These regions experienced rapid construction growth during the boom years, and the resulting inventory is now putting downward pressure on prices.

- In the West Coast, particularly California, high home prices combined with elevated interest rates have led to reduced affordability, but limited land availability continues to constrain supply, moderating price declines.

- In the Midwest and parts of the Northeast, where price growth was more moderate during the boom, declines have been less pronounced, reflecting more stable demand and lower baseline affordability challenges.

Santa Clara and the broader Silicon Valley region, for instance, continue to exhibit unique dynamics. While high-income buyers and limited inventory support elevated price levels, affordability constraints remain significant, and even small shifts in interest rates can have outsized effects on buyer activity.

Economic Implications of Falling Home Prices

The housing market plays a critical role in the broader economy, influencing consumer spending, construction activity, and financial stability. A sustained decline in home prices can have several ripple effects:

- Reduced household wealth: Falling home values can dampen consumer confidence and spending, particularly among homeowners who rely on home equity as a financial cushion.

- Slower construction activity: Builders may scale back new projects in response to lower prices and softer demand, potentially affecting employment in construction and related industries.

- Shifts in rental markets: As homeownership becomes less accessible or attractive, demand for rental housing may increase, putting upward pressure on rents in certain areas.

However, declining prices can also have positive effects, particularly for first-time buyers who have struggled to enter the market. Lower prices, combined with potential easing in mortgage rates, could gradually improve affordability and expand access to homeownership.

Inventory and Supply Dynamics

Another key factor influencing the market is housing supply. Over the past year, inventory levels for new homes have increased as builders completed projects initiated during the boom period. This increase in supply has provided buyers with more options and reduced the competitive pressures that previously drove prices higher.

Unlike existing homeowners, who may be reluctant to sell due to low locked-in mortgage rates, builders are more motivated to move inventory, even if it means accepting lower prices. This dynamic has contributed to the sharper price declines observed in the new home market compared to the resale segment.

At the same time, long-term supply constraints remain a challenge. The United States has faced a housing shortage for over a decade, driven by underbuilding following the 2008 financial crisis. While recent construction has helped close the gap, it has not fully resolved structural supply issues.

Comparison to Previous Downturns

The current price decline differs in important ways from past housing downturns, particularly the 2008 financial crisis. Unlike that period, today’s market is not characterized by widespread subprime lending or excessive leverage among homeowners.

Instead, the current adjustment appears to be driven primarily by affordability constraints and interest rate dynamics rather than systemic financial instability. Mortgage underwriting standards remain relatively strict, and most homeowners have significant equity in their properties.

This distinction suggests that while prices may continue to adjust, the likelihood of a severe housing market collapse remains lower than in previous cycles.

Outlook for the Housing Market

Looking ahead, several factors will shape the trajectory of home prices:

- Interest rates: Any decline in mortgage rates could stimulate demand and stabilize prices, while sustained high rates may prolong the current downturn.

- Labor market conditions: Strong employment and wage growth could support housing demand, even in the face of higher borrowing costs.

- Builder strategies: Continued adjustments in pricing, incentives, and home design will play a crucial role in aligning supply with demand.

The March decline in median new home prices highlights the complex interplay of these factors and underscores the evolving nature of the housing market. While the drop represents a significant shift, it also reflects a broader rebalancing process after years of rapid growth.

As buyers, sellers, and policymakers navigate this transition, the housing market remains a key indicator of economic health, offering insights into both current conditions and future trends.