)

US Consumer Sentiment Plummets to Record Low as Inflation Fears Mount

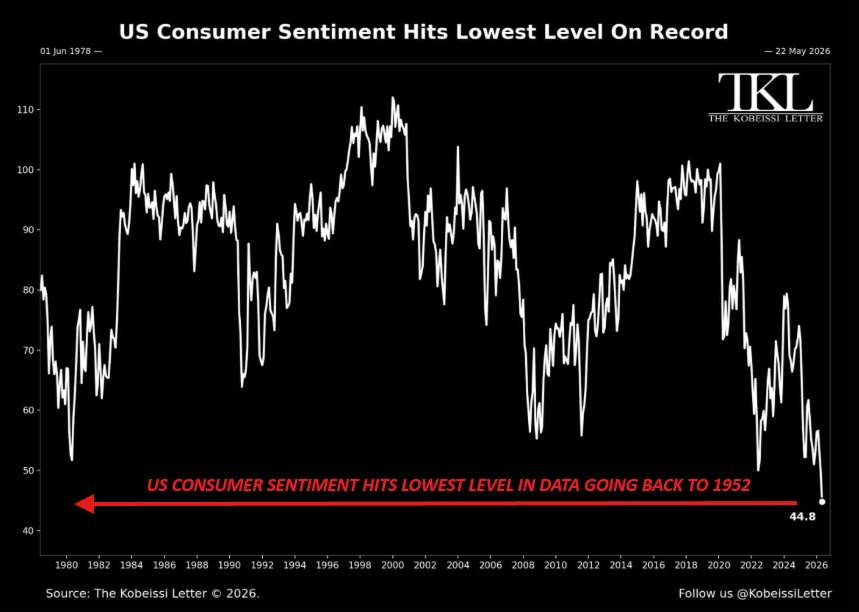

In a watershed moment for the US economy, consumer sentiment sank to its lowest level on record in data stretching back to 1952, marking a stark shift in public mood as households brace for higher prices and a tighter financial environment. The latest monthly readings show sentiment deteriorating by about 10 percentage points from the prior month, pushing the index down roughly 21% since February 2026. The result underscores a widening gap between consumers’ expectations and the improving economic indicators that have characterized the broader recovery in other sectors.

Historical context: waves of confidence and contraction Historical benchmarks illuminate the current mood swing. Consumer sentiment tends to move with the trajectory of inflation, interest rates, and labor market stability. During periods of rapid price growth, households often pull back on discretionary spending, prioritizing essentials and debt management. The latest downturn in sentiment echoes prior episodes where inflation surprises or perceived policy missteps prompted households to adjust their spending plans, even when unemployment remained relatively low by historical standards.

At a broader scale, sentiment has proved to be a powerful leading indicator for consumer spending, which constitutes roughly two-thirds of US GDP. When confidence wanes, even financially solvent households may tighten budgets, delaying purchases of durable goods such as automobiles and appliances, or deferring major home improvements. Conversely, a rebound in confidence can spur a pickup in retail activity and a faster-than-expected stabilization of demand. The current record low suggests a high bar for a near-term, sustained rebound in consumer activity, even as some segments of the economy demonstrate resilience in other indicators.

Economic impact: ripple effects across households and markets The direct implication of plunging consumer sentiment is a softer near-term outlook for consumer spending growth. Retail data, which tracks a broad spectrum of purchases from groceries to electronics, has already shown uneven momentum, with categories such as essential goods outperforming discretionary sectors. When households anticipate higher prices in the year ahead, they often accelerate purchases in the short term for fear that costs will rise further, which can temporarily bolster retail sales but may intensify inventory and price pressures in the longer run.

Inflation expectations play a central role in shaping behavior. If households expect inflation to run at or near 4.8% over the coming year, as the current reading suggests, households adjust their budgets accordingly. This can manifest as increased savings rates, more conservative debt management, and a tilt toward value-oriented shopping. For businesses, elevated inflation expectations translate into higher input costs and a demand environment that remains uncertain. Firms may respond by adjusting pricing strategies, re-evaluating investment plans, and prioritizing efficiency improvements to protect margins.

Labor market dynamics remain a critical, stabilizing factor. An employment backdrop characterized by steady wages and low unemployment can temper the severity of a sentiment downturn, supporting continued consumption in essential categories. However, if the sentiment decline reflects deeper worries about job security or real wage declines, the risk of a self-reinforcing slowdown in household spending rises. Policymakers watch these signals closely, alongside inflation data, as they calibrate monetary policy, aiming to balance price stability with growth.

Regional comparisons: different footprints, similar anxieties Regional dynamics offer additional nuance to the national picture. Coastal economies with high living costs may experience sharper sentiment deterioration due to amplified housing affordability pressures and interest-rate sensitivity on mortgages. In contrast, inland regions with resilient labor markets and lower price levels may exhibit more muted sentiment shifts, though concerns over healthcare costs, transportation, and housing remain pervasive. The divergence highlights how inflation expectations interact with regional cost structures, wage differentials, and industry mixes to shape consumer confidence locally.

Small businesses feel the reverberations as well. In communities reliant on discretionary consumer spending or seasonally driven sectors, sentiment weakness often translates into more conservative hiring plans or delayed capital expenditures. Yet, in areas with robust tourism, energy activity, or essential services, the impact may be less pronounced in the short term, even as executives monitor macroeconomic signals for longer-term planning.

Policy and expectations: the policy landscape and market psychology The sentiment trajectory occurs in a policy environment calibrated to address inflation while supporting growth. Central bank communications, forward guidance, and quantitative policy measures influence consumer expectations as much as financial conditions do. When households anticipate higher prices or tighter financial conditions, they may adjust their behavior before any official policy change takes effect, creating a lagged but potent impact on real-time demand.

Market participants, including investors and corporate strategists, parse sentiment alongside earnings, supply chains, and global developments. A downturn in consumer confidence can elevate concerns about growth trajectories, prompting reevaluation of capex plans, inventory management, and risk pricing. Conversely, the absence of a prolonged deterioration in sentiment—despite inflation pressures—can signal resilience in consumer balance sheets and a broader steadiness in the macroeconomy. The current readings, therefore, will influence the tempo of adjustments across sectors, from retailers to manufacturers and service providers.

Regional resilience and the path forward Looking ahead, the trajectory of consumer sentiment will likely hinge on how effectively price pressures ease and how households manage debt and savings in a higher-rate environment. Policymakers’ ability to anchor inflation expectations will be crucial. If inflation progress continues to slow and real wage growth picks up modestly, sentiment could stabilize, supporting a gradual return to pre-crisis confidence levels. In such a scenario, consumer spending would resume a more typical pattern, favoring a mix of durable goods, services, and experiences that underpin broader economic activity.

In the near term, sectors tied to non-discretionary spending—groceries, healthcare, and essential services—may maintain steadier demand, offering a buffer against more pronounced declines in leisure or luxury categories. Retailers and manufacturers that adapt quickly to shifting consumer preferences, optimize pricing, and manage inventories stand a better chance of mitigating the effects of sentiment volatility. Firms investing in value propositions, flexible supply chains, and digital channels can capitalize on evolving consumer behavior even as confidence remains fragile.

Public reaction: households respond with prudent reprioritization Public sentiment typically translates into a mix of caution and pragmatism. Consumers may increase savings rates, seek more affordable alternatives, and postpone nonessential purchases. This reprioritization can manifest in shared community efforts—such as price-conscious shopping, increased use of discount retailers, and greater attention to energy efficiency. Such behavior not only influences immediate consumer markets but can also affect long-run economic trajectories if it persists beyond the temporary shock, altering demand patterns across industries.

Outlook: navigating a challenging terrain The record-low consumer sentiment underscores a moment of heightened uncertainty for households and policymakers alike. As inflation expectations hover near 4.8% for the year ahead, the imperative for clear, credible policy guidance and durable supply-side improvements becomes more pronounced. The economy’s resilience will depend on a careful balance: maintaining consumer access to affordable goods and services while fostering an environment conducive to investment, productivity gains, and innovation.

Analysts will be watching a constellation of indicators—labor market stability, wage growth, inflation dynamics, and consumer spending after the release—to gauge the durability of any forthcoming improvement in confidence. A potential stabilization could arise from a combination of easing inflation, favorable energy costs, and continued job creation in sectors less sensitive to consumer sentiment swings. Alternatively, if inflation reaccelerates or mortgage costs rise decisively, sentiment could deteriorate further, feeding a cycle of cautious consumer behavior and slower growth.

Regional signals and sector-specific prospects will be essential to understanding the macro landscape. For retailers and consumer-facing industries, the present mood calls for strategic adjustment: prioritize value, optimize inventory, and enhance the omnichannel customer experience to weather a period of constrained spending. For policymakers, the message is clear: maintain transparent communication about inflation trajectories and policy objectives to anchor expectations and support household financial planning.

In sum, the latest figures mark a critical juncture in the ongoing economic narrative. With consumer sentiment at historic lows and inflation expectations elevated, households are recalibrating their budgets, hustling to balance short-term needs with longer-term financial health. The path forward will hinge on the interplay between inflation containment, wage growth, and the continued resilience of the labor market, all within a regional framework that reflects divergent experiences across the United States.

Note on methodology and context The sentiment measure in question captures consumer attitudes toward current conditions and near-term business and employment prospects. While it is a powerful gauge of confidence, it is one of several indicators used to assess the health of household finances and spending patterns. Analysts compare sentiment with actual spending data, inflation readings, and labor market statistics to develop a holistic view of the economy’s momentum. Understanding these relationships helps explain why sentiment can swing even as other metrics show signs of continued, if uneven, progress.

Public discourse around inflation and policy continues to shape expectations. As households adjust to a higher-cost environment, the role of price stability becomes increasingly salient. This dynamic, in turn, influences decisions about saving, borrowing, and consumption, creating a complex feedback loop that policymakers and markets must navigate with care.

For readers seeking a concise takeaway: when confidence wanes in tandem with rising inflation expectations, consumer behavior tends toward precautionary spending, which can temper near-term growth but does not automatically spell a downturn. The broader economic narrative remains contingent on the trajectory of inflation, the strength of the labor market, and the effectiveness of policy responses in stabilizing prices while supporting opportunity and investment.