U.S. Federal Budget Deficit Narrows Sharply in January as Revenues Surge

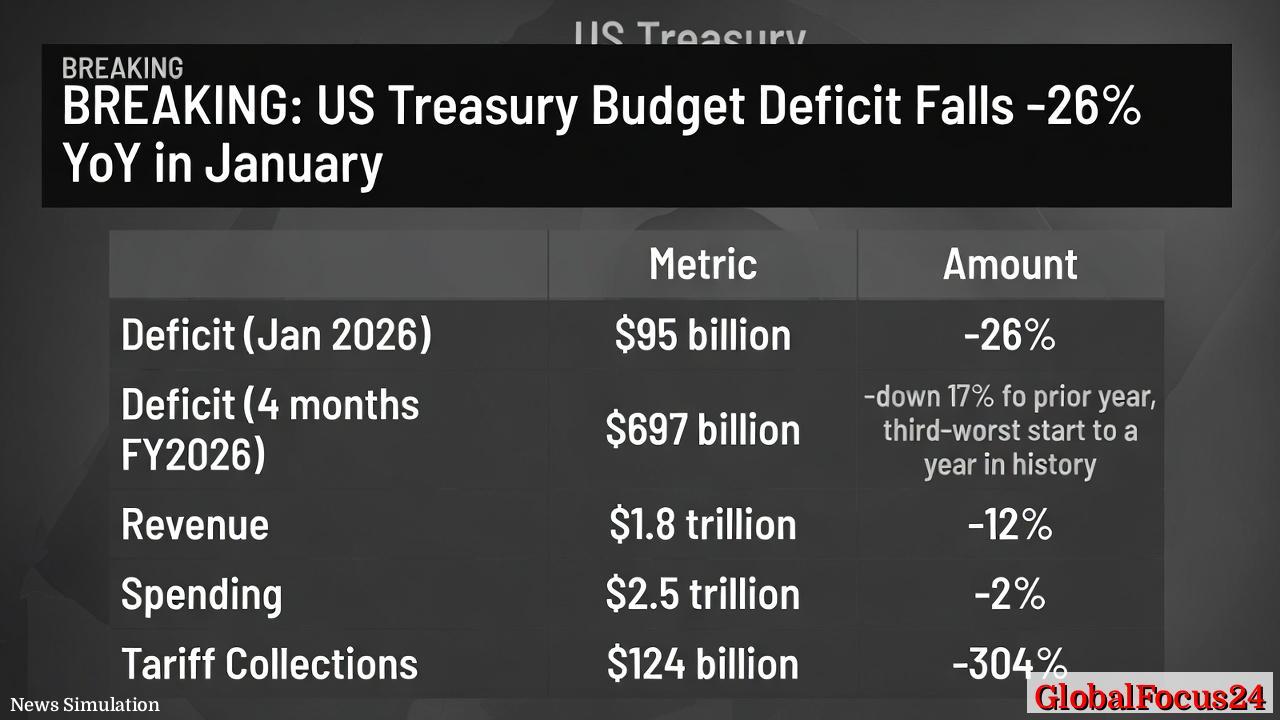

The U.S. federal budget deficit contracted to $95 billion in January, marking a 26 percent decline compared with the same month a year earlier, according to the latest Treasury Department data. The improvement comes amid robust revenue growth driven largely by a surge in tariff collections, offsetting modest spending increases that continued to weigh on federal finances.

Over the first four months of fiscal year 2026, which began in October, the cumulative budget deficit fell 17 percent to $697 billion. Although the shortfall remains among the largest in the nation’s history, ranking as the third-worst start to a fiscal year on record, the recent contraction offers tentative signs of fiscal stabilization following several years of pandemic-related spending and rising interest costs.

Revenues Strengthened by Tariff Windfall

Federal revenues climbed 12 percent from a year earlier to reach approximately $1.8 trillion during the first third of the fiscal year. The most striking change came in tariff collections, which soared 304 percent to $124 billion. Economists attribute much of that growth to newly imposed or expanded duties on imported goods, particularly in sectors such as semiconductors, steel, and consumer electronics, as well as the enforcement of previously delayed tariff increases introduced to bolster domestic manufacturing.

Personal and corporate income tax receipts also rose, reflecting sustained employment levels and strong corporate profits in late 2025. A resilient labor market, combined with slower inflation, helped maintain consumer purchasing power and steady wage growth. The Treasury noted that higher quarterly estimated tax payments added to January’s revenue strength, a pattern consistent with post-holiday collections in recent years.

Spending Growth Remains Measured

Total federal outlays increased 2 percent year-over-year to $2.5 trillion over the same four-month period. The pace of spending slowed compared with prior years, when emergency health measures, infrastructure programs, and debt-servicing costs expanded rapidly. Defense expenditures and entitlement programs continued to comprise the largest shares of federal spending, but the growth rate of those categories moderated as several pandemic-era programs fully expired.

Interest payments on the national debt — now exceeding $34 trillion — remain one of the government’s fastest-growing obligations. While the Federal Reserve’s decision to pause rate hikes late last year helped ease borrowing costs slightly, much of the U.S. debt has already been refinanced at higher rates, ensuring that interest expenses stay elevated. Economists estimate that interest costs could reach nearly $1 trillion for the full fiscal year, consuming a record share of total federal expenditures.

Historical Context and Long-Term Trends

Despite the recent reduction, the 2026 fiscal shortfall remains substantial by historical standards. Prior to the pandemic, annual deficits typically ranged between $500 billion and $800 billion. Extraordinary borrowing during 2020 and 2021 to fund public health responses and economic recovery programs expanded the deficit to levels unseen since World War II, peaking at over $3 trillion in fiscal 2020.

Since then, the federal government has gradually reduced emergency spending, but structural challenges continue to drive persistent deficits. Demographic shifts — particularly the aging of the Baby Boomer generation — have put sustained pressure on Social Security, Medicare, and other entitlement programs. At the same time, the combination of lower personal savings, higher debt servicing costs, and constrained discretionary funding creates a narrow fiscal margin for responding to future economic shocks.

The Treasury Department’s data indicates that, although short-term revenue gains have boosted collections, much of the improvement depends on temporary factors such as one-time tariff surges and delayed tax payments from high-income earners. Financial analysts caution that maintaining revenue growth without hindering consumer spending or industrial activity will require careful balance in trade and fiscal policies.

The Economic Backdrop

The latest budget report arrives as the U.S. economy continues its gradual, but steady, expansion. Real GDP grew at an annualized rate of 2.4 percent in the fourth quarter of 2025, supported by strong consumer demand and rising business investment in energy and technology sectors. Inflation cooled to an annual rate of 2.3 percent in January, marking a return to near the Federal Reserve’s long-term target after two turbulent years of price volatility.

Labor market resilience has been critical to sustaining federal revenues. The unemployment rate held at 3.8 percent in January, and average hourly earnings rose 4.1 percent from a year earlier. These figures underpin both individual tax receipts and consumption-driven growth, which together bolster the federal government’s fiscal base. However, analysts warn that productivity gains have lagged behind wage increases, a dynamic that could limit income growth and tax inflows later in the year.

Bond markets have responded cautiously to the improving deficit picture. Treasury yields eased modestly in early February, reflecting stronger investor confidence in the government’s near-term fiscal management. Yet the downward pressure on yields may remain constrained as the Treasury continues issuing long-term debt to refinance maturing obligations at higher rates.

Regional and Global Comparisons

The United States’ deficit trajectory remains steeper than that of most major advanced economies. The European Union’s aggregate fiscal deficit narrowed to roughly 3 percent of GDP in 2025, supported by strict budgetary rules and slowing inflation. Japan’s fiscal deficit, though still high, has stabilized due to moderate economic growth and disciplined spending. By contrast, U.S. deficits have averaged more than 5 percent of GDP over the past decade — a level rarely seen in peacetime outside of economic crisis years.

Despite the scale of U.S. borrowing, global demand for Treasury securities remains robust, reflecting the dollar’s dominance and the perceived stability of American institutions. Foreign holdings of U.S. debt grew modestly in 2025, led by incremental purchases from investors in Europe and the Middle East. Rising energy revenues and trade surpluses in those regions have supplied global liquidity that continues to flow into U.S. asset markets.

Domestically, however, the fiscal burden varies across regions. States with larger industrial bases and heavy trade exposure — such as Texas, California, and Ohio — have experienced both gains and challenges from tariff-driven revenue growth. Higher import costs have pressured some manufacturers but benefited local production, particularly in sectors shielded by protective duties. Regional tax revenues have likewise improved, reflecting stronger employment and corporate activity tied to reshoring efforts.

Policy Outlook and Fiscal Risks

Looking ahead, fiscal analysts expect the 2026 deficit to remain below last year’s total but warn that structural pressures will limit further improvement without policy adjustments. The Congressional Budget Office projects that absent changes to current law, deficits will rise steadily again by the end of the decade, driven by entitlement spending and interest costs. While near-term revenue growth from tariffs and taxes offers relief, it may not offset long-term obligations tied to demographic and healthcare trends.

The administration has emphasized continued investment in domestic manufacturing, infrastructure modernization, and technology research as essential to maintaining economic competitiveness. These initiatives, while growth-oriented, could require additional deficit financing unless offset by higher tax revenues or spending cuts elsewhere. Meanwhile, calls for fiscal discipline from market observers and credit rating agencies underscore the delicate balance between expansionary policy and debt sustainability.

One of the most immediate uncertainties stems from global trade dynamics. If tariff-related revenues continue to surge, they could provide a short-term cushion for federal finances. However, prolonged trade frictions risk inflationary effects and potential retaliation from trading partners, which might ultimately slow economic growth and reduce the very revenue streams now bolstering the Treasury’s balance sheet.

A Tentative Turning Point

January’s fiscal report offers a cautiously optimistic signal for the U.S. budget outlook. The narrowing deficit suggests that higher revenues can help offset the weight of persistent spending and interest obligations, at least temporarily. Yet the underlying fiscal challenges — from rising entitlement costs to large-scale borrowing requirements — remain unresolved.

Historically, meaningful deficit reductions have occurred during periods of strong economic growth combined with disciplined federal budgeting, such as the late 1990s balanced budget era. Whether similar conditions can emerge in the current environment will depend on sustained productivity gains, stable interest rates, and prudent fiscal management over the coming decade.

For now, the Treasury’s report underscores both the progress made and the scale of the challenges ahead. A 26 percent year-over-year decline in January’s shortfall reflects stronger revenue performance and disciplined spending growth, but also highlights the limits of one month’s improvement in the face of long-term fiscal headwinds. The U.S. economy enters the remainder of fiscal 2026 with renewed momentum — and a growing awareness that managing the deficit will require a sustained, strategic effort well beyond the current recovery.