Record High Subprime Auto Delinquency Signals Strain Across U.S. Credit Markets

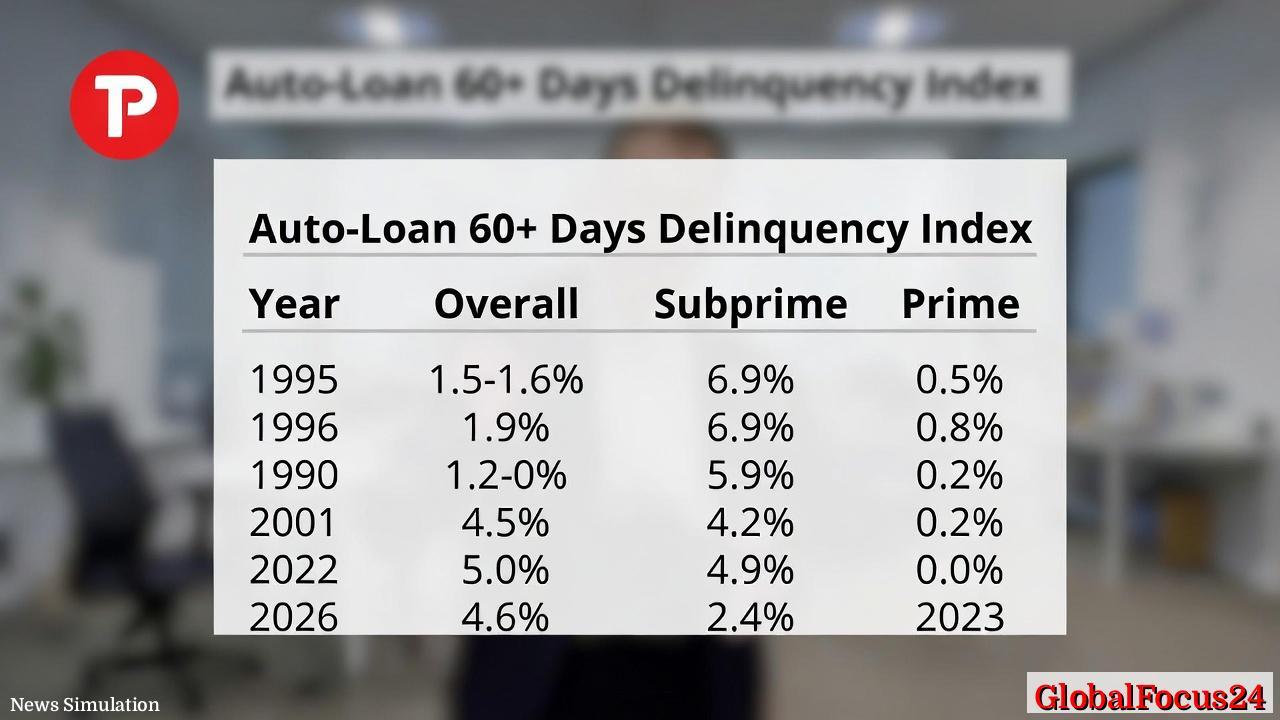

Subprime auto loan delinquencies have surged to a new record, with the 60-plus-day delinquency rate reaching 6.9 percent, according to the latest data. Analysts describe the milestone as a clear signal of mounting strain in consumer credit, as households grapple with higher vehicle costs, tighter budgets, and shifting economic pressures. The rise comes after a multi-year period of steadily increasing total auto debt, and it reverberates beyond auto finance into broader financial stability considerations for lenders, policymakers, and regional economies.

Historical context: a long arc of rising risk in auto lending

To understand the current rupture, it helps to place it in historical context. Auto lending has long acted as a leading indicator of consumer credit trends. In the mid-1990s, the delinquency environment for subprime borrowers was relatively contained, reflecting lower overall debt levels and more favorable financing terms. The late 2000s financial crisis brought a stark contrast: while prime borrowers remained comparatively stable, the broader subprime segment experienced heightened distress as unemployment and housing market disruption weighed on disposable income and credit access.

Since then, the landscape has evolved in two notable ways. First, total auto debt has swelled substantially. Five years ago, American households carried roughly $1.36 trillion in auto debt. Today, total auto debt has climbed to about $1.67 trillion, an increase of roughly $312 billion. The driver is not only more vehicles on the road but higher vehicle prices, ongoing demand for new models with advanced features, and rising sticker prices in a competitive auto market.

Second, risk dispersion within auto lending has shifted. Subprime financing, which underpins a sizable share of new and used-car lending, now amounts to about 14 percent of all auto loans, translating to roughly $234 billion outstanding in subprime credit. This segment, historically more sensitive to economic downturns, has faced intensified pressure as households confront higher costs for fuel, insurance, maintenance, and loan payments. The delinquency rate for subprime loans has more than doubled since 2021, underscoring a deterioration in timely repayment within this cohort.

Economic impact: spillovers to lenders, consumers, and regional markets

- Lending and credit availability: A rising delinquency environment increases the risk profile of auto portfolios held by banks, credit unions, and nonbank lenders. As delinquencies rise, lenders may tighten underwriting standards, raise interest rates on new subprime loans, or reduce available credit for borrowers with weaker credit histories. That tightening can create a cycle in which reduced access to affordable financing limits vehicle purchasing power, potentially slowing new-car sales and impacting dealership volumes.

- Consumer cash flow and household balance sheets: For households carrying subprime debt, higher delinquencies often correlate with elevated financial stress. Delinquent auto payments can affect credit scores, which in turn influences the cost and availability of other forms of credit, including credit cards and mortgages. Financial strain from elevated vehicle costs—driven by price increases and maintenance needs—can squeeze households’ discretionary income, complicating budgeting for essentials such as housing, utilities, and healthcare.

- Vehicle supply chain implications: Auto debt dynamics can influence consumer demand signals that reverberate through the supply chain. If delinquencies presage cooler demand, manufacturers and suppliers may adjust production plans, prices, and incentives. Regional economic ecosystems—especially those with a dense network of auto dealers, service centers, and related jobs—may experience slower growth or temporary shocks as consumer spending reallocates.

- Regional comparisons: varying regional exposure highlights different risk profiles. Areas with higher concentrations of subprime lending, stronger auto-dependent economies, or elevated vehicle prices can exhibit more pronounced delinquency pressures. Conversely regions with more robust employment growth, higher wage gains, and lower vehicle prices may experience relatively milder strain. In practice, delinquency patterns often track local labor markets, household debt service capacity, and regional costs of living.

Data interpretation: what the numbers imply for the near term

- The 6.9 percent 60+ day delinquency rate for subprime auto loans surpasses the 1996 peak by 0.9 percentage points and exceeds the 2008 financial crisis high of 5.0 percent. This comparison signals that current stress levels are historically elevated, even when adjusted for the different regulatory, economic, and lending environments that characterize each period.

- Overall auto loan delinquency trends have climbed but remain lower than subprime peaks, indicating that risk is concentrated within the subprime segment rather than distributed evenly across all borrowers. Prime borrowers continue to exhibit comparatively low delinquency rates, reinforcing the notion that credit quality remains a key differentiator in the current dynamics.

- The resilience or fragility of the broader consumer economy hinges on several factors, including unemployment trends, wage growth, inflation, and monetary policy. If labor markets stay strong and inflation moderates without triggering a recession, some of the headwinds on auto debt may ease as households regain disposable income and refinancing options improve. If economic conditions deteriorate, delinquencies could persist or worsen, creating additional financial pressure on lenders and borrowers alike.

Regional case studies: how different markets are coping

- Coastal metro areas with high vehicle prices and dense urban populations have seen notable stress in subprime auto portfolios, driven by elevated ownership costs and greater reliance on transportation for commuting. In these regions, even modest shocks to fuel prices or insurance premiums can affect loan repayment capacity.

- Midwestern manufacturing hubs, where auto industries have a significant footprint, face a complex mix of wage dynamics and debt exposure. Regions with strong job retention and higher median incomes may sustain better loan performance, but localized disruptions in auto supply chains or factory activity can translate into broader consumer effects.

- Sun Belt markets, characterized by rapid population growth and expanding vehicle fleets, show a nuanced picture. When wage growth matches or outpaces price increases, delinquency pressures can ease. But if vehicle costs rise faster than incomes, subprime borrowers may face sharper repayment challenges, amplifying regional risk concentrations.

Policy implications and lender responses

- Prudence in underwriting and credit monitoring remains essential. Lenders may emphasize enhanced oversight of subprime portfolios, tighter risk controls, and more frequent performance reviews to identify emerging trouble spots early. Dynamic credit scoring models that account for shifting consumer behavior can help institutions manage risk without withdrawing essential credit from creditworthy borrowers.

- Consumer protection and financial education initiatives can support households in navigating higher auto costs. Programs that promote budgeting, debt management, and access to affordable refinancing options contribute to longer-term financial resilience for borrowers at risk of delinquency.

- Public-private collaboration can play a role in stabilizing markets where auto debt exposure is most acute. Coordinated efforts to address affordability, insurance costs, and transportation access can reduce the likelihood of cascading financial distress in communities heavily reliant on vehicle mobility.

What this means for readers and everyday readers

- For borrowers: If you’re managing subprime auto debt, consider reviewing your repayment plan, exploring refinancing options, and seeking counseling if you’re feeling stretched. Small adjustments to repayment schedules or interest terms can yield meaningful relief over time.

- For investors and lenders: The current delinquency environment underscores the importance of robust risk analytics, diversified portfolios, and contingency planning. Maintaining liquidity buffers and stress-testing scenarios can help institutions weather rising delinquencies without abrupt market disruption.

- For policymakers and community leaders: Monitoring delinquency trends and supporting affordable financing pathways can help sustain consumer mobility without contributing to systemic risk. Local initiatives to align wage growth with living costs and improve access to affordable transportation can bolster regional economic stability.

Conclusion: navigating a turning point in auto finance

The record 6.9 percent delinquency rate among subprime auto loans marks a defining moment in the U.S. credit landscape. It reflects a combination of higher vehicle prices, rising debt levels, and a segment of borrowers facing heightened financial pressures. While prime and general auto loan delinquency rates remain comparatively contained, the subprime cohort’s trajectory offers a warning about tail risks in consumer credit markets.

As lenders recalibrate risk management and borrowers reassess their financial plans, the auto finance ecosystem will continue to adapt to evolving economic conditions. The interplay between household budgets, vehicle costs, and access to affordable credit will shape the near-term trajectory of auto debt, with regional dynamics adding texture to a national story that touches millions of households and communities across the country.