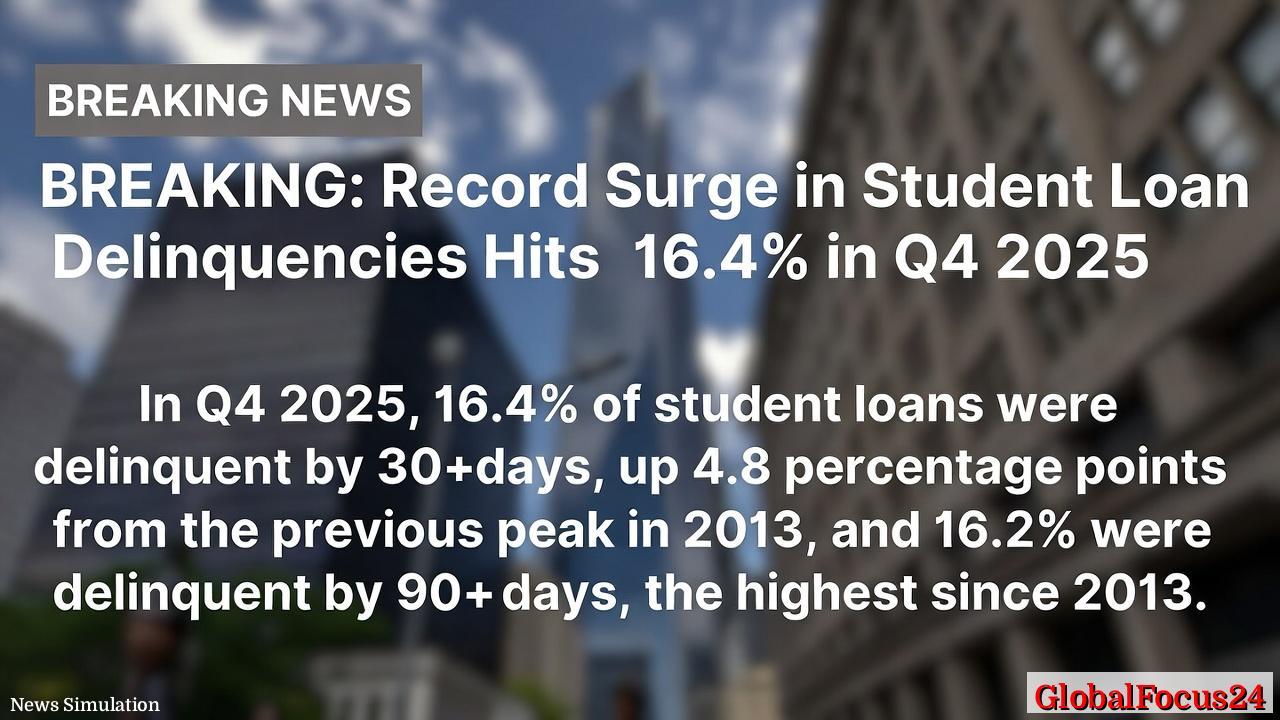

Record Surge in Student Loan Delinquencies Hits 16.4% in Q4 2025

The student loan landscape in the United States has reached a critical turning point. In the final quarter of 2025, a record 16.4% of student loans transitioned into delinquency of 30 days or more — a figure that surpasses the previous high from 2013 by 4.8 percentage points. Even more alarming, serious delinquencies — defined as loans overdue by 90 days or more — surged to 16.2%, more than double the rate observed at the beginning of 2025. These developments mark one of the sharpest deteriorations in repayment trends in over a decade, underscoring deep and growing financial stress among borrowers nationwide.

End of Relief Spurs Payment Shock

The abrupt end of the federal student loan relief program in late 2024 marked a turning point for millions of borrowers. The government’s pandemic-era suspension of loan payments and interest accumulation had provided breathing room for more than 43 million Americans, many of whom had not made a payment since early 2020. When repayment obligations resumed in October 2024, borrowers were immediately confronted with higher monthly payments due to accumulated interest and inflation-adjusted budgets that had not kept pace with rising living costs.

Within a few months of the restart, missed payments began to show up on credit reports. By the end of 2025, 9.6% of all student loans were classified as seriously delinquent — the second-highest percentage recorded since the first quarter of 2020. Analysts say this portfolio stress reflects not only the resumption of payments but also broader economic headwinds that have squeezed household budgets.

Inflation, Job Market, and Borrower Strain

The surge in delinquencies cannot be attributed solely to the resumption of repayments. Inflationary pressures that persisted through 2025 eroded disposable income, while wage growth, though steady, failed to fully offset rising costs of housing, transportation, and healthcare. As a result, many borrowers prioritized essential expenses over loan obligations.

Labor market dynamics added further strain. Whileunemployment remained relatively low — hovering between 3.8% and 4.2% nationally — underemployment increased in key urban centers, particularly among recent graduates. Entry-level job openings in technology, marketing, and education contracted in the latter half of 2025, leaving many degree-holders in temporary or part-time positions that offered limited income stability.

This imbalance between debt burdens and income opportunities has intensified the student loan crisis, exposing the vulnerability of borrowers whose financial health depends heavily on consistent employment and wage gains.

Historical Context: Lessons From 2013

The current delinquency spike evokes memories of the early 2010s, when student loan defaults climbed in the aftermath of the Great Recession. In 2013, the delinquency rate peaked at 11.6%, alarming policymakers and prompting the expansion of income-driven repayment programs designed to prevent defaults among low-income borrowers. Those measures helped stabilize the trend by mid-decade.

However, the 2025 surge surpasses even that crisis-level threshold, pointing to a more entrenched structural challenge. The average borrower today faces higher debt loads — approximately $38,000 per borrower compared with $27,000 in 2013 — as tuition costs have far outpaced inflation. Moreover, an increasing share of borrowers hold graduate or professional degrees, often carrying loan balances exceeding $70,000. These factors heighten repayment risk when economic conditions tighten.

Regional Disparities Across the U.S.

Delinquency trends vary widely across regions. States in the South and Midwest have shown the steepest increases, with Mississippi, Georgia, and Ohio experiencing delinquency rates above 18%. These states tend to have lower median incomes and higher concentrations of borrowers who attended for-profit institutions, where graduation rates are lower and post-graduation earnings often fail to justify the debt incurred.

In contrast, some Northeastern states — including Massachusetts and New York — have fared somewhat better, with delinquency rates closer to 12%. Analysts attribute this to stronger local job markets, higher average wages, and greater participation in income-driven repayment plans.

The Western region presents a mixed picture. California and Washington maintain moderate delinquency levels, yet rural areas and smaller college towns in these states are showing sharp upticks, reflecting uneven recovery patterns and housing affordability crises that continue to burden young professionals.

Borrower Demographics and Risk Concentration

Recent data suggest that younger borrowers and those with smaller loan balances are disproportionately affected by delinquency spikes. This counterintuitive trend reflects the precarious financial standing of borrowers who did not complete their degree programs but still owe thousands in debt. Without the income boost typically associated with a college credential, these individuals struggle to keep up with payments even on modest loans.

Conversely, graduate borrowers with six-figure debt loads are less likely to fall immediately into delinquency but face longer-term repayment challenges. Economists warn that while these borrowers may be able to defer payments through income-based plans or public service programs, their debt-to-income ratios could remain elevated for decades, constraining their ability to buy homes, start businesses, or save for retirement.

Economic Impact and Broader Implications

The ripple effects of rising delinquencies extend beyond individual borrowers. Analysts project that the increase will dampen consumer spending in early 2026, as households redirect funds toward overdue balances or deal with damaged credit histories. Credit access may tighten for younger consumers, particularly in the mortgage and auto loan markets, where lenders factor student loan performance into risk assessments.

In the financial sector, private lenders and servicers that manage federally guaranteed loans face operational and reputational challenges. Higher delinquency rates increase servicing costs, while collection efforts often trigger public backlash and political scrutiny. For the broader U.S. economy, prolonged repayment struggles may hinder long-term growth by delaying key life milestones such as homeownership and family formation.

From a macroeconomic perspective, the student loan market — valued at roughly $1.75 trillion — represents one of the largest consumer debt categories, second only to mortgages. A sustained deterioration in credit quality could influence monetary policy discussions, especially if delinquency-driven credit tightening affects aggregate demand in the coming quarters.

Policy Responses and Relief Options

In response to mounting distress, policymakers have revisited potential administrative measures, including revisions to income-driven repayment (IDR) programs and restoration of limited hardship deferments. The Saving on a Valuable Education (SAVE) plan, introduced in 2023, lowered monthly payments for many borrowers but has yet to reach full enrollment due to administrative delays and lack of awareness.

Experts suggest that targeted outreach — particularly to vulnerable borrowers in default or near-default status — could prevent millions from entering long-term delinquency. However, systemic solutions may require congressional action, such as expanding Pell Grant funding or revisiting bankruptcy restrictions that make student debt virtually non-dischargeable.

Financial counselors emphasize proactive engagement as a crucial step. Borrowers facing difficulty are encouraged to contact loan servicers early to explore IDR options or temporary payment waivers rather than allowing accounts to lapse into default.

Historical Evolution of Relief and Responsibility

Over the past half-century, the student loan system has undergone multiple transformations, from government-backed guarantees in the 1960s to the direct lending model adopted in the 1990s. Each reform sought to expand access to higher education, but affordability has remained elusive. Between 1980 and 2025, average tuition and fees at public four-year institutions more than tripled in inflation-adjusted dollars, while wage growth lagged behind.

Efforts to balance access, affordability, and fiscal responsibility continue to shape U.S. education policy. The current delinquency wave underscores an enduring tension: while education remains a key driver of social mobility, the financial mechanisms supporting it have become increasingly burdensome for middle- and lower-income families.

Public Reaction and Outlook for 2026

Public concern has intensified as borrowers share stories of struggling to meet obligations despite full-time employment. Online forums, student advocacy groups, and nonprofit organizations report surging inquiries from individuals seeking debt counseling or forgiveness guidance. The issue has gained renewed national attention, particularly as the delinquency rate approaches levels unseen since before the pandemic.

Looking ahead, financial experts expect continued volatility through mid-2026. Unless wage growth accelerates or new relief mechanisms are implemented, delinquency rates may remain elevated throughout the year. By some estimates, serious delinquencies could reach 10% of all outstanding student loans by midyear, nearing historically high thresholds.

While the long-term benefits of higher education remain evident, the current data raise fundamental questions about sustainability in the nation’s lending model. As repayment burdens reshape household finances and influence broader economic trends, the student loan system stands at a crossroads — one that will test the resilience of both borrowers and institutions in the years ahead.