)

SOFR-Federal Funds Spread Trading Surges as Markets Price Shift in U.S. Funding Landscape

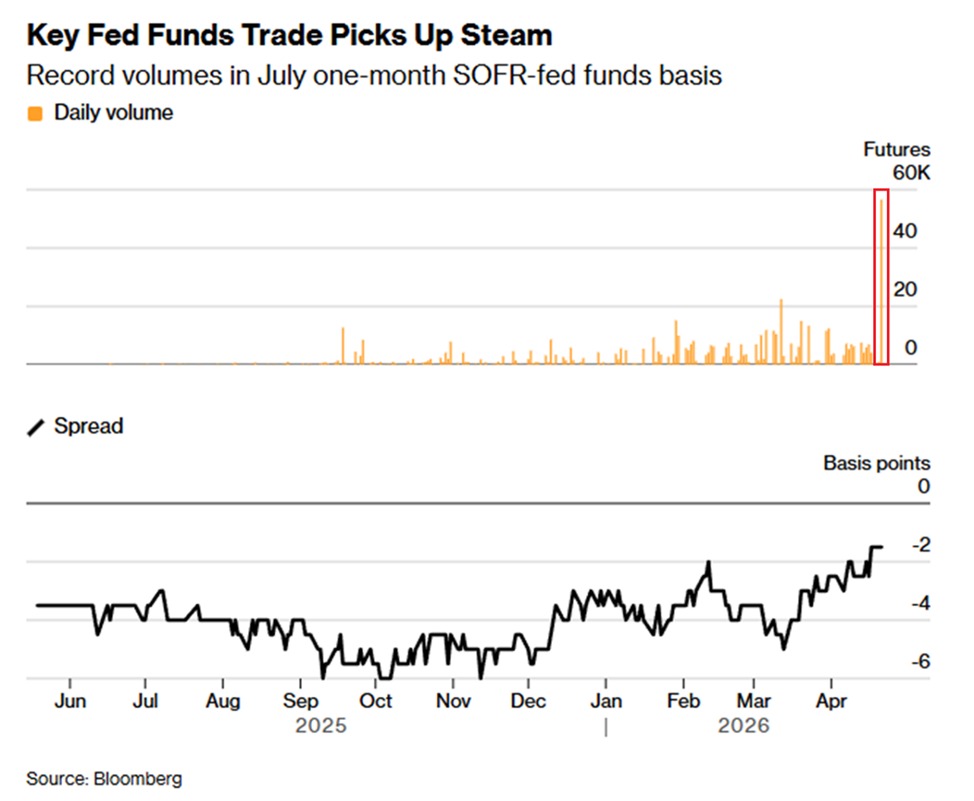

In a striking display of how quickly financial markets can reprice the plumbing of the U.S. money system, traders moved aggressively into futures tied to the spread between the Secured Overnight Financing Rate (SOFR) and the Federal Funds Rate last Tuesday. The daily trading volume for these futures climbed to a record 56,590 contracts, signaling a broad reassessment of risk, liquidity, and policy expectations as market participants anticipate a potential structural shift in U.S. funding markets.

Historical context: the evolution of benchmark rates and market signaling SOFR emerged as a dominant benchmark in the wake of the 2008 financial crisis, replacing a suite of older indicators that relied on unsecured lending. It reflects the cost of borrowing cash overnight collateralized by U.S. Treasuries, making it a more robust measure of the actual funding costs faced by primary dealers, banks, and money-market funds. The Federal Funds Rate, set by the Federal Reserve, represents the target interest rate at which banks lend reserves to one another overnight. The spread between the two rates has long been watched as a barometer of systemic liquidity and the friction between secured and unsecured funding channels.

Over the past decade, market participants have increasingly treated the SOFR-Federal Funds spread as a microcosm of short-term funding conditions. When the spread widens, it can indicate stress in unsecured funding markets or shifts in collateral demand. Conversely, a tightening spread can reflect ample liquidity and a reduced premium for secured finance. Traders in futures tied to this spread have used the instrument to express views on liquidity dynamics, central-bank policy expectations, and the evolving structure of wholesale funding.

Economic impact: implications for banks, money-market funds, and borrowers A sustained increase in demand for SOFR-Federal Funds spread futures points to several tangible consequences across the financial system. First, banks may adjust their balance-sheet strategies to optimize funding costs. A wider spread can incentivize banks to favor secured funding channels, such as repurchase agreements or secured overnight financing, over unsecured interbank lending. This tilts the liquidity calculus toward assets that are backed by collateral, potentially influencing the pricing of short-term credits and the availability of funding for corporate borrowers and municipalities.

Second, money-market funds—collectors of cash balances and primary purchasers of short-term securities—watch the spread closely as a proxy for risk, liquidity, and the attractiveness of different instruments. A larger spread often signals heightened demand for secured funding tools or a conservative stance toward liquidity risk, which can lead to changes in fund flows, yield spreads, and the composition of assets held by these funds. The net effect can influence the broader operating environment for short-duration debt, commercial paper, and other income-generating instruments used by corporations to manage working capital.

Third, borrowers—ranging from small businesses to multinational corporations—could feel the indirect effects through the cost of liquidity in the short end of the curve. If lenders price secured funding more aggressively, corporate financing terms may tighten for those reliant on short-term liquidity, particularly in environments where capital markets are volatile and funding at favorable rates becomes more selective. The ripple effects can extend to project timelines, capital expenditure plans, and the discipline with which firms manage cash buffers.

Regional comparisons: how U.S. funding dynamics stack up against international benchmarks The SOFR-Federal Funds spread sits within a global ecosystem of comparable benchmarks that govern liquidity and financial stability in other major economies. In Europe, for instance, markets monitor the euro short-term rate and related spreads to gauge cross-border funding conditions and the potential spillovers from euro-area monetary policy. In Asia, liquidity dynamics are influenced by a mix of domestic policy signals and global demand for U.S. dollar funding, particularly through the currency swap facilities and offshore funding markets.

Historically, shifts in U.S. funding conditions often have knock-on effects abroad, given the dollar’s role as a global reserve currency and the interconnectedness of global banks’ funding strategies. A surge in demand for secured funding in the United States can influence global dollar liquidity, affecting cross-border lending, trade finance, and the cost of dollar-denominated short-term instruments used by non-U.S. institutions. Conversely, synchronized trends in major markets can amplify volatility and prompt coordinated policy commentary from central banks and financial regulators.

Market structure and participants: who is trading the spread futures and why The surge in futures volume indicates participation from a broad cohort of market players seeking to hedge, speculate, or gain directional exposure to funding costs. Banks and broker-dealers monitor the spread as a proxy for liquidity risk and to adjust collateral management practices. Asset managers and hedge funds may use the instruments to express views on the trajectory of monetary policy and the evolving balance sheet strategies of major financial institutions. Proprietary trading groups and arbitrage desks also engage with the spread futures to capitalize on mispricings between secured funding markets, the Fed’s policy stance, and related money-market instruments.

As central banks communicate policy directions, the interpretation of the SOFR-Federal Funds spread becomes a window into expectations about future rate paths, balance-sheet normalization, and the resilience of money markets under stress scenarios. A rapid shift in the spread’s trajectory can prompt market participants to recalibrate risk models, adjust hedging programs, and reallocate capital across short-term instruments.

Regulatory and risk considerations: overseeing a critical funding channel Regulators have long emphasized the resilience and transparency of short-term funding markets. The adoption of SOFR as the preferred benchmark was part of a broader reform to reduce reliance on less transparent, interbank-offered rates. Ongoing oversight focuses on ensuring liquidity access, robust clearing and settlement infrastructure, and the proper functioning of collateral markets. The recent surge in futures trading on the SOFR-Federal Funds spread underscores the importance of monitoring for systemic risk, liquidity shortfalls, and potential spillovers into other segments of the financial system.

Market participants should also consider the interplay between monetary policy signaling and market-based expectations. While the Fed’s policy stance provides a essential anchor, funding markets can exhibit dislocations when rate expectations shift in ways that outpace policy communications. In such cases, the futures market serves as a barometer of collective judgments about liquidity risk, funding costs, and the timing of policy adjustments.

Public reaction and the psychology of volatility A record level of futures activity around the SOFR-Federal Funds spread can evoke a range of responses across the public and professional spheres. Businesses watching their financing costs, students of macroeconomics, and ordinary savers may interpret heightened spread volatility as a sign of ongoing adjustment in the post-pandemic financial landscape. Newsrooms and analysts track the health of short-term funding markets as an indicator of overall financial stability, which can influence consumer confidence and corporate investment plans.

Yet the market’s fast tempo can also provoke caution among participants who are sensitive to abrupt shifts in liquidity conditions. Financial institutions may exercise vigilance in managing collateral, liquidity buffers, and contingency funding plans to avoid being caught off guard by sudden dislocations that could affect day-to-day operations and the ability to meet obligations.

Technical underpinnings: how the spread futures are constructed and traded The SOFR-Federal Funds spread futures are designed to capture movements in the difference between secured overnight funding costs and the central-bank policy rate. Traders typically rely on a combination of macroeconomic data, central-bank commentary, and funding-market indicators to form views about where the spread is headed. Liquidity in the futures market can be influenced by the breadth of participants, the availability of hedging instruments, and the relative attractiveness of margin requirements and funding costs across venues.

Operationally, the price discovery process in these futures reflects the tug-of-war between perceived policy paths and the evolving supply-demand balance for secured funding instruments. When liquidity tightens, or when risk premia rise, futures prices can exhibit sharper moves as participants adjust expectations for the near-term path of short-term rates and collateral costs.

Looking ahead: what to watch as funding markets adapt

- Policy signals: Market participants will closely parse the next rounds of Fed communications for any shifts in language about balance-sheet normalization and the trajectory of the federal funds rate. Small changes in tone or guidance can have outsized effects on funding-cost expectations.

- Liquidity metrics: Ongoing monitoring of one-day and longer-horizon liquidity indicators will help gauge whether the surge in SOFR-Federal Funds spread trading reflects enduring structural changes or a temporary recalibration.

- Cross-market spillovers: Investors will watch for correlations with other funding- and risk-sensitive assets, including unsecured interbank markets, repurchase agreements, and money-market fund flows, to understand how funding dynamics feed into broader asset prices.

- Regional developments: Given the interconnectedness of global funding, regional benchmarks and policy signals from major economies can inform how U.S. funding conditions interact with international markets.

Conclusion: a milestone in funding-market evolution The record activity in futures tied to the SOFR-Federal Funds spread marks a notable moment in the ongoing evolution of U.S. funding markets. It reflects a confluence of shifting liquidity conditions, policy expectations, and the strategic recalibration of institutions that rely on short-term funding. As the financial system continues to adapt to a post-crisis regulatory framework and a changing macroeconomic landscape, the spread between secured and unsecured funding will remain a key barometer of resilience and risk. Market observers will stay attentive to how these dynamics unfold, seeking to understand whether the current signals herald a new baseline for short-term funding costs or a temporary phase of adjustment as institutions rebuild and recalibrate their funding strategies in a shifting economic environment.