Office CMBS Delinquency Rate Hits Record High in January

A sharp January uptick in office-focused commercial mortgage-backed securities (CMBS) delinquency rates has set a new benchmark, signaling intensified distress across commercial real estate finance and prompting broader questions about the sector’s resilience in a shifting macroeconomic environment. The data, which tracks overdue loan payments on CMBS collateral tied to office properties, shows a pronounced deterioration that extends beyond isolated pockets of vulnerability, reflecting a confluence of elevated borrowing costs, shifting workplace patterns, and tighter credit conditions that have unfolded over the past three years.

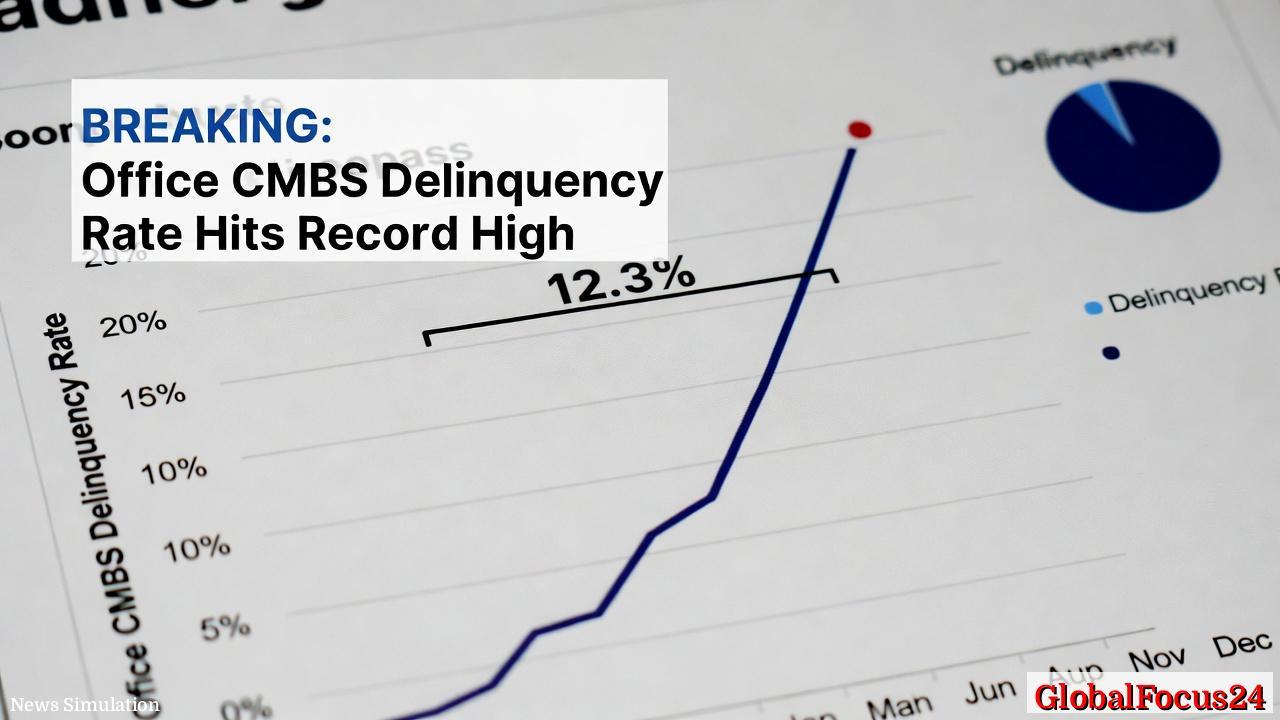

Historical context: cycles, leverage, and the office market The office real estate sector has weathered multiple cycles in the modern era, but the latest data illuminate a stark shift in risk dynamics for CMBS holders. Delinquency rates on office-property CMBS climbed by 103 basis points in January alone, bringing the national office CMBS delinquency rate to 12.3 percent. This figure surpasses the peak reached during the 2008 financial crisis by 1.6 percentage points, underscoring the severity of the current stress. To understand the magnitude, it helps to recall that the 2008 crisis was defined by broad, system-wide mortgage distress that reverberated through commercial real estate for years. The January jump suggests a more rapid accumulation of distress signals in the contemporary cycle, with debt tenors and loan-to-value structures tightening under conditions of higher interest rates and slower rent growth in many markets.

The broader CMBS landscape also reflects a widening mix of pressures. The overall U.S. CMBS delinquency rate rose to 7.5 percent in January, the highest in at least five years. Multifamily property loans, traditionally a counterweight to office volatility due to secular demand and resilient rent growth in many markets, saw delinquencies rise as well, with a 30-basis-point increase to 6.9 percent—the third-highest level since December 2015. The divergence between office and multifamily risk profiles within CMBS portfolios highlights how sector-specific headwinds—such as commuting patterns, hybrid work models, and evolving demand for urban vs. suburban space—translate into distinct credit outcomes.

Economic impact: balance sheets, credit markets, and capital allocation The January delinquency deterioration carries multiple economic implications for lenders, borrowers, and the broader financial system. First, rising delinquencies compress the income streams that CMBS servicers rely on to fund operations, manage special servicers, and maintain lien positions. As more loans slip into special servicing, trustee and master servicer costs rise, potentially diverting resources from proactive loan workouts to administrative management. This dynamic can escalate costs for the overall securitized vehicle and, by extension, for investors seeking predictable cash flows.

Second, heightened delinquency rates tighten new loan credit availability for office properties. Banks and nonbank lenders have increasingly priced risk, with higher spreads and stricter covenants affecting acquisition and refinancing activity. For developers and property owners, the cost of capital has moved higher just as the office market contends with structural changes in space utilization. The result can be slower transaction activity, delayed redevelopment projects, and a more cautious approach to portfolio management across major metropolitan regions.

Third, local and national employment patterns are intertwined with the performance of office-backed CMBS. The demand for office space is linked to corporate hiring trends, business travel, and the cadence of in-person collaboration. When employment growth slows or employee attendance remains uneven, demand for premium-grade office space may not rebound as quickly as rent expectations assume. The current data point to a landscape where some office segments may adjust to leaner footprints, while others—particularly high-quality properties in key city centers—could experience more resilient demand if market fundamentals shift in a favorable direction.

Regional comparisons: pockets of stability amid widespread stress While January’s national figures paint a picture of rising distress, regional metrics reveal a more nuanced story. Some markets exhibit more pronounced vulnerability due to local economic cycles, supply growth, and competitive alternatives to urban office space. In several gateway and tech-centric metros, office fundamentals have faced higher vacancy pressures, as firms adopt hybrid models that reduce the need for sprawling downtown footprints. Yet, other regions with robust employment hubs, live-work-play ecosystems, and limited new supply may display more durable rent dynamics and lower credit risk within CMBS portfolios.

For investors and lenders, regional analysis remains essential. Markets with diversified employment bases, strong wage growth, and less aggressive development pipelines can mitigate some of the credit stress observed in aggregated data. Conversely, markets with elevated retail exposure, weaker income growth, or high construction completions relative to lease activity may see delinquency trajectories worsen more quickly. The next several quarters will likely reveal how regional policy responses, infrastructure investment, and sectoral shifts—such as logistics and data centers within mixed-use developments—interact with office debt performance.

Structural factors shaping risk Several structural factors have converged to influence CMBS performance in the office sector. First, higher interest rates implemented by central banks to combat inflation have raised borrowing costs for property owners and developers. This affects debt service coverage ratios and loan refinancing feasibility, particularly for properties that saw rent growth stall or slow after the post-pandemic recovery period. Second, evolving workplace norms—such as flexible schedules and reduced in-office days—have rebalanced demand for traditional office space. While some firms continue to occupy space at pre-pandemic levels, others have optimized footprints, leading to rental stagnation or selective rent concessions in certain submarkets. Third, construction costs and permitting timelines have added to capex planning uncertainty, influencing the pace and structure of new office developments and the likelihood of loan-to-value adjustments that can trigger cross-default risk for CMBS borrowers.

Market signals and borrower profiles Credit quality within office CMBS portfolios varies by borrower type, property class, and geographic concentration. Higher-quality, core properties in prime markets often benefit from stronger sponsor track records and long-term leases, which can cushion distress to some degree. Yet, even these cohorts face challenges as debt maturity schedules converge with elevated cap rates and tighter underwriting standards. Value-add properties—those undergoing capital improvements to lift occupancy and rent—may experience higher sensitivity to cost overruns and occupancy timing, potentially increasing delinquency risk if projected cash flows fail to materialize.

In the multifamily space, the resilience of rental income and the relative defensive nature of housing assets have historically tempered the severity of delinquencies in CMBS backed by apartment properties. The January uptick to 6.9 percent for multifamily CMBS remains notable, though still below the office distress levels. Investors in this segment often watch occupancy trends, rent growth, and local economic conditions closely, given that strong multifamily performance can serve as a stabilizer within a diversified CMBS portfolio.

Policy context and macro considerations Policy landscapes at federal and local levels influence the broader credit environment for CMBS. Central bank actions to manage inflation and steer economic growth have a direct bearing on loan pricing, debt service requirements, and the appetite of lenders to extend credit for office properties. Additionally, regional policy priorities—such as incentives for urban redevelopment, transportation access, and zoning reforms—can affect office demand conditions and the attractiveness of certain submarkets. While policy considerations are unlikely to single-handedly reverse delinquency trends in the near term, they contribute to the backdrop against which market participants evaluate risk and allocate capital.

Public reaction and market sentiment Market participants, including property developers, lenders, and institutional investors, have responded to January’s data with caution and deliberate risk management. Some observers emphasize resilience factors—high-quality assets, diversified tenant rosters, and long-term leases—that can dampen the pace of distress. Others highlight the potential for a protracted period of higher capitalization rates and slower leasing activity if job growth slows or office demand remains structurally constrained. Public sentiment around urban office markets remains mixed, with renewed interest in amenity-rich, transit-accessible properties that promise productivity gains for tenants, even as occupancy patterns continue to evolve.

Outlook: what to watch in the coming quarters The trajectory of CMBS delinquencies in the office sector will hinge on several interrelated dynamics. Key factors to monitor include: the pace of economic growth and employment gains, job creation by sector, and the health of large corporate balance sheets that drive leasing decisions; the evolution of interest rates and debt prices, which influence refinancing windows and capex plans; and the development pipeline in major markets, including supply growth in central business districts versus suburban submarkets. If rent growth resumes in selective submarkets and leasing velocity improves, some office properties could stabilize, particularly those with strong sponsorship and solid credit metrics. Conversely, sustained high debt costs, weak rent growth, or a mismatch between maturing debt and cash flow could propel further delinquencies across CMBS-backed office loans.

Conclusion: a complex landscape requiring careful risk assessment January’s record-high office CMBS delinquency rate underscores a period of heightened credit risk within the commercial real estate finance sector. While multifamily delinquency rates show resilience relative to office properties, the broader CMBS market is navigating a blend of higher financing costs, evolving occupancy trends, and regional differences in demand. For lenders, investors, and policymakers, the priority remains a careful assessment of balance sheets, cash flow projections, and refinancing options across time horizons. The data highlight the necessity of disciplined underwriting, diversified portfolios, and proactive workout strategies to manage risk as the market seeks a path toward greater stability in the quarters ahead.