Paper Losses on Japanese Bonds Expand at Life Insurers

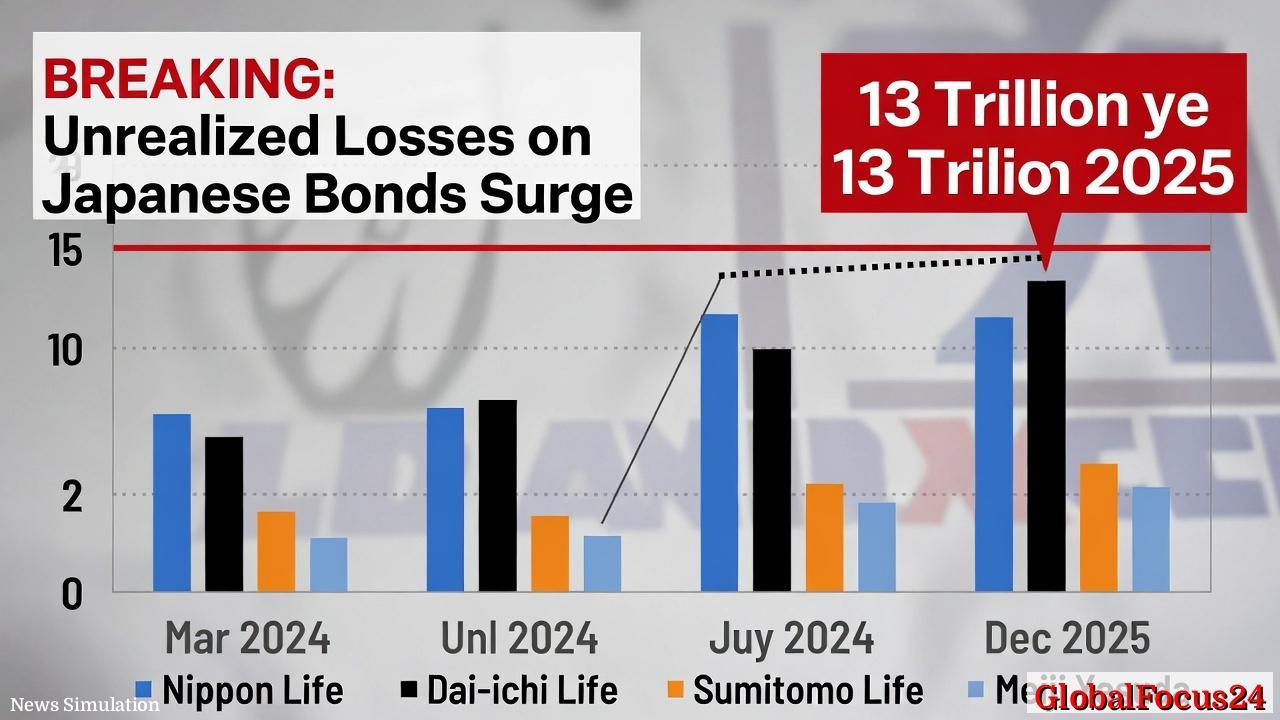

Japan’s major life insurers are confronting unprecedented paper losses on their vast bond portfolios, underscoring the deep strains that rising interest rates have inflicted on the country’s financial sector. According to recent company filings, unrealized losses on Japanese government bonds held by the nation’s four largest insurers—Nippon Life, Dai-ichi Life, Sumitomo Life, and Meiji Yasuda—swelled to 13.2 trillion yen ($86 billion) by the end of 2025.

The figure marks a 125% surge year-over-year and a staggering 546% increase since early 2024, reflecting the steep decline in domestic bond prices as yields climbed from historic lows. While the losses remain “unrealized,” meaning they have not yet been crystallized through sales, the scale of the deterioration reveals how vulnerable insurance balance sheets have become in Japan’s shifting interest rate environment.

Rising Yields Erode Decades of Stability

For decades, Japanese life insurers benefited from an era of ultra-low interest rates and stable bond valuations, aligning with the Bank of Japan’s long-running commitment to monetary easing. That environment began to change dramatically in 2023 when the central bank started allowing longer-term yields to rise more freely, seeking to normalize policy after years of yield curve control.

As 10-year Japanese government bond (JGB) yields edged closer to 1.2% by late 2025—up from near zero just two years earlier—the resulting price declines inflicted sharp valuation losses on insurers’ vast bond holdings. The life insurance sector, which traditionally invests heavily in long-dated government paper to match its long-term policy liabilities, has been especially exposed.

Nippon Life Insurance Co., the largest in the group, recorded the largest individual unrealized loss at approximately $36 billion, a 115% increase from a year earlier. Dai-ichi Life, Sumitomo Life, and Meiji Yasuda each reported significant additional losses that collectively pushed the total beyond the 13-trillion-yen threshold, the highest on record for Japan’s life industry.

The Mechanics of Paper Losses

Unrealized or “paper” losses arise when the market value of a security falls below its purchase price but has not yet been sold. For insurers with long-term investment horizons, these valuation swings are typically tolerated as temporary fluctuations. However, the scale seen in recent quarters has raised concerns among analysts and credit agencies, particularly as higher yields challenge the industry’s capital buffers.

Life insurers must maintain substantial reserves to guarantee payouts to policyholders—products that were often priced when yields were significantly lower. Rising interest rates help raise returns on new investments but simultaneously lower the value of legacy bond portfolios. The mismatch between old and new portfolios has complicated balance sheet management, especially when combined with regulatory capital requirements.

A senior Tokyo-based market strategist described the situation as “a collision between the legacy of yield curve control and the dawn of a higher-rate regime.” The concern, the strategist added, is not only about paper losses today but about whether insurers will need to realize them to rebalance their holdings toward higher-yielding securities.

Historical Context: From Stability to Volatility

For much of the past three decades, Japanese government bonds were considered a safe and even dull investment—a cornerstone of the country’s conservative financial system. Insurers, which oversee trillions in household savings, relied on these instruments to ensure steady, predictable returns.

The environment began to shift in 2022 when international inflation pressures and a weakening yen prompted markets to test the limits of the Bank of Japan’s yield targets. Subsequent policy tweaks opened the door for greater yield volatility. As yields climbed, the market value of previously issued low-coupon bonds began to slide, eroding insurers’ unrealized gains accumulated during the long period of monetary stability.

By 2025, the rapid pace of adjustment had exposed how dependent the sector had been on stable yields. The 13.2 trillion yen in combined unrealized losses dwarfs previous records, signifying one of the steepest value adjustments the industry has ever faced.

Economic Implications

Although the losses are not realized, their implications extend across Japan’s broader financial ecosystem. Insurers are key investors in both government and corporate debt. If rising losses constrain their investment capacity, it could ripple into credit markets and, potentially, government financing conditions.

A diminished appetite for JGBs by life insurers could compel the Ministry of Finance to seek a broader investor base or offer higher yields to attract demand. That shift would mark a historic turn for Japan, where domestic financial institutions have long absorbed the bulk of government debt issuance at ultra-low rates.

The impact might also influence corporate funding costs. Life insurers are traditionally significant buyers of corporate bonds and loans. Less available capital from these buyers could push firms toward higher-cost financing options, potentially slowing investment and economic growth.

However, not all effects are negative. The gradual normalization of yields also boosts the potential income that insurers can earn on new bond purchases. While older holdings suffer valuation hits, newly acquired securities promise better returns over time. Many analysts consider this stage a painful but necessary transition toward a more balanced yield environment.

Comparison With Global Trends

Japan is not alone in feeling the pressure from surging bond yields. Across major economies, insurers and pension funds have endured similar valuation declines as central banks raised rates to combat inflation. U.S. insurers, for example, saw steep unrealized bond losses in 2023 and 2024 when Treasury yields spiked. European insurers faced comparable strains as bond prices dropped after rate hikes by the European Central Bank.

What distinguishes Japan, however, is the speed of change after decades of yield suppression. The shift from nearly zero rates to more market-driven levels occurred within just a few quarters, leaving institutions little time to reposition portfolios. Additionally, Japan’s insurers operate under unique liabilities—many of their policy contracts were written decades ago under assumptions of near-zero or even negative interest rates—making adjustment more complex.

Regional analysts note that while insurers in the U.S. and Europe can offset valuation losses more quickly through higher reinvestment returns, Japan’s demographic and policy environment makes recovery slower. With aging policyholders drawing down savings and fewer new policy subscriptions, life insurers have limited flexibility to reallocate assets rapidly.

How Insurers Are Responding

In response to mounting losses, major insurers have stepped up efforts to diversify their investment portfolios. Some have increased allocations to foreign bonds, real estate, and alternative assets such as infrastructure projects and private credit. Others have shortened bond maturities to reduce sensitivity to rate swings.

Nippon Life has reportedly expanded overseas investments, taking advantage of higher interest rate differentials abroad, though currency hedging costs remain a limiting factor. Dai-ichi Life has engaged in more derivatives-based hedging, seeking to manage exposure without significantly altering portfolio composition.

Executives at several firms have emphasized their ability to hold bonds to maturity, thereby avoiding the need to realize losses. “Our long-term view remains unchanged—we match our investments with long-term liabilities,” one insurer’s spokesperson commented during recent earnings briefings. Nonetheless, even unrealized losses can affect solvency metrics that regulators and rating agencies closely monitor, influencing dividend policies and capital planning.

Outlook for 2026 and Beyond

Market observers expect bond valuations to remain volatile into 2026 as the Bank of Japan continues to calibrate its monetary stance. While inflation pressures appear to have moderated, policymakers face the challenge of fostering growth without reigniting price instability.

If yields stabilize near current levels, insurers may see a modest recovery in market valuations, particularly if coupon reinvestment at higher rates begins to offset paper losses. However, a further uptick in yields would deepen losses and potentially force some firms to reassess their asset-liability management strategies.

Japan’s Financial Services Agency is reportedly monitoring the situation closely but has not indicated immediate concern about systemic risks. Most insurers remain well-capitalized, with strong solvency margins after years of conservative risk management. Yet, analysts caution that the current episode is a stress test for a financial sector long accustomed to an unchanging rate environment.

A Turning Point for Japan’s Financial Future

The surge in unrealized bond losses among Japan’s life insurers may ultimately mark a turning point in the nation’s financial history. After decades of stability built on low yields and predictable returns, the sector is confronting a new reality—one in which volatility, rather than stability, defines the investment landscape.

How well insurers adapt to that reality will shape the resilience of Japan’s broader financial system. The transformation underway is as much about mindset as markets: moving from a tradition of passive bond accumulation to a more dynamic, globally integrated investment approach.

As the numbers from 2025 reveal, Japan’s insurers now stand at the front line of a structural shift—one that will test the durability of their strategies, the patience of their policyholders, and the adaptability of a system that anchored decades of economic calm. The 13.2 trillion yen in paper losses, while daunting, may ultimately serve as the price of transition to a more sustainable era of interest rate normalization.