Inflation Surges: December PCE Data Highlights Shifting Economic Momentum

December inflation readings for the United States, as measured by the Personal Consumption Expenditures (PCE) price index, showed a notable shift from the recent easing trend, with thePCE and the core PCE both underscoring persistent price pressures. The latest data indicate broader inflationary momentum that could influence policy considerations at the Federal Reserve and alter the financial outlook for households, businesses, and regional economies across the country.

Historical context: tracing the inflation trajectory

- The PCE price index, favored by the Federal Reserve for its comprehensive view of household spending and price changes, has been the focal point of inflation analysis for much of the past decade. After years of volatile swings surrounding the pandemic, the inflation narrative oscillated between periods of moderation and renewed upward pressure as demand rebounded, supply chains adjusted, and labor markets tightened.

- December’s reading arrives after a sequence of months in which the inflation rate showed signs of cooling, leading some observers to anticipate a steady deceleration throughout the next year. The latest numbers, however, suggest a renewed momentum that echoes episodes in prior cycles when price pressures re-emerged as demand outpaced supply or as monetary policy lagged changes in the broader economy.

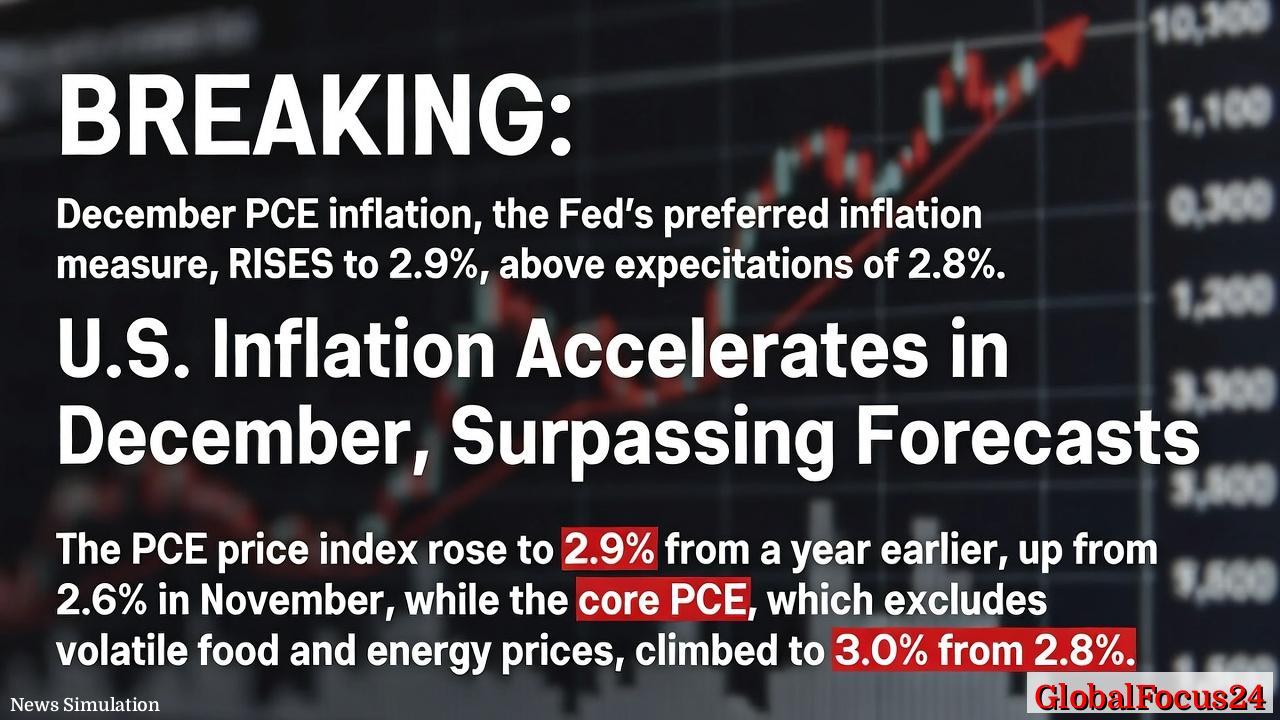

- The distinction between thePCE and the core PCE remains crucial. Core PCE strips out food and energy prices to reflect underlying inflation trends more accurately. The December data show core inflation at its highest level in over a year, underscoring the persistence of price growth in goods and services beyond volatile energy markets.

What the December readings indicate

-PCE inflation rose to 2.9% in December, surpassing economists’ forecasts and signaling that overall price gains still cling to higher levels than target expectations. This movement suggests that consumer price dynamics remain sensitive to a range of factors, including wages, consumer demand, and production costs across sectors.

- Core PCE, which excludes the more volatile food and energy components, increased to 3.0%, the highest since late 2023. This uptick points to ongoing margin pressures in service sectors, durable goods, and other components that feed into household budgets beyond energy price fluctuations.

- Taken together, the December figures imply a potential re-evaluation of near-term monetary policy paths. While the Fed has signaled a cautious approach to policy normalization, the persistence of inflationary momentum could influence discussions about interest rate trajectories, balance sheet management, and the timing of future rate adjustments.

Regional and sectoral implications

- Consumer prices moving higher in December reverberate through regional economies in ways that interact with labor market conditions, housing affordability, and local business sentiment. Regions with higher housing costs or tighter labor markets may experience more pronounced price pressures, which in turn affect consumer confidence and spending patterns.

- Sectors most closely tied to consumer demand—such as retail, hospitality, and discretionary services—face a nuanced outlook. When inflation remains sticky, consumers may reprioritize purchases, delaying big-ticket items or seeking value-driven options, which can influence job stability and investment decisions across metropolitan and rural areas alike.

- Manufacturing and supply chains also feel the impact of sustained price growth. Input costs, shipping, and raw materials can translate into higher prices for final goods, potentially narrowing profit margins and shaping capacity planning for manufacturers across the country. Policymakers and business leaders will watch closely for whether wage growth accelerates in tandem with prices, influencing labor-market dynamics and inflation expectations.

Economic impact and policy considerations

- The December inflation data reinforce the notion that monetary policy needs to balance the risks of letting inflation become more entrenched against the goal of supporting continued growth. Markets will assess whether the uptick in core inflation signals a longer-lasting inflation regime or reflects temporary factors that will ease in coming months.

- For households, the persistence of higher inflation translates into increased living costs and potential adjustments in spending, saving, and debt management. This dynamic has implications for consumer credit markets, mortgage rates, and household balance sheets, particularly for households near the lower end of the income distribution where price sensitivity is highest.

- Businesses, especially small and medium-sized enterprises, will weigh procurement strategies, pricing decisions, and wage expectations in an environment where inflation remains a factor. The December numbers could influence planning related to inventory, capital expenditure, and hiring cycles as firms calibrate to evolving cost structures.

Historical comparisons: regional and global perspectives

- Historically, inflation cycles in the United States have shown episodic increases after periods of relative calm, often influenced by shifts in energy markets, global supply chain developments, and domestic demand surges. When inflation rebounds, regions with diversified economies and strong consumer bases tend to experience more resilient activity, albeit with rising costs that affect real incomes.

- Internationally, many advanced economies have encountered similar dynamics—sticky inflation, evolving central-bank responses, and market expectations adjusting to new policy regimes. The December PCE readings provide a timely data point for comparative analysis, illustrating how U.S. inflation trends align with or diverge from peers in regions such as Europe, Asia-Pacific, and beyond.

- For investors and policymakers, cross-regional comparisons help gauge whether domestic inflation pressures are primarily cyclical or symptomatic of broader structural factors, such as evolving productivity, labor-market tightness, or shifts in global energy pricing.

What to watch next

- Upcoming inflation reports will be instrumental in shaping market expectations and policy guidance. Investors will scrutinize the persistence of core inflation, service-sector price dynamics, and the trajectory of wages to determine if the December uptick represents a new baseline or a temporary fluctuation.

- The Federal Reserve’s communications and any policy adjustments will be closely tied to ongoing data surprises. Market participants will consider scenarios in which policymakers adopt a more cautious stance on rate normalization or, conversely, reaffirm a gradual path toward suitable policy settings that maintain price stability without constraining growth.

- Economic indicators to monitor alongside inflation include unemployment data, labor-force participation, consumer confidence, retail sales, and manufacturing activity. A comprehensive view of these metrics will help analysts interpret whether December’s inflation figure is part of a broader trend or a blip within a complex dynamic.

Public reaction and sentiment

- Public sentiment in the wake of higher-than-expected inflation readings often shifts toward concerns about purchasing power and cost-of-living pressures. Families balancing budgets, renters facing housing costs, and small business owners assessing input costs may respond with tighter household budgets or adjusted spending plans.

- Business communities may respond with renewed emphasis on efficiency, price discipline, and strategic investments aimed at mitigating cost pressures. Public dialogue often centers on the balance between supporting economic growth and maintaining price stability, especially in regions where inflation has a pronounced impact on daily life.

- Financial markets typically respond with heightened sensitivity to inflation data and expectations about monetary policy. Equities, bonds, and currency movements can react to revisions in interest-rate outlooks, inflation risk premia, and investor confidence in the inflation trajectory.

Conclusion

- The December PCE readings underscore a nuanced inflation landscape, whereinflation remains on the higher end of anticipated ranges while underlying price pressures in core components reveal persistent momentum. The numbers highlight the ongoing challenge for policymakers to navigate a path that sustains economic activity without letting inflation entrench itself.

- As regional economies grapple with cost pressures, labor-market dynamics, and shifting consumer behavior, the December data serve as a critical gauge of near-term economic health. Market participants, policymakers, and households alike will monitor the forthcoming data releases to assess whether inflation will ease in the coming months or maintain a steadier presence on the economic horizon.

- In a landscape shaped by evolving monetary policy and global economic currents, the December inflation figures reinforce the importance of vigilant data analysis and balanced decision-making aimed at fostering long-term price stability and sustainable growth.