Global Bond Yields Near Historic Lows: Implications for Investors and Economies

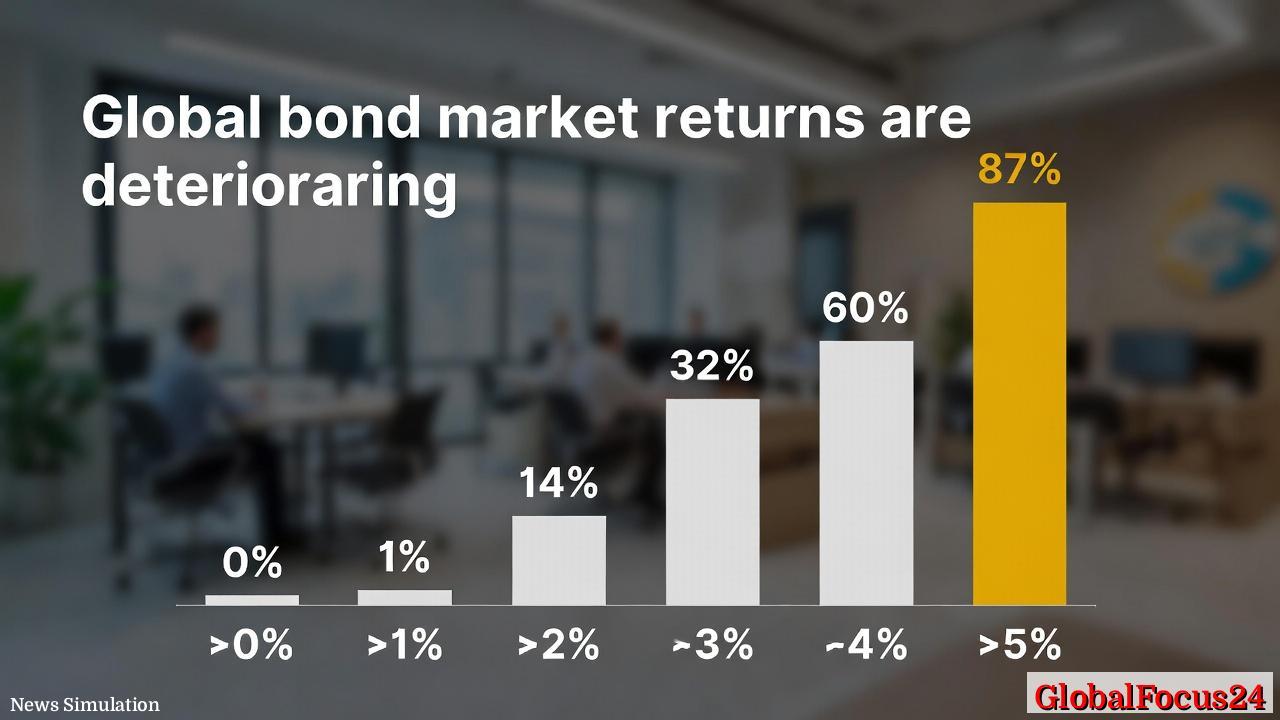

A sweeping majority of the world's debt securities continue to trade at yields below 5 percent, underscoring a persistent environment of ultra-loose monetary policy, persistent demand for income, and the lingering effects of lower-for-longer interest rates. Recent market data illustrate a striking distribution: roughly 87 percent of outstanding bonds yield under 5 percent, with substantial shares below 3 percent and even 1 percent in select segments. This article examines the drivers behind this regime, the potential economic ramifications, and how regional dynamics compare in a globally connected fixed-income landscape.

Historical context: the long arc toward low yields Since the global financial crisis of 2008, central banks around the world implemented aggressive monetary stimulus to revive growth and stabilize markets. The result was a prolonged period of ultra-low policy rates, expansive balance sheets, and search-for-yield behavior among investors. In the subsequent decade, many major economies saw yields on government and corporate debt trend downward, punctuated by episodic volatility during inflation spikes or policy shifts. The last few years have reinforced this pattern: despite pockets of inflation, structural factors such as aging demographics, modest productivity gains, and high demand for safe assets kept benchmark rates anchored at historically low levels in many regions. Against this backdrop, the share of bonds trading with yields under 5 percent has remained remarkably broad, reflecting the ongoing recalibration of risk and return in global markets.

Key drivers shaping current yield distributions

- Central bank policy and inflation dynamics: When policy rates stay low for extended periods, newly issued debt carries lower coupons, and existing securities with higher coupons become more attractive, compressing wider yield spreads. Even as inflation fluctuates, expectations of eventual normalization have often been gradual, supporting a broad base of sub-5 percent yields.

- Global capital flows and demand for income: Fixed-income investors, including pension funds, insurance companies, and sovereign wealth funds, require steady income streams. In many markets, competition for high-quality bonds has pushed prices higher and yields lower, especially for investment-grade credit and government issues.

- Globalization of debt markets: International investors freely move capital across borders, seeking diversification and risk-adjusted returns. This cross-border demand tends to anchor prices and suppress yields in diverse markets, contributing to the prevalence of sub-5 percent yields worldwide.

- Low real yields and risk premia compression: Even when nominal yields are modest, real yields can be negative or near zero on certain maturities or credit qualities. The appetite for downside protection in uncertain times can sustain pricing that supports yields beneath 5 percent across broad segments.

- Growth and earnings expectations: For corporate debt, strong earnings and stable cash flows in many sectors have supported credit quality and reduced default risk, enabling bonds to trade at favorable prices and compressed yields relative to historical standards.

Regional snapshots and comparisons

- United States: As the world’s largest bond market, U.S. Treasuries often set global yield benchmarks. In a climate of cautious optimism about growth and inflation, yield curves have flattened at times, and a large portion of high-quality corporate bonds trades with yields well under 5 percent. The maturity structure matters: longer-dated maturities tend to carry higher yields, but the overall distribution still features a substantial share below 5 percent, reflecting robust demand for duration and quality.

- Eurozone: The European market has been characterized by extended periods of low or negative policy rates, with central banks maintaining accommodative stances to support herding inflation targets and growth. Sub-5 percent yields are common across many German, French, Dutch, and other high-grade issuances, particularly on shorter to intermediate maturities. Corporate credit, including banks and utilities, often exhibits yields aligned with this broad trend, while higher-rated sovereigns attract continued investor interest.

- Asia-Pacific: A broad spectrum exists within Asia. Developed markets such as Japan and parts of Australia may exhibit low or even negative yields in certain durations, while emerging-market debt in the region can show higher yield levels, though still frequently below 5 percent for many investment-grade credits. Currency dynamics and inflation trajectories play a pivotal role in regional yield dispersion.

- Emerging markets: In several emerging economies, higher nominal yields reflect higher inflation risk, currency considerations, and varying political risk. However, even among this group, the appetite for credit quality and diversification has driven many bond issues toward sub-5 percent yields, especially in dollars or other strong currencies where hedging costs are manageable.

Economic impact: what does a sub-5 percent world mean?

- Investment strategies and pension funding: With longer-term yields constrained, institutional investors face challenges in meeting long-term liabilities. Many are compelled to extend duration, search for higher-yielding but still manageable-quality assets, or diversify into non-traditional income sources. This dynamic can influence asset allocation, risk budgets, and funding adequacy metrics.

- Corporate financing and capital structure: Lower yields ease borrowing costs for companies, potentially supporting investment, growth, and refinancing activity. In a climate of subdued yields, firms may pursue buybacks or expansions, contingent on earnings prospects and liquidity conditions. However, if yields remain persistently low and growth falters, the incentive to leverage may wane, and debt management strategies could shift toward balance-sheet optimization rather than expansion.

- Government debt sustainability: While low yields reduce debt service costs in the near term, they also reflect and influence macroeconomic expectations, including growth potential and inflation. In economies with high debt-to-GDP ratios, sustained low yields help stabilize budgets but can complicate longer-term fiscal room if inflation and growth reaccelerate, requiring policy adjustments that may impact the yield landscape.

- Financial sector health: Banks and other lenders benefit from a steeper yield curve and healthier net interest margins. When yields sit under 5 percent across many maturities, profitability hinges on efficiency, fee-based businesses, and risk management. The mix of assets and hedging strategies becomes more critical as the yield environment evolves.

Public reaction and investor sentiment Market participants often describe a sense of cautious optimism tempered by concern for future normalization. Many investors acknowledge the benefits of lower borrowing costs and stable income streams, particularly for long-duration liabilities. At the same time, savers and retirees worry about the erosion of purchasing power and the difficulty of achieving real returns in a sub-5 percent yield world. Wealth managers note that diversification remains essential, with attention to credit quality, duration risk, currency exposure, and macroeconomic indicators that could shift the yield regime.

Historical context within regional markets Looking back over the past two decades, the global yield environment has shifted from episodic spikes in the early 2010s to a more persistent plateau of low-to-moderate yields. The evolution has been shaped by policy experimentation, global trade dynamics, and shifting inflation expectations. Regions with more aggressive macroprudential policies or stronger productivity gains may experience different yield trajectories, but the overarching trend toward broad sub-5 percent yields has held in many developed and select emerging markets.

The role of inflation expectations Inflation remains a central determinant of fixed-income performance. When inflation pressures subside, central banks may signal patience in normalizing policy, reinforcing sub-5 percent yield regimes. Conversely, surprise inflation can compress high-quality bonds momentarily, as investors price in tighter policy and higher short-term rates. The net effect across markets is a balancing act between growth prospects, consumer demand, supply dynamics, and policy signaling.

What to watch next

- Policy guidance and rate trajectories: Market sensitivity to central bank communications cannot be overstated. Any shift toward earlier normalization or more aggressive tightening could lift yields and reshape the distribution across maturities and credit qualities.

- Inflation data and wage trends: Persistent inflation or unexpected wage growth could alter risk assessments and investor appetite for duration or credit risk.

- Global debt issuance patterns: A surge in supply, particularly from sovereigns or highly rated corporates, can influence yields by changing the supply-demand balance in various segments of the market.

- Currency movements: For international investors, currency risk remains a significant factor. Hedging costs and exchange rate volatility can affect the attractiveness of foreign-denominated bonds and, by extension, the yield distribution.

Implications for policy and markets The prevalence of sub-5 percent yields signals a fixed-income market that remains highly sensitive to policy expectations and macroeconomic developments. Policymakers should monitor debt sustainability, financial stability indicators, and the transmission of monetary policy to the real economy. For investors, the current environment underscores the importance of disciplined risk management, diversified sources of income, and a clear framework for assessing duration, credit quality, and liquidity.

Conclusion: a yield landscape in transition As the global economy navigates evolving inflation dynamics, growth prospects, and policy adjustments, the distribution of bond yields continues to reflect a cautious but constructive stance among investors. With a substantial majority of bonds trading below the 5 percent threshold, the market remains characterized by disciplined risk assessment, diversified portfolios, and a focus on income stability. While the path ahead remains uncertain, the current yield landscape highlights the enduring interplay between monetary policy, fiscal conditions, and the complex web of factors that shape global debt markets.