Global Holdings of U.S. Treasuries Reach Record High in 2025, Driven by Private Investment and Cross-Continental Demand

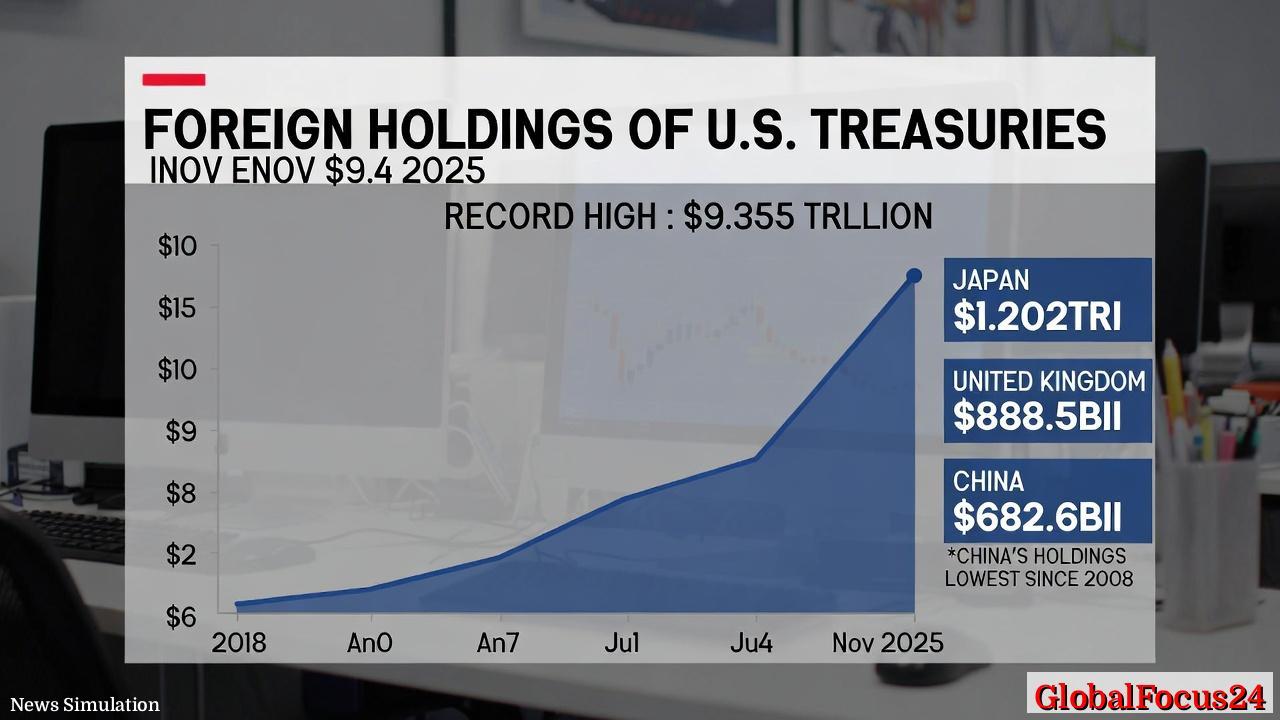

In November 2025, foreign holdings of U.S. Treasury securities climbed to a new peak of $9.355 trillion, according to the latest Treasury Department data. The month’s total rose by $112.8 billion from October, marking the highest level on record and underscoring a sustained trend of foreign investment that has carried through 2025. The reported figure encompasses both official reserves and private sector holdings, illustrating a broad-based market demand that has remained resilient even as the global economy navigates inflation, interest rate volatility, and shifting geopolitical dynamics.

Historical context: a long arc of growing foreign demand

The escalation in foreign ownership of U.S. Treasuries over the past decade has its roots in a mix of exchange-rate management, diversification strategies, and the search for safe, liquid assets in uncertain times. Since 2018, total foreign holdings have risen from roughly $6 trillion to surpass $8 trillion before reaching this record threshold in 2025. This trajectory reflects a period of relatively stable U.S. macro fundamentals, including a strong Treasury market, deep liquidity, and the global demand for risk-adjusted assets. It also mirrors central banks’ ongoing need to manage foreign exchange reserves in the face of monetary policy normalization in major economies.

Leading holders and changes within the portfolio

Japan remained the largest foreign holder of U.S. Treasuries in November 2025, with holdings of about $1.202 trillion, a level not seen since mid-2022. The persistent accumulation by Japan—spanning 11 consecutive months of increases—signals an ongoing strategy of reserve diversification and a preference for high-quality, highly liquid assets amid a low-interest-rate environment in some domestic segments. The United Kingdom ranked second, with holdings rising to approximately $888.5 billion, reflecting brisk activity by London-based financial institutions and sovereign entities seeking to maintain broad-based exposure to the U.S. debt market.

On the other hand, China’s holdings declined to around $682.6 billion, the lowest level since September 2008 and representing a drop of more than 10% from the start of 2025. The retreat by China aligns with a broader shift in its capital-flow management and a recalibration of reserves amid regulatory changes, currency considerations, and evolving trade relationships. The divergence between rising private-sector demand in some regions and reduced official and private allocations from others contributed to the net rise in total foreign holdings for November.

Private versus official components: where the gains came from

The month’s gain was driven largely by private holdings, which have been a principal engine of growth for foreign ownership in recent years. Official reserves—held by central banks and monetary authorities—have hovered near the $4 trillion mark, providing a stabilizing floor for the market. The majority of incremental demand in November appeared to originate from private investors, financial institutions, and sovereign wealth funds seeking diversification and yield in a globally interconnected financial landscape.

Regional patterns and cross-border dynamics

Europe accounted for a substantial share of foreign purchases throughout much of 2025, illustrating the region’s ongoing integration into the U.S. debt market as both a liquidity hub and a home for diversified asset allocations. The November 2025 figures reflect a broad-based appetite across Europe, the Americas, and parts of Asia, with buyers such as Norway, Canada, and Saudi Arabia cited as contributors to the month’s buying activity. The coordinated flow of purchases across continents highlights the appeal of U.S. Treasuries as a benchmark asset in a world where monetary policies continue to diverge across major economies.

Economic implications: what the record means for markets and policy

- Market liquidity and price discovery: A larger stock of foreign-held Treasuries contributes to deeper on-the-run and off-the-run market liquidity, facilitating smoother price discovery and lower transaction costs for traders and institutions. This liquidity is particularly valuable during periods of volatility, as it supports orderly borrowing costs for the U.S. government and broader financial markets.

- Interest rate environment: Foreign demand can influence the yields on U.S. Treasuries by shaping the demand-supply balance. When foreign buyers accumulate Treasuries, it can help moderate rises in yields, potentially affecting the cost of borrowing for the federal government as well as for U.S. households and businesses that rely on Treasury benchmarks for pricing.

- Monetary policy transmission: The international appetite for Treasuries interacts with domestic policy in nuanced ways. Strong foreign demand can amplify the global reach of U.S. monetary policy, making U.S. rate adjustments impactful not only at home but also in portfolios that include large overseas holdings. Conversely, shifts in foreign demand can prompt policymakers to monitor external financing conditions and reserve-management strategies.

- Fiscal considerations: The record level of foreign ownership underscores the interdependence between U.S. fiscal policy and global capital markets. Sustained demand from foreign buyers supports the Treasury’s ability to finance deficits at favorable rates, but it also places import on the U.S. fiscal trajectory to maintain credibility and predictable debt management.

Regional comparisons: how other markets stack up

- Japan versus China: Japan’s continued accumulation contrasts with China’s retreat, illustrating different trajectories in reserve management and economic priorities. While Japan emphasizes diversification and liquidity, China’s diversification away from U.S. Treasuries reflects a broader reallocation of reserves alongside shifts in its own currency policy and trade posture.

- Europe’s role: European buyers have long been a cornerstone of the U.S. debt market. The 2025 data emphasize Europe’s ongoing engagement, with any net flows contributing to a more globally balanced ownership structure. This pattern has implications for the resilience of the Treasuries market in the face of regional economic cycle shifts.

- The Americas and the Middle East: The participation of nations such as Norway, Canada, and Saudi Arabia points to a wide geographic distribution of demand. These buyers often pursue Treasuries for risk-adjusted returns, liquidity, and diversification within sovereign wealth frameworks and institutional portfolios.

Public reaction and narrative context

Private citizens and investors often view foreign holdings as a gauge of global confidence in the U.S. economy and the reliability of U.S. government debt. In 2025,s about the record level of foreign holdings were accompanied by discussions about the resilience of the U.S. Treasury market, the role of central banks in global financial stability, and the balance between domestic fiscal policy and international capital flows. While some observers highlighted potential vulnerabilities associated with high external ownership, others stressed the importance of a deep, liquid market that can absorb large-scale transactions with minimal disruption.

Regional resilience and risk factors

Looking ahead, several factors could influence the trajectory of foreign holdings in 2026 and beyond. These include:

- Global growth trajectories: If global growth remains uneven, central banks may continue to adjust monetary policy in ways that affect the relative attractiveness of U.S. Treasuries versus other safe assets.

- Inflation and real yields: Persistent inflation trends and the interplay with real yields will shape investor appetite for Treasuries. As real yields shift, risk-reward calculations for private and public buyers will adjust accordingly.

- Currency markets and reserve strategies: Movements in exchange rates and the evolution of reserve-management practices in major economies can drive changes in demand for U.S. debt. Countries seeking to optimize their balance sheets may alter their holdings in response to policy shifts or external shocks.

- Geopolitical considerations: Diplomatic relationships, trade developments, and regional security events can influence risk perceptions and the allocation of foreign exchange reserves, potentially affecting the flow of funds into or out of U.S. Treasuries.

A forward-looking perspective: what to watch in coming months

- Tendering patterns and maturities: The composition of holdings by maturity matters for the market’s sensitivity to rate changes. Investors’ preferences for short-, intermediate-, or long-term maturities can signal expectations for future rate trajectories.

- Technical factors in the Treasury market: Auction dynamics, primary dealers’ behavior, and secondary market liquidity will continue to shape pricing and turn-over. Any shifts in auction sizes or bid-to-cover ratios can offer early clues about demand patterns.

- Policy communication: Statements from the Federal Reserve, Treasury, and foreign central banks will be closely watched for indications of how external demand and domestic policy will interact with ongoing macroeconomic objectives.

Implications for regional economies and investors

For regional economies with exposure to U.S. debt markets, the record reflects an environment in which U.S. government bonds remain a cornerstone of global investment portfolios. Institutional investors—pension funds, insurance companies, sovereign wealth funds, and asset managers—often rely on Treasuries as a stabilizing component of diversified portfolios. The sustained foreign appetite can influence investment strategies across continents, informing risk management practices, duration strategies, and hedging approaches in the face of evolving macro risks.

Conclusion: a durable anchor in a shifting global map

The November 2025 milestone of $9.355 trillion in foreign Treasuries marks more than a numeric peak; it signals the continuing, nuanced balance between global capital flows and U.S. financial credibility. While certain nations adjust their exposure in response to domestic priorities and international relations, the broader trend points to a market that remains deep, liquid, and trusted by a wide spectrum of international investors. As economies adjust to new growth patterns, higher or fluctuating rates, and ongoing policy shifts, U.S. Treasuries are likely to remain a foundational instrument in the global financial system, serving as a crucial reference point for risk, liquidity, and strategic asset allocation across the world.