)

Fed Holds Rates as Dissenting Voices Signal a Cautious Path in 2026

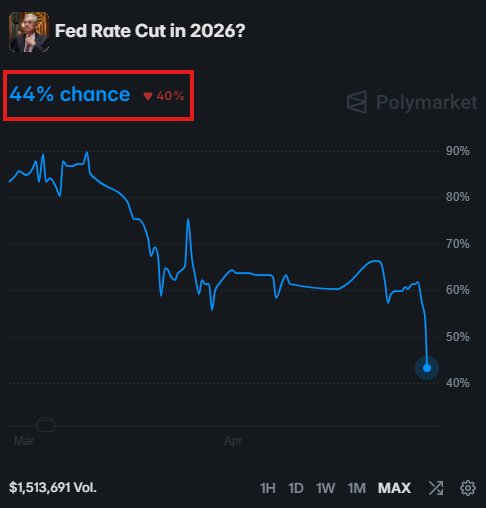

The Federal Reserve’s latest policy decision reframed the path for U.S. interest rates in 2026, signaling that a near-term rate cut is unlikely and that policymakers are prepared to contend with evolving economic pressures. The decision comes amid renewed debate within the Fed about inflation, labor markets, and financial conditions, with four dissents marking the first broad internal disagreement at this level since 1992. Financial markets absorbed the news with a mix of caution and recalibration as investors reassessed expectations for monetary policy this year.

Economic backdrop and context

The decision to hold rates reflects a careful balancing act by central bankers who must reconcile a resilient but cooling economy with persistent price pressures. Inflation has slowed from its double-digit peaks, yet core measures remain above the Fed’s longer-run target in many periods. At the same time, the labor market has shown signs of cooling—job openings have moderated, wage growth has paused in some sectors, and unemployment has edged higher—but remains historically tight in several industries. Against this backdrop, the Fed’s leadership emphasized that inflation, while trending toward the target, could reaccelerate if demands for goods and services outpace supply or if wage dynamics regain momentum.

The 2026 policy landscape

- Rate trajectory: By signaling no imminent rate cut, the Fed reinforced a slower, more deliberate pace for policy normalization. Markets had previously priced in some probability of cuts within the year, but the latest update shifted expectations toward a longer hold period and a cautious stance on how quickly the Fed would withdraw its accommodative stance.

- Dissent dynamics: The four dissents underscore a notable shift in internal consensus. These voices typically arise from policymakers who wish to prioritize tighter financial conditions to curb inflation risks or who are concerned about the lagged effects of monetary tightening. While dissent does not automatically translate into policy change, it does illuminate a broader debate about risk management, the trajectory of inflation, and the appropriate balance between growth and price stability.

- Economic indicators in focus: The Fed’s decision followed a suite of data on consumer spending, manufacturing output, and wholesale price trends. Early signals suggested that demand remained robust in some pockets of the economy, even as supply chains continued to smooth and inventory dynamics evolved. The central bank noted that incoming data would play a critical role in shaping policy moves in the quarters ahead.

Regional considerations and comparisons

The U.S. economy is not monolithic, and regional performance adds nuance to central bank decisions. Areas with high-tech sectors, such as the West Coast, demonstrated strong hiring in software and biotech, while manufacturing-heavy regions faced cyclical pressures from global demand fluctuations. The Fed’s cautious stance is thus partly a response to divergent regional conditions: some districts reported cooling price pressures and moderating growth, while others faced sustained demand that could rekindle inflationary momentum if not managed carefully.

International comparisons provide additional context. Global central banks are navigating a mixed landscape of persistent inflation in some economies and slowing growth in others. In several advanced economies, policymakers balance the desire to support growth with mechanisms to prevent overheating, much as the Fed seeks to avoid premature policy loosening that could necessitate a steeper tightening later. The international environment matters for the United States through exchange rates, import prices, and cross-border investment flows, all of which influence domestic inflation and growth trajectories.

Historical context

To understand the current moment, it helps to recall how past cycles unfolded when the Fed faced similar crossroads. In the early 1990s, a string of dissents and debates around policy pathways foreshadowed a broader reorientation in monetary policy. The 1992 instances of dissent reflected concerns about overheating in particular sectors and the desire to calibrate policy to evolving economic conditions. Those historical episodes illustrate that central banks occasionally walk a fine line between maintaining credibility on inflation and supporting employment and growth. The present moment echoes that tension, with market participants keenly watching for any shift in the inflation signal, labor market resilience, and financial conditions that could complicate the path to normalization.

Implications for households and businesses

- Borrowing costs and credit conditions: For households, the timing of rate cuts affects mortgage rates, auto loans, and credit card costs. A longer hold period means that borrowing costs may remain elevated relative to earlier expectations, shaping consumer spending, homebuying plans, and debt management decisions. For businesses, financing conditions influence capital expenditure, equipment purchases, and hiring plans. An extended stance could discourage aggressive expansion in the near term, while also keeping credit risk expectations prudent for lenders.

- Investment and market dynamics: Equity and fixed-income markets react to policy guidance with volatility that often creates both risk and opportunity. In a hold scenario, investors may gravitate toward sectors with price resilience or those that benefit from stable monetary conditions. The bond market typically prices in higher yields when rate cuts are delayed, affecting long-term financing costs for projects and infrastructure initiatives.

- Inflation expectations: Inflation psychology matters as households and firms form expectations about future price levels. The central bank’s communication around inflation containment remains a key driver of these expectations. Clear signals that price gains are moderating—and that the Fed will act if needed—can anchor expectations and contribute to broader economic stability.

Public reaction and sentiment

Public sentiment often rides the wave of central bank announcements. On the ground, households and business leaders weigh immediate financial implications against longer-term economic prospects. Some consumers may welcome the prospect of steadier borrowing costs, while others worry about the pace of wage growth and the potential for rising prices on essential goods. In regional markets, small business owners may recalibrate expansion plans in response to anticipated changes in interest rates, while homeowners monitor mortgage-rate forecasts as they plan refinanced loans or new housing purchases.

Outlook and considerations for the year ahead

- Data dependence: The Fed emphasized that its policy path would hinge on incoming data. Key indicators—inflation measures, labor market statistics, consumer spending, and industrial production—will influence the timing of any future policy shifts. Market participants will be scanning for signals that inflation is sustainably converging toward the target and for signs of emerging wage pressures.

- Financial conditions: The stance taken by financial markets in response to the decision will feed back into the Fed’s assessment of monetary conditions. If credit conditions tighten or if financial markets signal heightened risk, the central bank may reevaluate its approach to guard against unintended tightening or financial instability.

- Regional growth patterns: The disparate regional performance noted earlier will continue to shape economic prospects. Regions with strong tech and services sectors could maintain momentum, while areas reliant on manufacturing or export demand may experience more pronounced cyclical fluctuations. Policymakers will watch regional indicators to gauge the broader health of the economy.

A note on the broader policy framework

The Fed’s decision fits within a broader framework of macroprudential oversight and balance-sheet considerations. While rate policy remains a critical tool, other dimensions—such as the management of the federal budget, the health of regional banks, and the resilience of supply chains—also influence the trajectory of growth and inflation. The current stance signals a commitment to data-driven adjustment, with an emphasis on preventing inflation from reaccelerating while supporting sustainable employment gains.

Economic impact by sector

- Housing and construction: Mortgage rates near current levels shape demand for homes and renovation activity. A steadier rate environment can support housing market stabilization, though affordability and inventory remain pivotal factors. Builders and lenders alike will adjust timelines for project starts and financing strategies based on anticipated policy moves.

- Technology and innovation: Sectors driving productivity gains—software, semiconductor manufacturing, and biotech—continue to contribute to growth while navigating global supply chain dynamics and talent competition. Monetary policy clarity helps these sectors plan capital-intensive projects and research investments with greater confidence.

- Energy and commodities: Energy markets respond to macroeconomic expectations and financial conditions. If rate expectations shift more decisively, it could influence investment in energy infrastructure and the cost of capital for commodity-linked activities, with downstream effects on prices and consumer energy bills.

- Small business activity: Local enterprises gauge interest rates for expansions, inventory financing, and payroll investments. A cautious Fed stance can incentivize prudent budgeting while still enabling growth opportunities where demand remains robust.

Historical parallels and lessons for policymakers

Looking back, the Fed’s experience with late-cycle rate management offers both caution and insight. Policymakers have learned that delay or hesitation must be balanced against the risk of allowing inflation to become more entrenched. Conversely, premature tightening can stifle growth and reduce job creation. The current position—holding rates with dissent—reflects a deliberate posture: stay vigilant, respond to data, and avoid overreacting to short-term fluctuations while maintaining a credible commitment to price stability.

Conclusion

As the Fed navigates an uncertain but resilient economy, the decision to hold rates and the presence of dissent underscore a nuanced approach to monetary policy in 2026. The central bank’s priority remains clear: anchor inflation expectations, support sustainable employment, and adapt to evolving economic signals without compromising financial stability. For households, businesses, and regional economies, the coming months will hinge on data movement, the pace of wage moderation, and the external environment that continues to shape demand and prices.

In a landscape of shifting bets and evolving data, the path forward will require vigilance and flexibility. The Fed’s guidance, criticism, and contingency planning will influence borrowing costs, investment decisions, and the broader tempo of economic activity across the United States in the year ahead. As markets digest the implications, observers will watch closely for fresh data that could tilt policy toward gradual easing or a more extended holding pattern, always with an eye on the balance between price stability and real growth.