Credit Card Delinquencies in the U.S. Reach Highest Level Since 2011, Signaling Shifts in Consumer Debt Dynamics

The United States is experiencing a notable tightening in consumer credit health as credit card delinquencies rose to 12.7 percent in the fourth quarter of 2025, the highest level observed since the first quarter of 2011. This uptick, driven by a combination of economic pressure, evolving consumer behavior, and shifting risk profiles within major card portfolios, underscores both a lingering post-pandemic debt normalization and the persistent challenge of balancing credit access with prudent credit risk management. As lenders, policymakers, and households digest these developments, the implications span economic stability, regional performance, and the broader trajectory of household indebtedness.

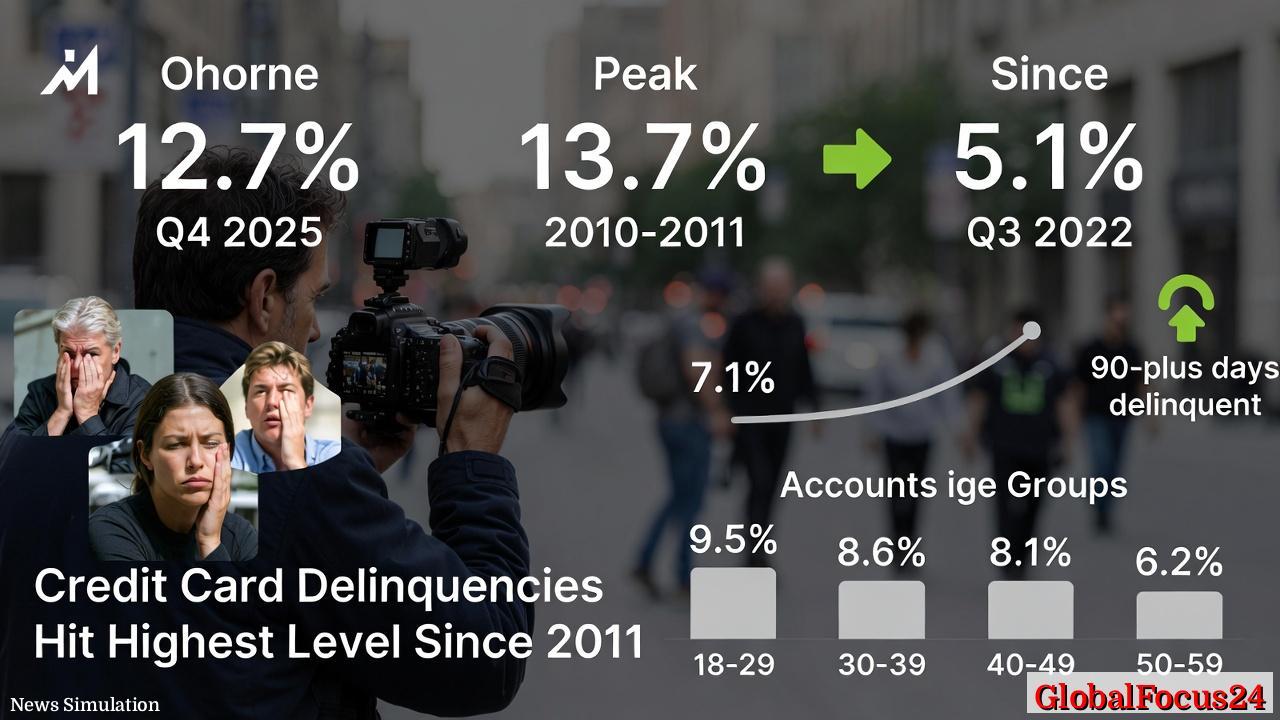

Historical context: tracing the arc from recovery to elevated delinquency To understand the current environment, it helps to look at the long arc of credit card delinquencies following the 2008 financial crisis. The late 2000s and early 2010s saw a steep spike in delinquencies, peaking around 13.7 percent in 2010–2011, before gradually moderating as unemployment declined, consumer balance sheets improved, and credit markets normalized. The ongoing rise from 2022 onward marks a reversion toward stress conditions not seen since that post-crisis period, yet with distinct dynamics. Unlike the Great Recession-era shock, today’s delinquencies emerge in a backdrop of low unemployment relative to historical highs, evolving consumer credit utilization, and a more segmented consumer base where vulnerability concentrates in younger cohorts and lower-to-middle income brackets.

Fourth-quarter snapshot: 12.7% overall delinquency

- The quarterly increase of 0.3 percentage points puts the total delinquency rate at 12.7 percent. This level sits just below the 2010–2011 peak, signaling that risk exposure in the credit card portfolio remains historically elevated.

- The metric typically captures borrowers who are 30 days or more past due, with “serious delinquency” commonly defined as 90 days or more past due. This period saw transitions into 90-plus days delinquency rise by 10 basis points to 7.1 percent, marking the third-highest level since early 2011.

- The pace of deterioration since the third quarter of 2022—an increase of 5.1 percentage points—outstrips the magnitude of stress observed during the 2008–2009 downturn, highlighting a marked shift in consumer credit quality over the past few years.

Demographic patterns: a focus on younger borrowers

- The most pronounced volatility is among younger age groups. The 18–29 cohort exhibited a transition rate into serious delinquency of 9.5 percent, the highest among the measured brackets.

- The 30–39 group followed closely at 8.6 percent, signaling that early adulthood remains a period of heightened risk, potentially tied to employment transitions, student debt burdens, and balancing household expenses.

- For mid-life groups, the 40–49 and 50–59 brackets posted 8.1 percent and 6.2 percent, respectively, indicating that while delinquency persists across ages, younger consumers continue to experience outsized stress.

- The distribution of risk by age underscores the importance of targeted risk management strategies within card portfolios and suggests a need for consumer education and credit-building programs for emerging adults.

Economic impact: implications for lenders, consumers, and the wider economy

- For lenders, rising delinquencies translate into higher credit losses and more aggressive loss mitigation costs. Banks and card issuers may respond with tighter underwriting standards, higher minimum payments, or slower growth in new credit lines, all of which can influence consumer access to credit.

- Consumers face a higher risk of a downward credit cycle: strained budgets, unexpected expenses, and rising interest costs can create a feedback loop, where higher debt service leads to reduced discretionary spending and slower income growth.

- The macroeconomic ripple effects include potential reductions in consumer spending, which has been a cornerstone of GDP growth in recent years. Slower consumer expenditure can influence retail sectors, automotive financing, and services, contributing to a broader cycle of slower economic momentum if sustained.

- Regional variation is likely to be pronounced. Coastal urban areas with higher living costs, versus inland and rural regions with different employment mixes, may exhibit divergent delinquency trajectories. Local labor markets, cost of living, and access to credit influence the timing and magnitude of delinquency shifts.

Regional comparisons: perspective across major markets

- In high-cost metro areas with elevated living expenses, households may face tighter budgets, pushing some borrowers toward higher credit utilization and increased delinquency risk during economic softness or wage stagnation.

- Regions with stronger manufacturing or services sectors experiencing payroll volatility could see pockets of stress in credit card portfolios, especially among younger workers who are more mobile and leveraged for education and experience-building.

- Conversely, markets with diversified economies, stronger job growth, and robust wage gains may exhibit more resilience, though the persistence of debt and higher interest-rate environments can still exert pressure on household balance sheets.

- The health of regional consumer credit should be watched in conjunction with unemployment trends, wage growth data, and local housing market dynamics, as these factors collectively influence the ability to manage debt obligations.

Credit conditions and consumer behavior: what’s driving the shift

- Higher interest rates continued to weigh on credit card costs for borrowers carrying balances, increasing the burden of minimum payments and accelerating the path toward delinquency for some households.

- Inflation dynamics, while moderating, still influence discretionary spending and savings rates. When households allocate more of their budget to essential needs and debt service, credit card flexibility can shrink.

- Spending patterns show a tilt toward essential purchases and financing of recurring expenses, which can elevate reliance on revolving credit if other financing options are constrained or less accessible.

- Delinquency trends are also shaped by underwriting changes made over the pandemic period and the post-pandemic normalization of card portfolios, as lenders recalibrated risk appetites in response to evolving consumer credit behavior and macroeconomic uncertainty.

Policy and regulatory context: the environment for credit risk management

- Supervisory expectations emphasize robust risk governance, effective collection strategies, and prudent capital planning to absorb potential losses from rising delinquencies.

- The current environment may prompt a recalibration of credit scoring models to reflect shifting borrower risk profiles, with a focus on age cohorts, utilization patterns, and income volatility.

- Consumer protection and disclosure rules continue to influence how lenders communicate terms, manage defaults, and provide assistance programs during periods of rising delinquency.

What this means for households and financial literacy

- Households should evaluate monthly cash flow, prioritizing essential needs and debt repayment, to cushion against rising credit costs.

- Building an emergency fund and maintaining transparent debt calendars can help mitigate the risk of sudden delinquencies.

- For younger borrowers, financial literacy initiatives around credit utilization, interest accrual, and repayment strategies can be especially valuable in reducing the likelihood of long-term delinquency.

Historical context and future directions: reading the tea leaves

- The current high delinquency rate, while historically elevated, does not automatically translate into an immediate financial crisis. It does, however, signal tighter credit conditions for consumers and greater risk sensitivity for lenders.

- If inflation remains on a controlled trajectory and wage growth strengthens, there is potential for stabilization in delinquency trends. Conversely, renewed macroeconomic stress—such as energy price shocks or sustained unemployment pressure—could accelerate strain, feeding into a feedback loop of higher delinquencies and tighter credit.

- Monitoring key indicators, such as 90-plus day delinquency rates, average credit card balances, and utilization trends across age cohorts, will be important for understanding whether the current period marks a turning point or a plateau in consumer credit health.

Regional performance: actionable takeaways for markets across the United States

- Urban centers with high living costs may experience more pronounced stress during economic downturns, underscoring the importance of targeted support for households facing rent and utility pressures alongside debt management.

- Rural and smaller metro areas may see variable outcomes based on local employment cycles and the availability of credit products tailored to stable income streams and responsible borrowing habits.

- Financial institutions may respond with regionally tailored risk models and proactive outreach programs that offer repayment guidance, hardship accommodations, and financial counseling to mitigate delinquency growth.

Conclusion: navigating a moment of heightened credit card risk The fourth-quarter rise in credit card delinquencies to 12.7 percent, the highest since 2011, reflects a period of elevated risk in consumer credit. While the economy continues to show resilience in several dimensions, the age-specific vulnerabilities and regional disparities highlight the need for vigilant risk management within lenders, prudent financial planning for households, and continued monitoring by policymakers and market participants. As the debt landscape evolves, the balance between accessible credit and sustainable borrowing remains a central theme shaping the financial well-being of American households in 2026 and beyond.