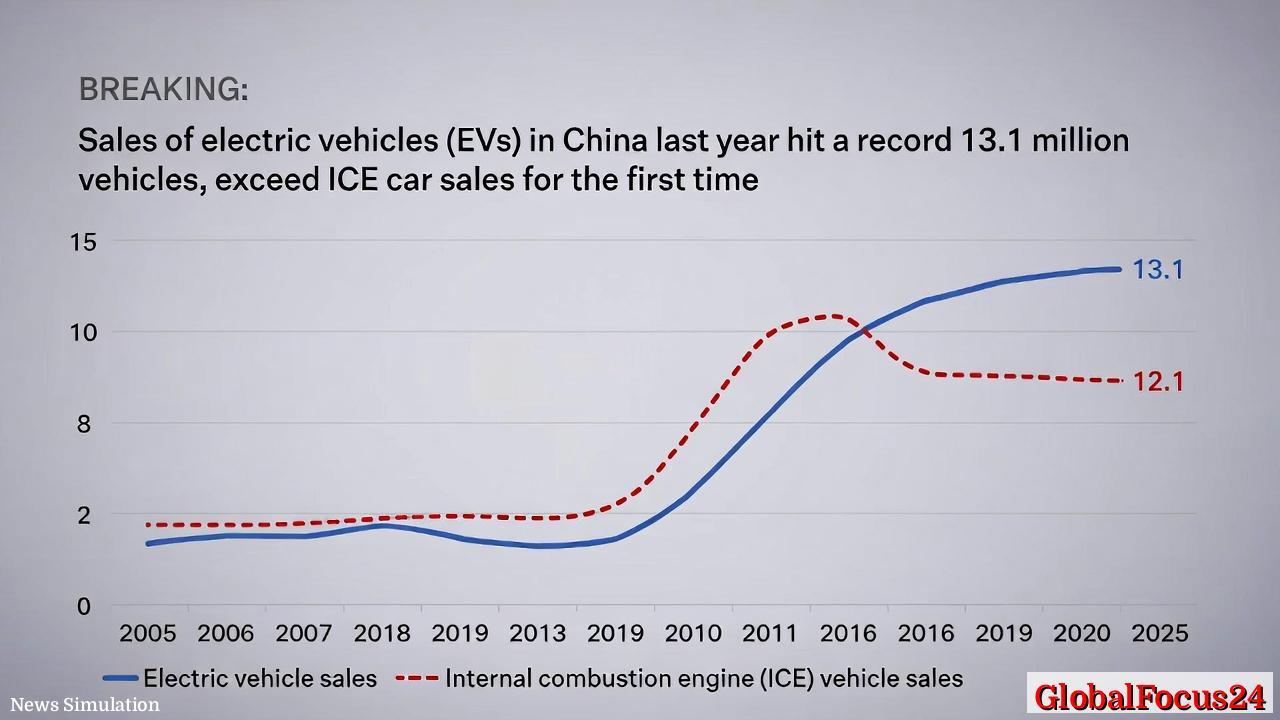

Sales Slump: China’s Traditional Car Market Faces a Decade of Decline and Transformation

Sales of traditional internal combustion engine (ICE) vehicles in China have extended a dramatic, decade-long slide, with 2025 posting the lowest annual totals in 15 years and signaling a structural shift in the world’s largest auto market. The latest figures show ICE vehicle sales totaling 12.3 million units for 2025, down 13% year-on-year through November data, marking the eighth consecutive annual decline and underscoring a broader transition toward electrification, digitization, and new mobility models. This trajectory follows a sharp 49% drop since the peak years of 2017, equating to a cumulative loss of roughly 11.6 million ICE units over the period. The ongoing decline is not merely a fiscal concern for traditional manufacturers; it reflects a sweeping economic and industrial recalibration across China’s automotive ecosystem.

Historical context: from explosive growth to a steady reorientation

To understand the present situation, it helps to recall the ICE market’s ascent in the early 2000s. China’s automotive industry built its modern backbone on volume, speed, and scale. Output surged as global automakers established joint ventures, domestic brands expanded distribution networks, and consumer demand grew with rising urbanization and household income. By the mid-2010s, passenger car sales had become a symbol of modernization, with ICE vehicles representing the bulk of consumer choice and a benchmark for employment, supply chains, and regional development.

Yet, the last decade has redefined that landscape. Government policy, consumer preferences, and technological progress converged to accelerate a shift toward electrified powertrains, particularly battery electric vehicles (BEVs) and plug-in hybrids. In 2017, the ICE market in China stood at a peak that would not be revisited. Since then, sales have trended downward as BEVs and hybrids captured increasing share, aided by policy incentives, local manufacturing ambitions, and consumer awareness about sustainability and total cost of ownership. By 2025, ICE sales had declined to their lowest level in 15 years, revealing a structural transition rather than a temporary demand hiccup.

Economic impact: implications for manufacturers, suppliers, and regional hubs

- Revenue and profitability pressures: The sustained decline in ICE sales compresses margins for traditional automakers that relied on high-volume, low-margin ICE platforms. At the same time, BEV and hybrid segments, often supported by subsidies or favorable financing terms, have started to command higher gross margins in certain product lines, even as competition intensifies. The net effect is a reshaping of profitability across brand portfolios, with some firms prioritizing electrified platforms and others seeking to diversify through mobility services or software-centric offerings.

- Supply chain realignment: A long-term pivot toward electrification requires different components—lithium batteries, electric motors, power electronics, and battery management systems—driving demand toward new suppliers and re-valuing old ones. Regions with established battery plants and chip ecosystems may gain strategic advantages, while traditional ICE-intensive manufacturing belts face a period of transition, potential rationalization, and re-skilling costs.

- Employment and regional development: The reallocation of labor—from ICE assembly lines toward battery production, charging infrastructure, and software development—affects employment across manufacturing corridors. Provinces with highly integrated EV ecosystems could see accelerated investment and job creation, while areas dependent on ICE-centric plants may experience transitional challenges. Policy support, retraining programs, and public-private partnerships are likely to shape these outcomes.

- Investment cycles and capital allocation: Capital markets and corporate planning have increasingly favored electrification ambitions. R&D budgets are tilting toward battery technology, autonomous driving software, and energy efficiency innovations. Investors monitor the pace at which automakers can convert product pipelines, secure raw materials, and scale charging networks to sustain growth beyond ICE decline.

- Trade and regional competition: As China intensifies its leadership in EV technologies, regional comparisons with peers highlight competitive advantages. Domestic brands leveraging scale, cost advantages, and integrated ecosystems may outpace traditional foreign competitors in the longer term, while international automakers recalibrate joint ventures and localization strategies to align with China’s evolving market mix.

Regional comparisons: China’s trajectory versus other major markets

- East Asia and the broader Asia-Pacific region: China’s ICE decline mirrors a global shift but occurs at a more accelerated pace due to government support for electrification and a large domestic BEV appetite. Other major markets, such as Japan and South Korea, are balancing ICE retention with aggressive BEV deployment, but China’s sheer scale and policy environment give it a distinctive lead in EV manufacturing and supply chain development.

- Europe: European markets have also experienced ICE contraction amid policy pushes toward zero-emission zones and CO2 regulations, yet the pace and drivers differ. Europe benefits from a mature charging network and established BEV consumer base, but China’s battery supply chain and domestic production capacity provide a unique competitive edge in volumes and price dynamics.

- United States: The U.S. market shows growing BEV adoption but faces different structural factors, including consumer incentives, domestic production strategies, and charging infrastructure development. While ICE sales remain robust in some segments, the shift toward electrification adds complexity for manufacturers seeking global alignment across markets.

- Emerging markets: In many developing economies, ICE vehicles continue to play a significant role due to affordability and infrastructure constraints. However, China’s leadership in EV technology increasingly influences global price curves and component standards, accelerating a broader transition beyond its borders.

Implications for policy and consumer behavior

- Policy incentives and regulation: Government policy remains a primary driver behind the ICE-to-EV transition. Subsidy programs, purchase tax reductions, electric-vehicle mandates, and infrastructure investments can accelerate uptake or recalibrate demand in the short term. Policymakers must balance the pace of transition with concerns about manufacturing resilience, employment, and energy demand.

- Charging infrastructure and energy mix: The evolution of charging networks and the decarbonization of the energy grid are crucial to sustaining BEV growth. Urban planning, grid upgrades, and smart charging initiatives will influence consumer confidence and total cost of ownership for electrified vehicles.

- Consumer sentiment and adoption curves: As transportation preferences shift, consumers weigh factors such as range, charging availability, vehicle cost, and brand trust. Automakers that can demonstrate reliability, long-term value, and compelling ownership experiences stand to capture greater market share in a post-ICE era.

Market outlook: what the data suggests about the next decade

- Continued ICE consolidation: The downward trend in ICE sales over recent years suggests continued consolidation and a shrinking ICE market share. Manufacturers that remain heavily invested in ICE platforms may increasingly face overcapacity and the need to pivot toward electrified offerings or diversified mobility solutions.

- Rapid acceleration of EV adoption: The pivotal driver of future growth lies in BEVs and other low-emission technologies. Battery technology improvements, supply chain maturation, and expanding charging networks are expected to unlock sustained demand and potentially restore robust sales growth in electrified segments.

- Strategic diversification: Firms are likely to pursue a multi-pronged approach—expanding EV lineups, investing in battery manufacturing or partnerships, and exploring software-driven services such as vehicle diagnostics, fleet management, and autonomous features—to create resilient revenue streams that extend beyond traditional ICE sales.

Public reaction and market sentiment: a changing automotive culture

Across urban centers and manufacturing hubs, the shift away from ICE emphasizes a broader cultural transformation. Consumers often associate BEVs with modernity, clean urban living, and progressive policy alignment. At the same time, concerns about charging accessibility, vehicle price parity, and the longevity of battery technology fuel ongoing dialogue among drivers, policymakers, and business leaders. Public reaction ranges from enthusiastic adoption in major cities to cautious optimism in regions where charging infrastructure remains uneven. The narrative now centers on a cleaner, smarter transportation ecosystem rather than a simple replacement of one propulsion type with another.

Conclusion: a watershed moment for China’s automotive industry

China’s decline in traditional ICE vehicle sales over the past decade reflects more than shifting consumer taste; it marks a fundamental transformation of the country’s automotive industry. The alignment of policy, technology, and infrastructure has accelerated electrification, reshaping demand, investment, and employment across the sector. As ICE volumes continue to contract, the country’s leadership in EV production and supply chain development positions it at the forefront of a global transition with wide-reaching economic implications. Stakeholders—from policymakers to manufacturers, suppliers to consumers—stand at a crossroads where strategic decisions in the near term will influence industry structure, regional economics, and the shape of mobility for years to come. The coming decade will reveal how quickly ICE demand fades and how swiftly electrified transportation becomes the default choice for a broad cross-section of Chinese consumers.