Central Banks Accelerate Gold Purchases as Crisis Hedge and Reserve Diversifier

Central banks around the world are amassing gold at a pace not seen in years, signaling a broader strategy to shield national treasuries from currency volatility, inflation, and geopolitical risk. The latest survey-based evidence shows that a record share of central banks view gold as a crisis-tested store of value and a stabilizing ballast for reserve portfolios, especially when confidence in fiat currencies wavers. This shift reflects a long-standing practice that has gained renewed urgency amid renewed global uncertainty and shifting monetary dynamics.

Historical context: gold as a perennial hedge and anchor

- For decades, gold has served as a trusted hedge against inflation and currency depreciation. In periods of financial stress, gold’s scarcity and global liquidity make it an appealing counterpart to fiat reserves, a role that has persisted through episodes such as debt crises, currency reforms, and budgetary instability. This enduring function helps explain why central banks have repeatedly turned to gold as part of a diversified reserve strategy.

- The post-2008 landscape deepened gold’s appeal as a crisis-resistant asset. With central banks engaged in expansive monetary easing and extraordinary liquidity measures, gold offered a non-sovereign, globally liquid store of value less prone to policy, political, or currency-specific shocks. Recent years have reinforced that narrative as price spikes and macro volatility underscored gold’s role as a stabilizing asset in reserve portfolios.

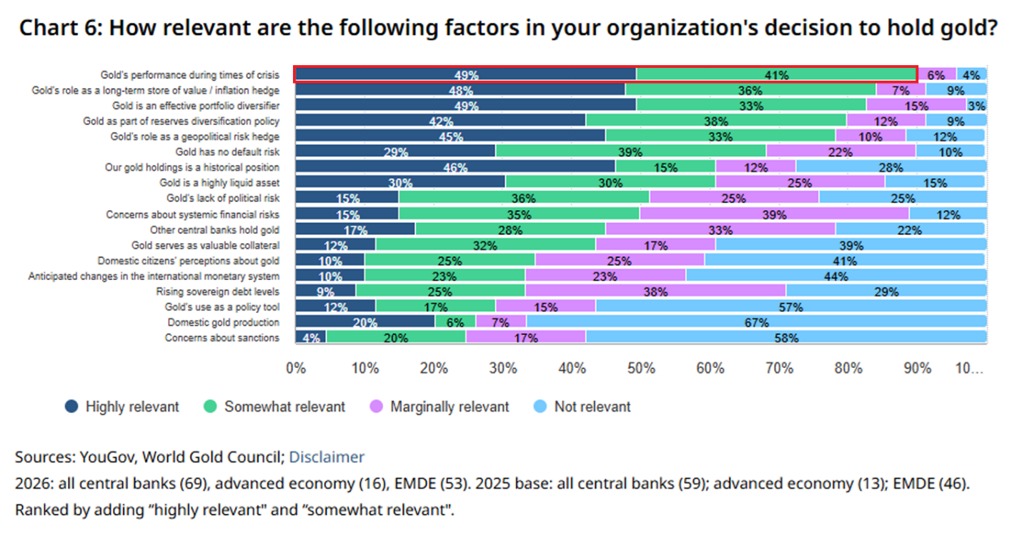

Core reasons behind the surge in buying

- Inflation hedging and monetary resilience. Gold’s historical tendency to preserve purchasing power during currency depreciation makes it a natural hedge as inflationary pressures re-emerge and as real interest rate environments fluctuate. Central banks use gold to shield wealth against the eroding effects of rising prices on their reserves, complementing traditional fiat holdings.

- Crisis protection and geopolitical uncertainty. In times of geopolitical tension or financial market stress, gold’s universal acceptance and portability enable central banks to maintain liquidity and confidence even when other assets become constrained or politicized. This crisis-resistant characteristic is repeatedly cited as a primary driver for reserve diversification into gold.

- Diversification and reduced issuer risk. Holding gold alongside currencies and government bonds reduces exposure to any single issuer or monetary system. Gold’s non-mollarized, globally traded nature provides a counterbalance to country-specific risks, helping stabilize overall reserve performance in imperfect markets.

- Financial-system resilience and policy autonomy. By stocking gold, central banks can bolster credibility and policy resilience in scenarios where domestic currencies face sharp devaluations, external shocks, or sanctions. Gold is perceived as a neutral, portable asset that can be mobilized quickly in support of national financial stability.

Regional patterns and notable developments

- Emerging markets have been particularly active, driven by concerns over dollar strength, trade tensions, and the need to diversify away from a heavy reliance on a single reserve asset. In many countries, gold now sits at the core of strategic asset allocation, reflecting a broader shift toward asset diversification and resilience.

- Developed economies have also continued accumulation, albeit at varying paces, underscoring a global consensus on the importance of gold as a crisis hedge and long-term reserve anchor rather than a speculative instrument. The steady growth across multiple central banks indicates a long-run structural preference for gold as a stabilizing reserve component.

Implications for gold prices and markets

- Reserve-buying cycles can support gold prices, particularly when multiple central banks signal a stronger preference for bullion over other assets. While central bank purchases are typically a small fraction of annual global supply, sustained demand from a broad base of countries can contribute to price strength over extended periods.

- Market dynamics also reflect expectations of future policy regimes. If central banks view gold as a credible hedge amid inflationary risks and policy uncertainty, prices may remain elevated relative to periods of calmer financial conditions, even as broader risk assets move differently.

Comparisons with other reserve assets

- Compared with Treasuries or sovereign bonds, gold offers non-credit risk and universality, which makes it attractive during times of currency stress or when governments want to avoid over-reliance on any one counterparty. That risk-diversification logic remains central to why central banks continue to accumulate gold alongside other reserves.

- Gold’s liquidity and global acceptance stand out as advantages during international crises or sanctions, reinforcing its role as a portable, fungible asset that can be mobilized across borders with relative ease.

Public and market reactions

- Public sentiment often views central bank gold purchases as a signal of growing caution about monetary debasement or geopolitical risk. While observers disagree on pace and scale, the consensus is that gold holds a unique place in national balance sheets as a shield against uncertainty.

- Analysts note that the price impact of ongoing central bank buying can be modest in the near term due to the scale of global demand being spread across many jurisdictions, but the cumulative effect over years can shift the gold market’s baseline expectations.

What to watch next

- The pace of purchases in major economies, including reserve diversification strategies and quarterly reporting, will shape the gold market’s trajectory in the near term. Given the reflexive relationship between central-bank demand and bullion prices, continued buying could reinforce a higher-price environment even if inflation and growth signals fluctuate.

- Developments in monetary policy, currency stability, and geopolitical tensions will continue to influence demand dynamics. If global risk sentiment shifts or if inflation moderates, the rationale for gold accumulation may adjust, though many central banks appear to view gold as a durable precaution rather than a transient trading vehicle.

Illustrative context: a sense of urgency in the market

- In today’s uncertain landscape, central banks treat gold not as a speculative bet but as a strategic reserve asset designed to preserve financial sovereignty and national wealth across a spectrum of possible futures. The repeated emphasis on crisis resilience and diversification reflects a long-standing, pragmatic approach to reserve management that remains highly relevant as new risks emerge.

Conclusion

- The global uptick in central-bank gold purchases underscores gold’s enduring role as a crisis hedge, diversification tool, and anchor for monetary credibility. While the exact pace and composition of purchases vary by country, the core rationale — resilience in the face of inflation, financial stress, and geopolitical risk — remains consistent across regions and policy regimes.