All-Cash Home Purchases in the U.S. Fall to Five-Year December Low, Signaling Market Shift

Decline in All-Cash Purchases Marks Changing Dynamics in U.S. Housing

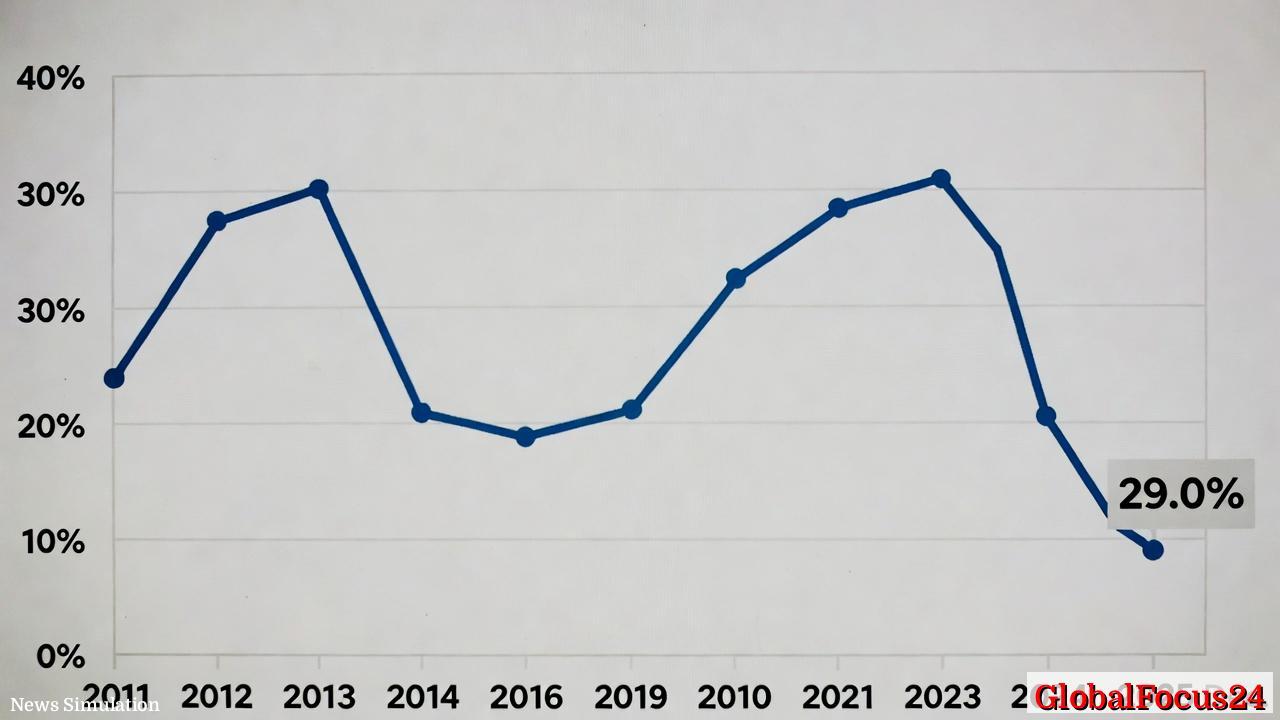

The share of homes purchased with all cash in the United States slipped to 29% in December 2025, down from 30.3% a year earlier. The decrease marks the lowest December reading since 2020 and underscores a gradual cooling in investor and high-net-worth buyer activity after several years of elevated cash transactions.

This data, drawn from county deed records across 38 major metropolitan areas, reflects home sales in which no mortgage loan information appeared on the title—typically a clear signal of cash purchases. The shift indicates a notable rebalancing in how Americans finance real estate, as declining cash participation meets falling mortgage rates and rising listings in the broader housing market.

Historical Patterns Show Cash Peaks Follow Rate Surges

All-cash buying has long served as a reliable barometer of market sentiment and affordability pressures. Since 2011, the share of cash transactions has oscillated between roughly one-quarter and one-third of all home sales, with distinct peaks emerging during periods of tight credit or financial volatility.

- Around 2011 and 2012, cash purchases surged near 35% as the market reeled from the Great Recession and foreclosed properties drew investors seeking discounted deals.

- Between 2015 and 2019, the share steadied around 25%–27% as mortgage financing became more accessible and home prices began to recover nationwide.

- Beginning in 2021, the rate surged again—climbing close to 33% in late 2023—driven by investors and affluent buyers sheltering from record-high borrowing costs.

By the close of 2025, however, that upward trajectory had reversed. The 29% figure in December not only represented a five-year low for that month but also reflected the broad weakening of investor demand and improved financing conditions that followed successive quarters of easing inflation and stabilizing mortgage markets.

Influence of Mortgage Rate Movements

The timing of the decline aligns closely with the trajectory of U.S. mortgage rates. After peaking at multi-decade highs in 2023, average 30-year fixed mortgage rates gradually fell through 2024 and into 2025. The shift eroded the relative advantage of cash offers that had dominated in earlier periods of credit scarcity.

Buyers who previously found cash king in a market marked by constrained supply and fierce bidding wars began re-entering the lending market as rates eased. This return of financed buyers diversified buyer types, particularly first-time purchasers who had struggled to compete with investors armed with liquidity.

Economists note that when rates fall, financed buyers regain leverage while cash buyers lose some of their negotiating power. “Cash dominance typically softens as financing becomes more affordable and available,” said one housing analyst familiar with transaction trends over the past decade.

Regional Imbalances Show Varying Market Responses

Regional data reveal that all-cash activity remains far from uniform across U.S. markets. In high-priced metro areas like San Francisco, New York, and Los Angeles, the use of cash continues to play a larger role due to elevated price points and the presence of international and institutional investors. In contrast, markets like Dallas, Phoenix, and Atlanta—where price growth and investor activity surged earlier in the decade—saw more pronounced drop-offs through 2025.

Florida remains a distinctive outlier. Metropolitan areas including Miami, Tampa, and Naples have historically reported some of the nation’s highest shares of cash home sales, bolstered by retirement migration, overseas buyers, and second-home demand. Even there, local agents report moderation as inventory levels slowly improve and sellers display more flexibility on pricing.

In the Rust Belt and parts of the Midwest—such as Cleveland, Detroit, and Pittsburgh—cash buying also remains elevated compared to national averages. These regions attract smaller investors purchasing rental properties at lower price points, often below thresholds where traditional financing remains practical or cost-effective.

Investor Retreat and Normalization

The current downtrend in cash transactions coincides with reports that institutional and small-scale real estate investors have scaled back acquisitions. Rising insurance costs, tougher rent regulations in some states, and moderating rental yields have reduced incentives to purchase properties outright.

During the height of the pandemic-era housing frenzy, investors often accounted for a substantial portion of cash transactions, competing aggressively with owner-occupants. That investor pullback now points to a market gradually finding equilibrium after years of intense demand and limited supply.

A brokerage executive in Chicago noted that “the balance between investor and traditional buyer activity feels closer to normal, and that’s generally healthy for long-term market stability.”

Broader Economic Context: Cooling Inflation and Stabilizing Prices

The decline in cash purchases cannot be viewed in isolation. It parallels an environment of easing inflation, modest economic expansion, and a better-aligned housing supply. As inflation slowed during 2025, household budgets began to stabilize, fostering improved confidence among financed buyers.

Meanwhile, sellers faced price sensitivity from a broader base of shoppers comparing financing options. The national median home price decelerated slightly after years of double-digit growth, a sign that affordability pressures were beginning to ease even as property values remained historically elevated.

The result has been a housing market trending toward moderation rather than contraction—a notable distinction from past downturns triggered by credit shocks or mass foreclosures.

Long-Term Trends: The New Normal for Cash

Historically, cash purchases accounted for about one in four home sales nationwide, a baseline that many economists now view as the “structural floor” for the U.S. housing system. A sustained share below that level would be unprecedented in modern times, but a return toward the mid-20% range would still signal normalization rather than weakness.

Cash buyers will likely continue to play a significant role in niche segments such as luxury properties, downsizing retirees, and secondary markets with limited financing infrastructure. However, the importance of cash as a competitive advantage may continue to wane as mortgage markets stabilize and competition cools.

Comparison With International Markets

Globally, the U.S. decline in cash-based purchases aligns with similar patterns in other advanced economies. In Canada, cash buying surged in 2022 and 2023 before declining as borrowing costs fell and regulatory measures targeted speculative investment. The United Kingdom saw comparable behavior, with cash transactions peaking amid rapid rate hikes and then retreating by late 2024.

By contrast, in emerging economies such as Mexico and parts of Southeast Asia, where formal mortgage markets remain underdeveloped, cash purchases continue to dominate property sales. That global context positions the U.S. closer to the post-pandemic normalization seen among peer economies rather than any unique domestic collapse in demand.

Potential Impact on Affordability and Market Access

A smaller share of cash transactions could bring wider benefits to market inclusivity. For much of the past three years, fully financed buyers found themselves disadvantaged in bidding wars where cash offers guaranteed faster closings and fewer contingencies.

With that dynamic easing, younger buyers and moderate-income households using mortgages may find greater opportunity. Real estate agents in several metropolitan areas report that financed offers are no longer automatically dismissed, signaling a subtle but meaningful cultural shift in homebuying practices.

At the same time, sellers may face longer closing timelines and more due diligence as mortgage underwriting reasserts influence—a tradeoff many view as a return to healthy transaction norms.

Outlook for 2026

Looking ahead, industry forecasts suggest the share of cash purchases could remain around 27–30% in early 2026, depending on rate trends and investor sentiment. If mortgage rates continue to stabilize or decline modestly, this proportion may drift lower through midyear before plateauing alongside broader housing activity.

The interplay between liquidity, credit conditions, and demographic demand will define the next phase of housing recovery. For now, the decreasing share of all-cash home purchases stands as one of the clearest indicators of a market that is cooling—not crashing—after years of unprecedented volatility.

As 2026 progresses, the focus among economists and brokers alike will likely shift from questions of competitiveness to sustainability. With more buyers able to secure financing on fairer terms and fewer being pushed aside by cash-rich investors, the American housing market may be on the cusp of a long-awaited rebalancing that brings opportunity back to the everyday homebuyer.